It’s that day of the month when the apex of silly attention gets focused on the BLS. Just in time to directly contradict the FOMC’s “careful” rationale for cutting back on the fuel for small caps and the flood of cov-lite, the December jobs report was wintry. Despite the paltry advance in the Establishment Survey, there has been a rush to refocus that silly attention on the 6.7% and the “improvement” in the official unemployment rate.

For the most part, economic accounting has at least some high degree of rational sense embedded as a core concept. The unemployment rate, for example, makes intuitive sense as a proxy for economic growth as it relates to and through jobs and what most people believe to be a functioning economy. But the edge of that logical sense clearly lies when movements in the fraction predominate in the denominator. It was never meant to be accurate for this kind of condition because such a condition was never believed possible for any length of time.

That itself should lead to more intense scrutiny over other economic accounts as they suffer the same sort of recency bias. There is a lack of account going back to the foundation of these statistics, not the least of which is the embedded assumptions in all of it that the current state of affairs will closely resemble the past, or even the recent past.

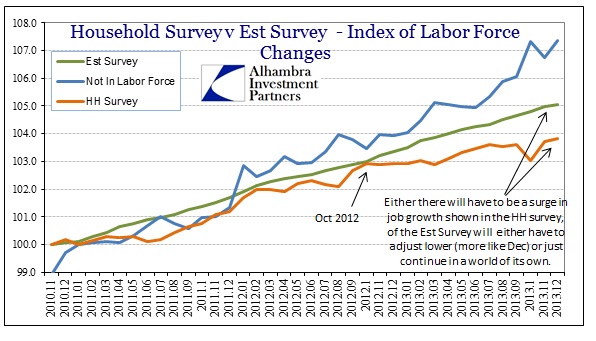

That is why it is becoming increasingly clear that the heavily adjusted Establishment Survey finds itself on an economic island, alone and secluded. What a state of affairs for the FOMC to use as cover in an effort to extricate itself from its own policy creation; when even the fashioned Establishment Survey disappoints just when all is set to be proclaimed right with the economy.

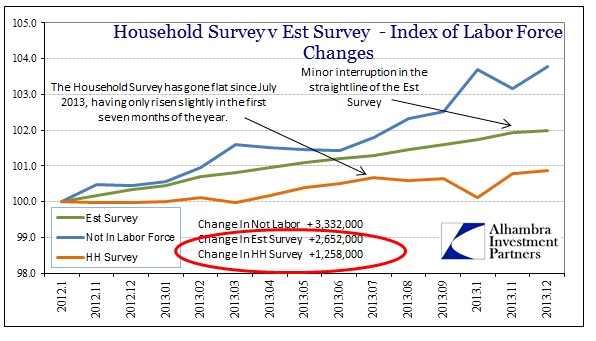

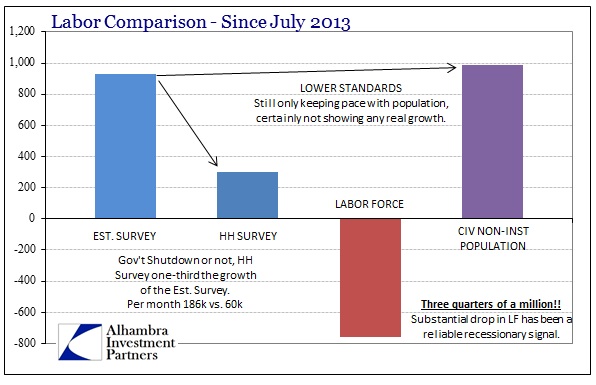

Outside of the carefully crafted plucking measure, the economy looks decidedly less robust. The Household Survey actually doubled the Establishment Survey in December, but to little avail over the course of 2013. The numbers are downright ugly (meaning recession-like).

Since October 2012, where there was clearly a break between the two surveys as the economy clearly downshifted, the HH Survey is now at just half the pace of its more “precise” cousin. On a per month basis, the Est Survey has gained at about a 189k rate – which we are told is a recovery signal. It is not, at least by any historical definition. The HH Survey, on the other hand, features a 90k monthly rate. At least it’s not negative?

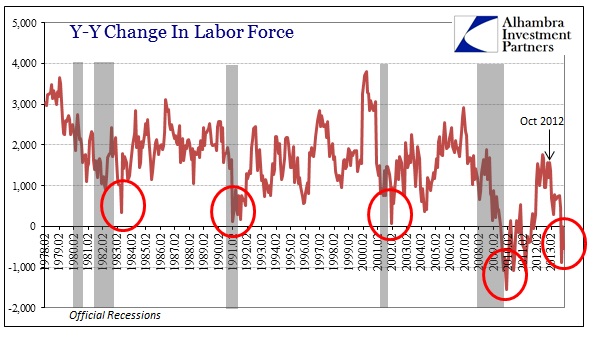

In reality, pretty much all of that above is noise. The most important part of the Employment Situation Report as it pertains to economic “cyclicality” is the official measure of the labor force itself. Most people are well aware of the labor force participation problem, and again in December it was more than ugly. But since the middle of this year something has changed, a clear inflection, where even labor force members are now moving out.

If this is associated with a recovery it would be the first time in history. Being careful of recency bias myself, I have to at least admit that possibility; but Occam’s Razor also applies. What is more likely, particularly given any number of parallel economic accounts, that the economy has a shrinking labor force leading to recovery or that conditions changed for the worse right around the time the bond market sold off, interest rates headed significantly higher and the trickle of mortgages completely collapsed?

Since July, the official labor force has declined by an enormous 756k! That simply does not happen except in recessionary conditions. In fact, the labor force is again down Y/Y, something that is highly recessionary.

Putting this all together, when the economy experienced a sharp downward adjustment in the middle of 2012 it had an effect on the demand for labor. That is exactly what we see in the Household Survey, the Labor Force and the participation rates. But there was a second “shock” or inflection downward in the middle of 2013 that coincides with the taper-driven fiasco of dollar tightening. It is still too early to confidently assert that as a cause, it could be coincident tied to a further change in some other governing dynamic, but there is enough to at least speculate in that direction. It also appears to follow an even earlier template, should history be a valid comparison in this manner.

What I can be very confident in asserting here is that this is not a recovery at all, given nearly every indication of the opposite direction, and that there is a very low probability that this is some new type of recovery heretofore unseen. On the one hand is “precision” and faith that monetary policy actually works, and diametrically opposed is empirical study.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@4kb.d43.myftpupload.com

Stay In Touch