The global supply chain is pretty well established at this point, particularly in the years since the obvious dollar devaluation (Y2K and forward). Commodity countries like the BRICs (South Africa only gets included in BRICS when gold is mentioned) ship to manufacturing centers in the east, primarily China, that assemble and manufacture for further embarkation to end markets in the US and Europe.

Europe we already know is heading further into the depths of depression, particularly France now. So it is not surprising to see the global supply chain slowing. But slowing is not collapsing, or should not be. Enter Australia.

The Reserve Bank of Australia just cut its benchmark monetary rate to 2.75% from 3%, a new record low rate. Since record low interest rates have become the norm for this age of global monetary defeasance, perhaps it should be expected. But Australia had largely been the exception to the global growth rule, particularly having been spared the worst of the Great Recession.

We have been talking about a bifurcated economy in the United States for some time – the uneven nature of inflation and monetary imbalances that are “positive” for some parts of an economic system, but decidedly negative for the whole. Even the Australian economy the past few years has been dubbed the “two-speed economy”. Mining and resource extraction had been booming, along with residential real estate. The rest – not so much.

The Australians are increasingly concerned that two-speed becomes one-speed rather quickly, and economies split by monetary imbalance always converge on the lower. Thus the RBA cut the monetary rate in an attempt to bolster credit effects in the lower gear economy, but also to get the Aussie dollar back in line in an attempt to help the resource export business.

The Australian Markit/CBA PSI index (measuring service sector activity) for April fell a rather large 5.5 points to 44.1. That was a particularly sharp drop indicating an accelerating contraction even in the lower gear section of the economy.

The Markit/Australian Industry Group Manufacturing PMI was, however, far worse. The headline index fell 7.7 points to 36.7, a level equal to May 2009. The export subindex indicated even worse conditions, all the way down to 24.5 – the lowest reading recorded in the series (going back to 2004).

These indications have been corroborated by other data points. Caterpillar’s latest earnings report showed that mining and resource extraction equipment demand is off by about 50%! That was a global indication that resource demand has not just slowed, but collapsed.

In addition, we know (or at least suspect) from China that although loan growth has remained relatively robust, almost all of the growth so far in 2013 has been concentrated on real estate. According to China Daily, loans to the real estate sector reached 12.98 trillion yuan, or up 16% Y/Y. In contrast, loans to industry only grew by 3.2%, down from 3.8% the month before. Less industrial demand from China, lower demand for resources in Australia.

The Baltic shipping indices are also down (and not just due to an increase in shipping tonnage). The Baltic Dry, which measures demand for shipping resources and ores around the globe, is down to $878; compared to $1,157 May 2012; $1,314 Mary 2011; $3,707 May 2010; $10,273 May 2009.

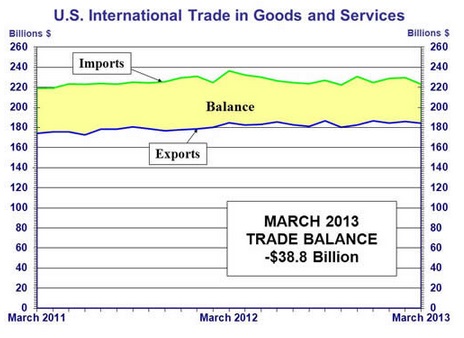

The US Department of Commerce also reported that the US trade deficit fell a remarkable 11% in March 2013 to $38.8 billion. Nearly all of that decline was due to a reduction in imported consumer goods from China – from a goods deficit of $23.4 billion in February to $17.9 billion in March. That was the lowest monthly merchandise imbalance between China and the US since March 2010. The $27 billion in total goods imported was 13% below the previous year (and the running three-month total for 2013 is down about 4% from 2012).

Given the state of Europe, the sum of all these data points validates the decline in Australia, particularly since Australia is heavily dependent on the Asian economy flow-through (in contrast to, say, Canada that is more directly exposed to North America). If this is correct, then the reduction in global supply chains is real and having an evolving and dampening impact on the global economy at various paces and places. It is a warning that worries should not be limited to Europe.

Stay In Touch