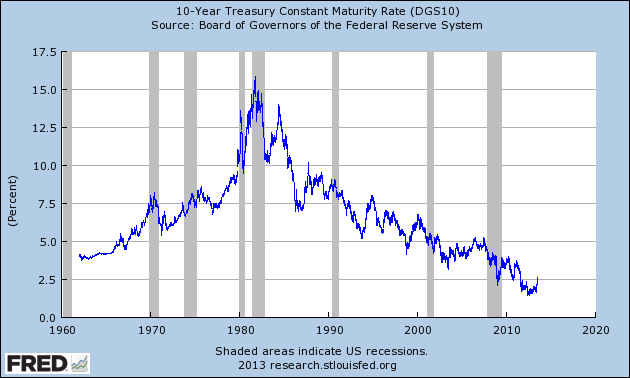

Interest rates, as measured by the 10 year Treasury note, are up roughly 100 basis points (1%) from the low yields set last year of about 1.4%. That has everyone and his brother calling for the end of the great bond bull market that has been going on all my adult life. The 10 year Treasury note peaked in yield way back in late 1981 at just over 15% and has been falling, with some minor hiccups along the way, since then until it hit a level 1/10 of that last year. I suppose this could be the end of the great bond bull market but before you make that call you might want to take a gander at this chart:

As you can see, the recent blip higher in rates has not changed this picture in any significant way. 10 Year T Note yields have been trending down for over 30 years and they still are. I also think it would be wise, before announcing that a trend this old is coming to an end, to at least check on the fundamentals of the market in question. Yes, the Fed has probably distorted things somewhat in the Treasury market but I don’t think they have nearly the control they or their cheerleaders believe so the economic fundamentals still matter. If the market decided, based on those fundamentals, that 10 Year Treasury Notes should yield 5%, I don’t think there is a damn thing the Fed could do about it. Richard Fisher apparently disagrees and last week said:

“Markets tend to test things,” Fisher told the Financial Times. “We haven’t forgotten what happened to the Bank of England [on Black Wednesday]. I don’t think anyone can break the Fed . . . . But I do believe that big money does organize itself somewhat like feral hogs. If they detect a weakness or a bad scent, they’ll go after it.”

I’m sorry, Mr. Fisher, but you are wrong. What the bond market just experienced was a minor rooting around by some fully domesticated piglets. If it had been feral hogs in the bond markets, Bernanke would have a tusk up his monetary transmission channel and we would have experienced something a bit more troubling that this tempest in a teapot correction we’ve had over the last couple of weeks. We didn’t get feral hogs in the bond market because there is little in the way of fundamentals that would justify a continued rise in rates. Inflation expectations are falling and while the Fed is forecasting, as it always seems to be, better economic growth in the future there is seemingly nothing but hope to justify that outlook. Commodity prices are falling and the dollar is rising, both of which are positive for the US economy long term, but probably not supportive of a bond bear market any time soon.

Of course that quick analysis doesn’t take into account other factors that might have an impact on bond prices and interest rates. The demand for Treasuries from abroad may be waning. Asian countries and other emerging markets have been accumulating Treasuries for most of the last decade as reserves. They accumulated those reserves with the expectation that they would use them to protect their currencies during a capital flight event. Well, unless we get lucky and Abenomics works just in time to pick up the slack from a bursting Chinese credit bubble, we might just find out soon whether those reserves are sufficient. The good news is that unless things get really bad, they probably are. The bad news is that to the extent they have to use those reserves, Treasuries will bear the brunt of the selling.

So bond yields could go up more if a problem crops up in emerging markets. Brazil is kind of the leading edge there so keep an eye on it. Still, even given that possibility it is hard to see a reason for bond yields to break that long term downtrend any time soon. The economic data continues to be uninspiring with housing and autos about the only bright spots. Jeff is convinced we are headed for a recession and that might turn out correct, but frankly I think this continued muddling along at a sub 2% growth rate might be worse. The continued weak growth and a compliant Fed makes it too easy for the politicians to ignore the obvious problems with our economy. The point being that even if the emerging markets have problems and end up selling some of their Treasuries, if the US economy continues to perform poorly, I would expect demand for Treasuries to be sufficient to keep yields from rising too much.

It appears to me that the US economy – indeed the global economy – is in transition right now from a weak dollar environment to a stronger dollar one. This transition has been going on for several years now but it takes time to change perceptions when trends have been in place a long time. The weak dollar period from 2002 to 2008 was one where investment was channeled into real estate and commodities and capital flowed to China and the emerging markets. A lot of investors seem to think that is the world in which we still live. Private equity funds are investing in real estate, oil companies are still investing in shale production and emerging markets are still considered to have better growth prospects than the developed world.

Unfortunately for those investors, the dollar has been strengthening for at least two years now. Gold peaked – and the dollar bottomed – over $1900/ounce in mid 2011 and has been trending down since. If you prefer the dollar index, its low was way back in late 2008 and after some volatility has settled down in a narrowing, yet obviously rising,trend. The rising dollar has long term investment consequences. Generally, in a falling dollar environment, investors move toward hard assets such as real estate and commodities to protect their purchasing power and to foreign stocks for growth. In a rising dollar environment, investors are less concerned about protecting purchasing power and are able to use their capital for more productive investments to fund growth in their home markets.

It takes time to alter investor behavior as the dollar rises. If we are really in a strong dollar period – and these currency trends tend to last a long time and are hard to change – the private equity guys funding condo projects and the oilmen spending capital in shale deposits and the institutional investors who think they have to have EM in their portfolios, are all going to be very disappointed with their decisions today. Those investments make a lot of sense when the dollar is weak but all face headwinds with the dollar rising. My guess is that PE will wonder one day why they didn’t stick to loading companies up with debt and firing people, oil companies will again learn to rue the day they answered the siren call of shale and institutional investors will find out that emerging markets are still emerging after all these years for good reason.

For now, we’re still seeing investment flow to weak dollar investments. But suppose for a minute that the dollar continues to rise and commodity prices continue to fall. What happens to all that capital flowing into North Dakota to fund shale oil development if oil prices fall to say $50/barrel? What happens to the rail tanker cars being used to move that oil around? What about the capital going into building housing for oil workers? What if all this shale activity stops because the price of oil makes continued drilling there uneconomical? So far, oil has not followed the CRB index lower but if the dollar keeps rising, that will change. And if it does and the shale boom turns to bust, a recession isn’t hard to imagine. Ultimately, a strong dollar and low commodity prices are good for the US economy but it will take time – and probably some pain – to transition investment away from weak dollar winners. And that is why the rumors about the death of the bond bull market may be greatly exaggerated.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, Joe Calhoun can be reached at: jyc3@4kb.d43.myftpupload.com or ![]() 786-249-3773. You can also book an appointment using our contact form.

786-249-3773. You can also book an appointment using our contact form.

Stay In Touch