Given the relatively light holiday week, I thought it somewhat appropriate to finish the very heavy and systemic examination of the series on eurodollar markets (Part 1 here; Part 2 here). The preceding episodes were dedicated to the eurodollar system as it built up toward the 2007 reckoning. What started out as an alternative to the gold standard quickly morphed, as everything does with finance, into a conduit to convey overwrought credit production (in dollar terms) globally.

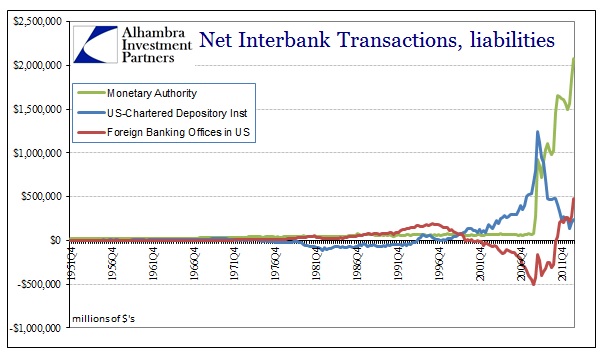

Accounting for this evolution is difficult, made so largely by the OTC nature of the vast majority of arrangements. That is not to say that we have no idea or measurements, however. The Federal Reserve’s Flow of Funds report (Z1) tracks interbank transactions of primary dealers and the overall banking system (derived from call reports and the Federal Reserve Bulletin, among others). Since domestic interbank markets on a systemic basis net out to zero (if Citigroup lends overnight to Merrill Lynch, for example, there will be changes on each individual balance sheet, but the overall system sees zero net change since the lending of those funds is cancelled out by the borrowing of them).

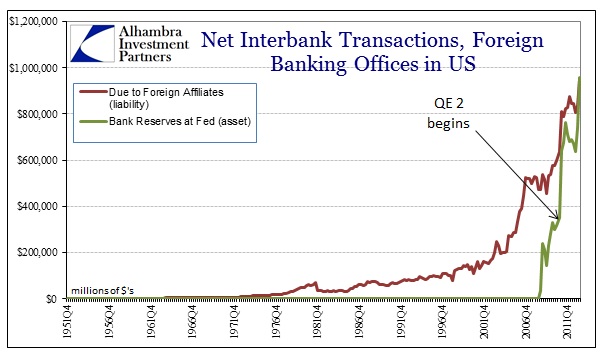

Net interbank transactions presented on this basis, then, mostly relate to foreign transactions, i.e., eurodollar markets. Getting back to Milton Friedman’s initial framework, this makes sense since “excess reserves” in the US form the basis of claims on dollars in foreign dollar markets. As we have seen, though, there is a world of difference between participants and dispositions. US banks behaved differently than foreign bank branches operating in the US.

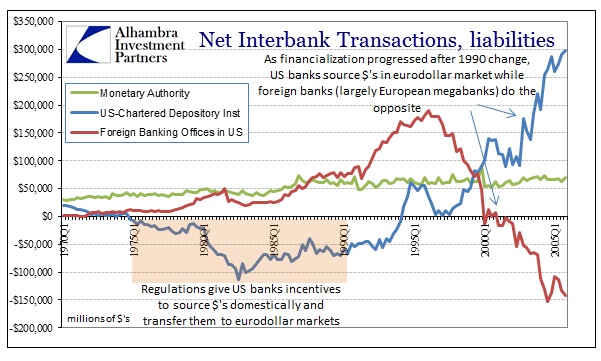

This is due in full part to regulatory differences, particularly before 1990 (and 1980 with Regulation Q). As the eurodollar market became more and more financialized, tending away (at the margins) as a source of financing global trade, US banks “borrowed” dollars in foreign markets for transfer to US operations (the blue line above turning positive), contrary to the original design. Foreign banks operating branches inside the US did the opposite – they sourced dollars inside the US and transferred them to foreign dollar markets (the red line above turning negative).

For its part, the Fed maintained a stable balance sheet, adding little to the changing dynamics (focused instead on maintaining its interest rate target beginning sometime in the 1980’s).

That obviously changed in 2008. The crisis began in 2007, but, as shown in the chart above, dollar supply in interbank markets was first reactive in private sources, not the monetary authority. This was the infamous “money elasticity” of central banking lore, as the banking system itself created additional “dollars” in response to a liquidity event. The main problem, contrary to the orthodox interpretation, was not one of dollar supply but fragmentation among dollar markets and dollar participants (flow).

The pathology of the 2008 panic conforms to the contours of conventional thought about financial crises. The Fed’s first instinct was solely to “encourage” private dollar sources to fill the breach. Indeed, it was believed to have been fully effective after Bear Stearns failed, with only some modifications to collateral programs. The central bank was eventually forced to step in and create “dollars” ostensibly to break the blockage in flow by essentially recreating wholesale interbank markets almost entirely.

Various dollar programs were fashioned which would bridge (it was hoped) the divide between those that had access and those that didn’t (TALF, AMLF, PDCF, etc.). The Fed also conducted reverse repos designed to take in “excess” cash and disperse usable and functioning collateral (along with the Supplementary Finance Program with the US Treasury). In those cases, the Fed was both a supplier of “dollars” and a user of them. That is not indicative of a supply issue, but of flow impediments. Instead of lender of last resort, the central bank became the wholesale intermediary of “dollars.”

Quantitative easing has been something entirely different. Those looking at QE through the lens of a liquidity program are making false interpretations (and expectations). QE is nothing more than a psychology experiment, owing to adherence to rational expectations theory. Conventional wisdom posits that it is akin to “money printing”, but QE only creates inert balance sheet entries.

That is not to say that there is no impact on systemic function. Rather, QE distorts collateral markets first, by removing usable collateral from repo markets. I’ve covered that topic at length. But QE is also having an impact on eurodollars.

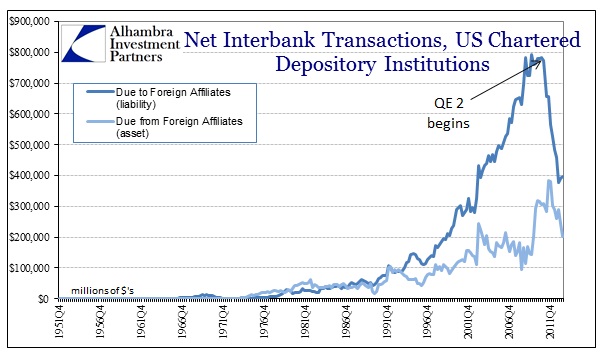

Where eurodollar markets were growing in size and scope until 2007, they have been retreating since QE was first initiated. On the US side, domestic banks’ tendencies to source operations through eurodollars has dramatically declined since QE2. The net figures cited in the charts above don’t tell the whole story.

In terms of both assets and liabilities, US banks’ borrowings from eurodollars has declined by about 50% since the advent of QE2. In other words, US/domestic volume participation in eurodollars has collapsed.

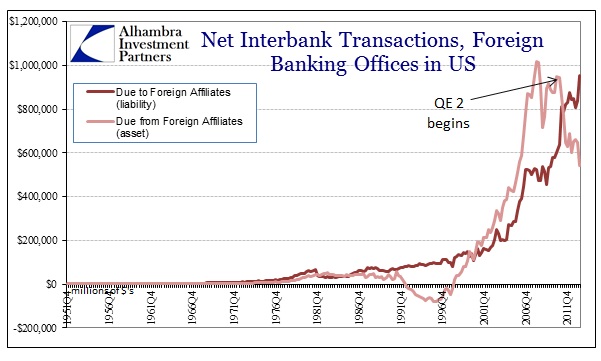

On the other side, foreign propensity toward the opposite has been similarly disturbed.

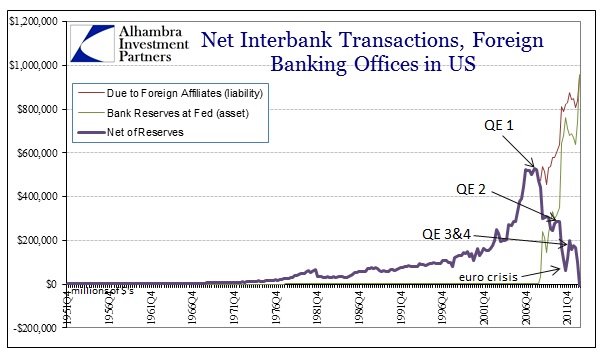

In terms of foreign bank participation, their liability side is being skewed by the accounting for QE purchases of assets. The operational component of QE is to purchase assets from foreign banks (the ultimate holders of dollar-denominated assets), with reserves being booked at US subsidiaries (since foreign banks cannot participate directly at the Fed, but their US-based primary dealer subs can). Thus, in the chart above, the liability side is skewed by this transfer between foreign bank holders of US-dollar assets and domestic branches – making it appear that foreign banks are growing sources of dollars here.

If we adjust the liability of Foreign Banking Offices in the US by those branches’ holdings of “reserves” at the Fed (those inert “dollar” balances created by QE), we see far more clearly that foreign bank participation in eurodollar markets has also dropped significantly.

Not only has participation declined dramatically, the stepped pattern coincides exactly with the QE programs themselves. The net effect from QE is apparently a substitution of privately sourced dollars (pre-crisis) for publicly-created/central bank “dollars” that are totally inert, and therefore unsuitable for that task (because that was not the intention). It’s as if the Federal Reserve has crowded out the private system of wholesale “money” creation. And that makes intuitive sense because low interest rates are not exactly conducive for private firms to engage in risky transactions, including interbank wholesale dollar arrangements. Further, there is a world of difference between private money creation with a direct and intended purpose compared to central banks that create inert money without a direct and immediate purpose.

The combined effects of reduced collateral availability plus crowding out private dollar sources would logically produce uncertain and uneven funding conditions. Thus the very heavy hand of QE 3&4 might then be expected to reduce dollar functioning to the point that curious and troubling liquidity-related occurrences increase in frequency. It might also be reasonably expected to make these markets particularly susceptible to “exogenous” shocks, such as expectations for changes in policy stances (taper).

The usual warning and caveat applies here – namely that we have limited visibility in these types of markets – so we do have to be careful about being fully deterministic. Given that, however, it does seem consistent with the various secondary indications that have been observed throughout 2013. In short, QE is negatively affecting market liquidity via these channels, including a large decline in depth and volume of eurodollar availability.

That may not necessarily pose a problem or hazard, particularly since eurodollar markets are not only driven by short-term funding conditions. Eurodollar banks might just as well reduce reliance on overnight funding through these interbank markets and replace them with bond or loan funding. That is certainly what regulators wish to see, and are actively nudging participants toward that end.

That may not necessarily pose a problem or hazard, particularly since eurodollar markets are not only driven by short-term funding conditions. Eurodollar banks might just as well reduce reliance on overnight funding through these interbank markets and replace them with bond or loan funding. That is certainly what regulators wish to see, and are actively nudging participants toward that end.

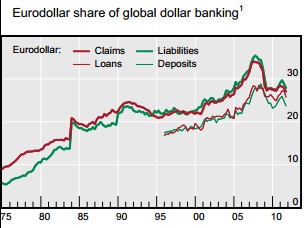

I don’t doubt that some of that has taken place, and that banks, now aware of fragmentation and flow risks (learned, as usual, the hard way), are actively seeking alternative funding models. But it is far more likely, given the timing of interbank conditions relative to QE implementations, that dollar sourcing in these markets is being reduced by these very monetary distortions. Since the eurodollar market itself is shrinking in terms of total credit relative to the total world banking system (chart to the left, from the BIS), the QE explanation is, by far, the most likely.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@4kb.d43.myftpupload.com

Stay In Touch