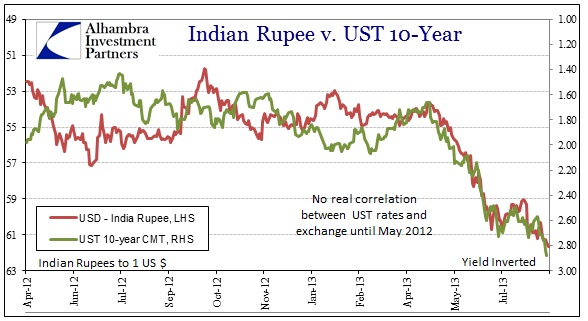

The Reserve Bank of India (RBI) was back in action yesterday, this time promising monetary measures in search of stability not just for the rupee but for collapsing bond and stock markets.

“Markets have fallen despite steps taken by the government and the Reserve Bank to support the beaten-down bond market. The RBI relaxed rules on mandatory bond holdings for banks, which would help protect lenders from large mark-to-market losses and said it would buy long-dated government bonds worth Rs. 8,000 crore.”

For now, the RBI is following the mainstream monetary script by using its position to intermediate currency flows into and out of India. In some ways this looks like QE, but it really doesn’t matter what name it is given. The crisis in India is being driven by the dollar, not the rupee. That’s not to say there aren’t significant problems inside India, including fiscal deficits and a dramatically slowing economy, but what is driving the currency threat is external.

We know this by the conspicuous correlations with US dollar markets.’

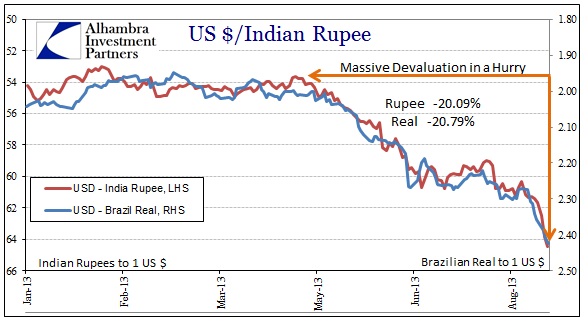

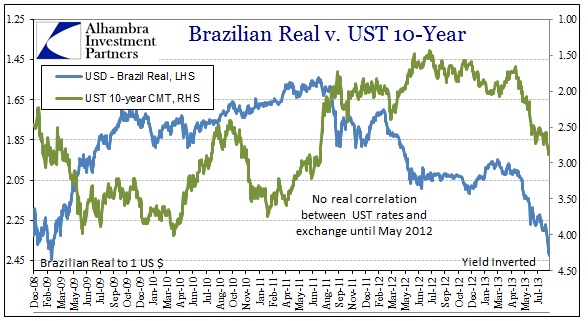

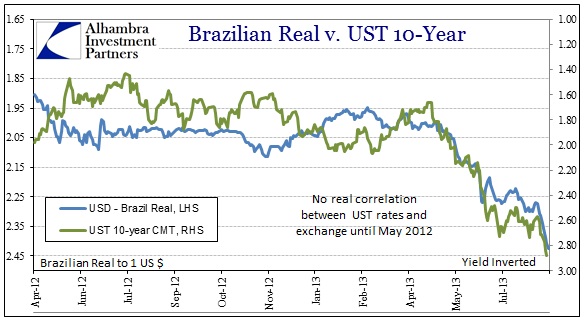

Not only is the dollar threat affecting India, it is the primary driver of Brazilian monetary distress too.

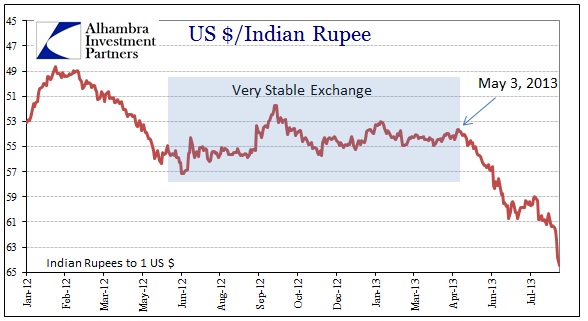

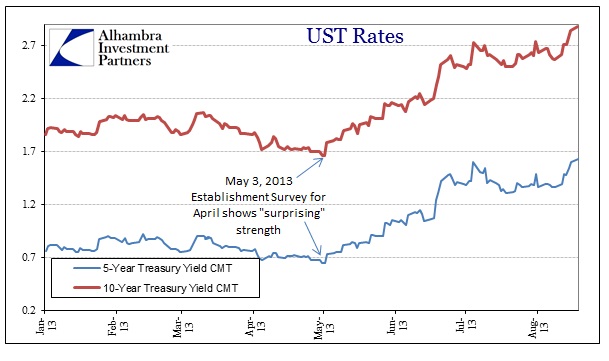

Both currencies suddenly began to devalue on May 3. That was the date of the April jobs report where the Establishment Survey “convinced” many that the recovery was at hand, and therefore the veiled threats to “taper” were about to become serious. It was the same day the US bond market selloff began.

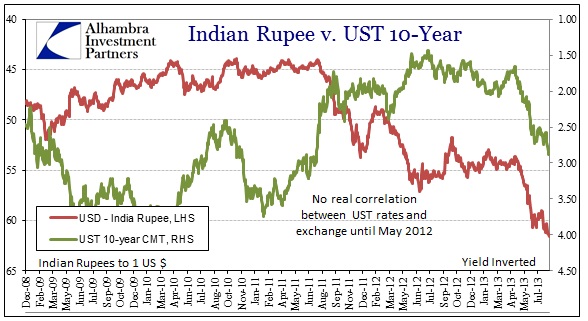

There usually exists, in the economics textbooks at least, an expected relationship between rates in the US and rates abroad (interest rate differentials are still believed to be a primary factor in exchange rates). But there did not exist much correlation between UST rates and the dollar exchange with either reals or rupees prior.

That changed in May 2012, around the time the US economy began to slow. The downshift in US growth proxies increased expectations of an imminent QE 3, particularly centering on MBS. Regardless of the target, that was when the housing bubble began to “froth” and dollar finance changed toward such policy.

Where no correlation existed before, suddenly stability in the US bond market was exported as stability in the rupee and real. When the bond market reacted violently to perceptions of tapering US QE, other currencies simply followed the funding structure. This is commonly called the dollar carry trade, and it runs through London.

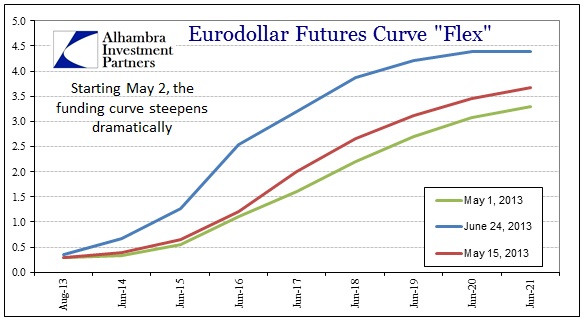

The effect of taper on liquidity and funding markets was evident in eurdollar futures, as even the thought of tapering has steepened the funding curve and introduced a massive amount of volatility into the liquidity structure. In short, global markets were leveraging themselves to US QE policy expectations, and are now caught the wrong way as Bernanke and the FOMC are experiencing buyer’s (UST & MBS) remorse.

Ever since the Bretton Woods system collapsed in the late 1960’s (ending with the Nixon administration’s gold convertibility ban in 1971), the global trade and finance system has been operating on a dollar swap standard run through eurodollars (I wrote about this historical transformation here). The availability of US dollars in London has been a central and ongoing crisis/anti-crisis theme since August 9, 2007.

Now as QE perceptions unwind, global liquidity disproportionately shrinks. The banking system that was once fully oriented to endless QE is now jeopardizing economies and markets all over the globe. As the dollar shortage squeezes further, and it will given the readjustment of risk models that are right now incorporating this dollar funding volatility, there will be little the RBI or Banco do Brasil can do on their own. To arrest the currency declines will mean a program of rapidly rising interest rates, further killing their own economies. If they let their currencies keep devaluing, they further risk market destabilizations and devastating internal inflation (and their economies get killed anyway).

Because global monetary policy has been wrongfully focused on suppressing “tail risks” after the European crisis in 2011 (eurodollars prominently featured), the entire funding system has misguidedly rebuilt based on that policy, particularly US QE. The only way an unwind stood even a remote chance to be orderly was in an environment of robust global growth. Since QE can never create such an environment, it was bound to be a disaster at some point.

The corruption of orthodox monetary economics runs very deep and very far.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@4kb.d43.myftpupload.com

Stay In Touch