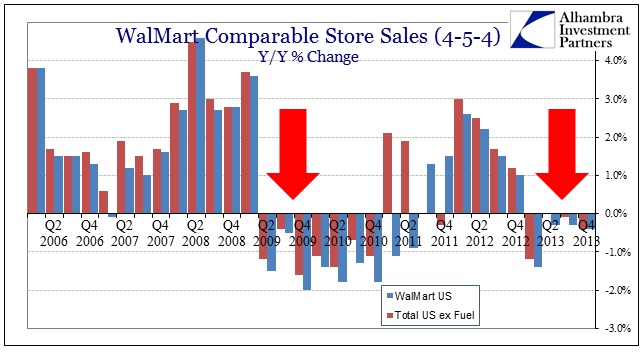

In the fourth quarter of 2007, WalMart became the first retailer in history to surpass $100 billion in quarterly sales. It was an impressive feat despite growing unease over what were then considered (by the vast majority of economists) unrelated matters of the financial economy (subprime was “contained”). Overall, sales had grown 8.3% (including membership fees to Sam’s Club), though profit growth was underwhelming at +4%. The retailer had made a conscious decision in late 2007, in advance of that holiday season, to cut prices in order to capture market share. In some ways that was successful, but comparable store sales in the US only grew 1.6%, adding to that economic uncertainty.

One year later, after Lehman and amidst ongoing panic in the financial economy, WalMart reported only 1.6% revenue growth and a rather stark 7.4% decline in net income. However, comparable store sales were better than the holiday period of 2007, growing at 2.8%.

The holiday season results for 2013 are worse in every meaningful qualitative measure than those two periods. Total revenue for the fourth quarter was up only 1.5%; net income fell a rather alarming 21%. Comparable store sales in the US, both with and without fuel, declined 0.4%.

As with the other major bellwether companies I have highlighted recently, it seems as if they no longer matter, certainly not to economists. I believe that there is great deal of value in analyzing actual results of companies as both a proxy and companion for the often esoteric statistics that we use to form judgments about the health and direction of the real economy. Can it be consistent to expect that the current economy is functioning somewhat “normally” when its largest retailer just turned in a quarter, the Christmas shopping period no less, that is objectively worse than either 2007 or 2008?

It would be easier to dismiss it all if this was an outlier, a potential misstep in one period among many others that show the opposite. But WalMart’s struggles have been ongoing for more than a year now. Despite economists’ assertions and comfort infiltrated by QE-based math, what we have seen from WalMart actually matches the wider pattern of so many other statistical series. Trouble began in the middle of 2012 and has only grown worse since then; to the point 2013 has been, not a revival as so commonly cited, but a disaster.

These results cannot be ignored as irrelevant in any macro context. The best case is that WalMart is only representative of the “lower strata” of the US and global economy. That is damning with faint praise, mostly because a truly healthy economy would see growth throughout, not concentrated in very narrow corridors most exposed to asset inflation.

That formed a major part of the intentions of the QE/ZIRP experiment, a bastardized trickle-down effect where “wealth”, at least nominal changes in asset prices, would eventually lead to rising growth in all sectors and income layers. Yet, if this was a valid theory or idea, it should have been apparent by now. It’s not as if we are rushing to judgment here, that QE hasn’t been given enough time to work through lags and feedback effects, it has been more than five full years.

If it hasn’t worked, and WalMart’s results are pretty conclusive in that direction, through five years and four discrete applications, it seems reasonable to conclude that it likely never will. Unfortunately, taper and eventual removal is not the same as never having gone through the QE experience at all. QE has not been a neutral proposition, an experiment that only failed to yield positive results. There has been a definite cost to its applications, and thus the economy is actually much worse off now than had it never been started.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@4kb.d43.myftpupload.com

Stay In Touch