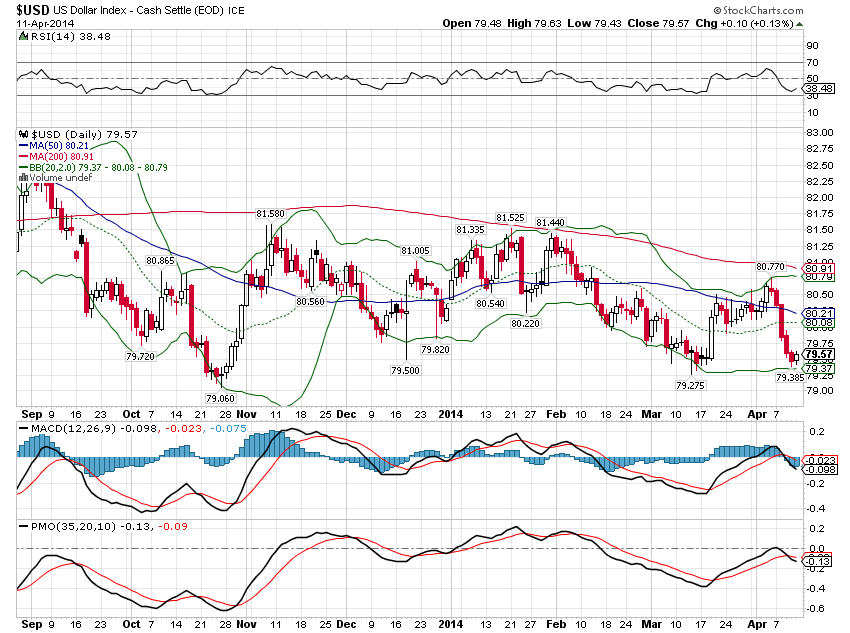

The US Dollar index exhibits the classic characteristics of a downtrending asset: Declining 50 and 200 day moving averages with the 50 solidly below the 200. Momentum indicators (MACD, PMO) both on sell signals.

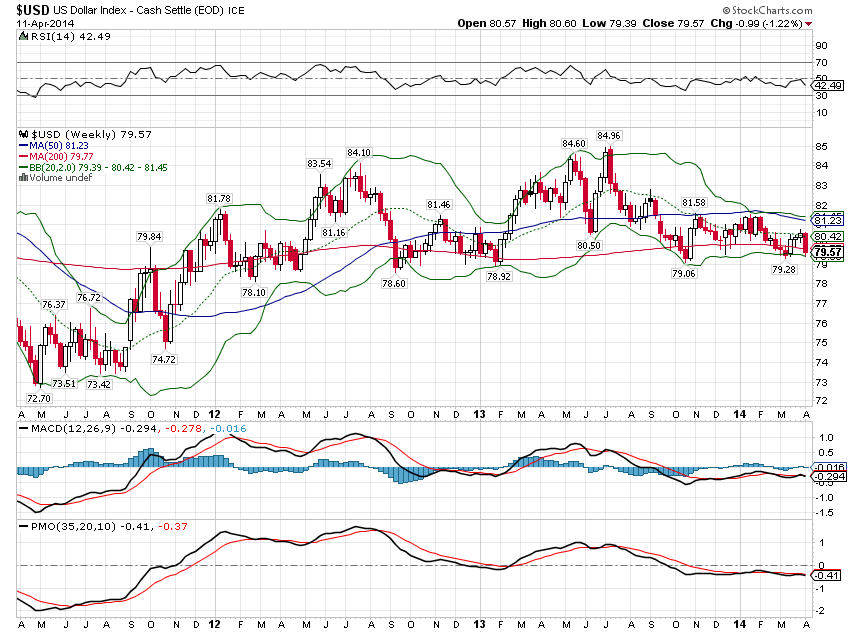

A longer term view shows the index on the edge of support:

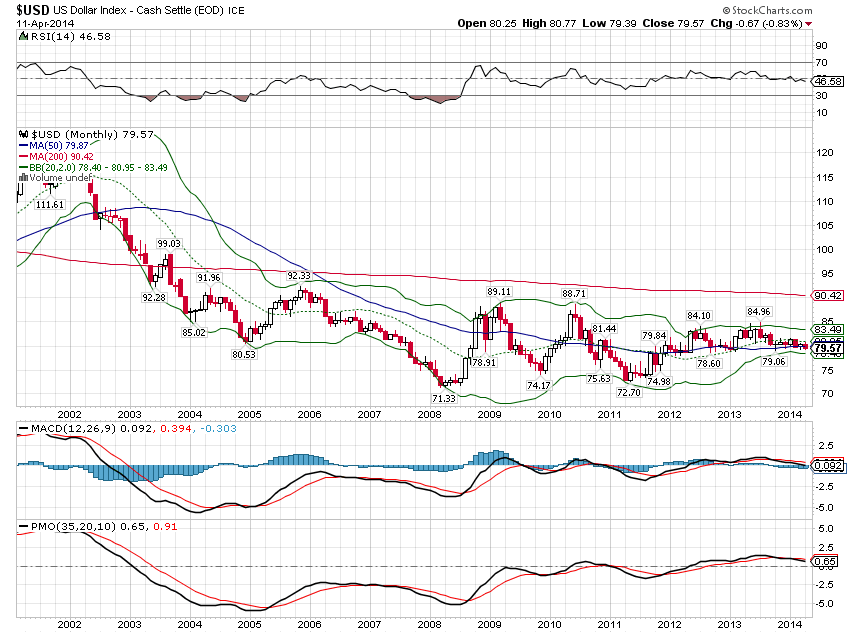

A break of the 78-79 support level would open the way to a return to the lows. A very long term view on the monthly chart shows some reason for optimism as the index has built a base over the last few years:

Unfortunately this dollar stability of the last few years is somewhat of a mirage. Other indicators of the value of the dollar, such as gold and general commodity indexes, have been much more volatile. Regardless, from a technical perspective, all these charts point to a return to the weak dollar environment we experienced from 2002 to 2008. The reasons for renewed weakness are hard to pinpoint (as always) but I’ve always viewed currency values as measures of growth expectations. Interest rate differentials do play a role but not as much as most suppose.

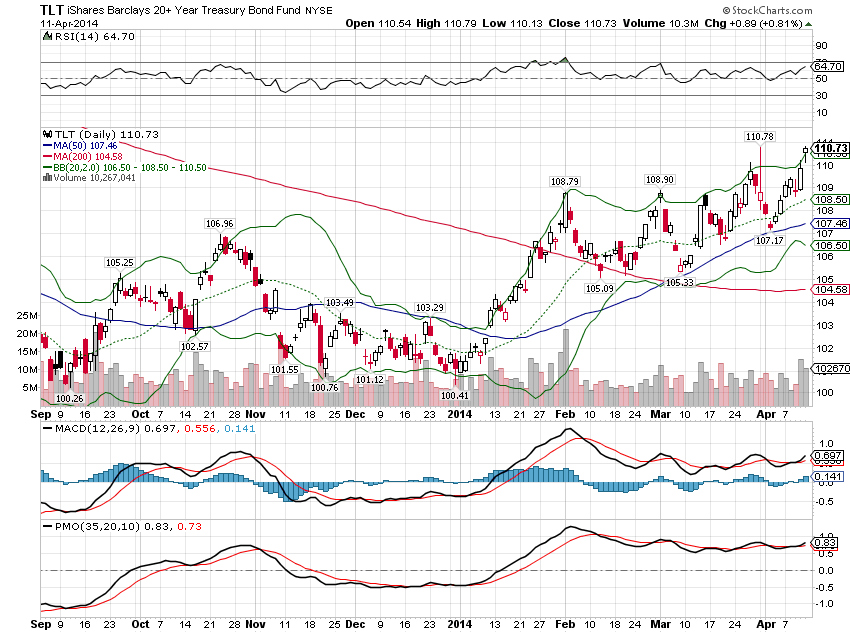

Fear of weaker growth can be seen rather starkly in the Treasury market:

The long term Treasury ETF (TLT) has been rallying rather hard since the beginning of the year defying the market expectation of the opposite as the Fed tapers its QE program. Of course, anyone who bothered to look at what happened after the end of previous iterations of QE isn’t surprised by this development but the expectation that the last QE finally did the trick and moved the economy to a self sustaining expansion is, I guess, hard to kill. The popular, mainstream view of the economy since before the end of last year is that recent weakness is a function of a hard winter, but if that were true one would expect to see the bond market start to reflect better growth expectations as the weather warms. That may yet happen but there is no evidence of it yet.

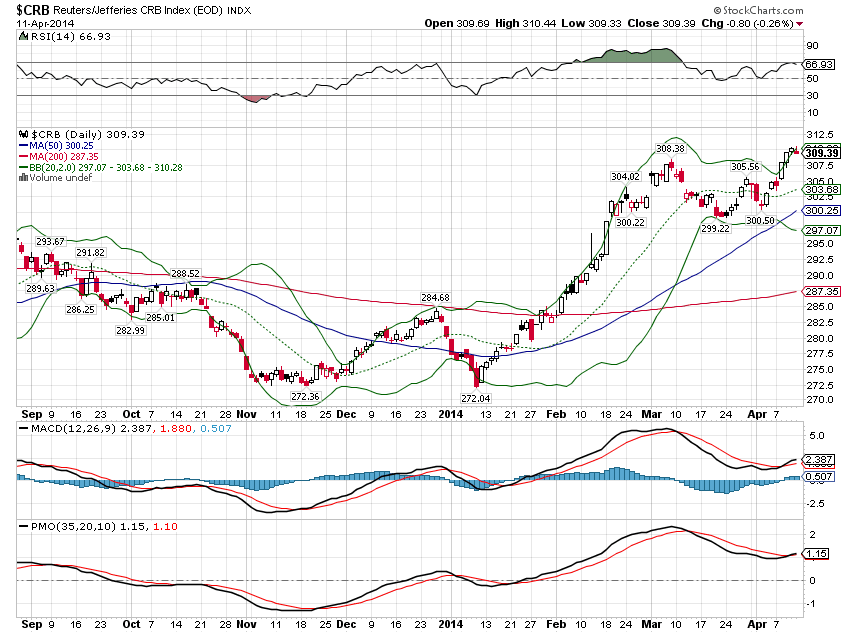

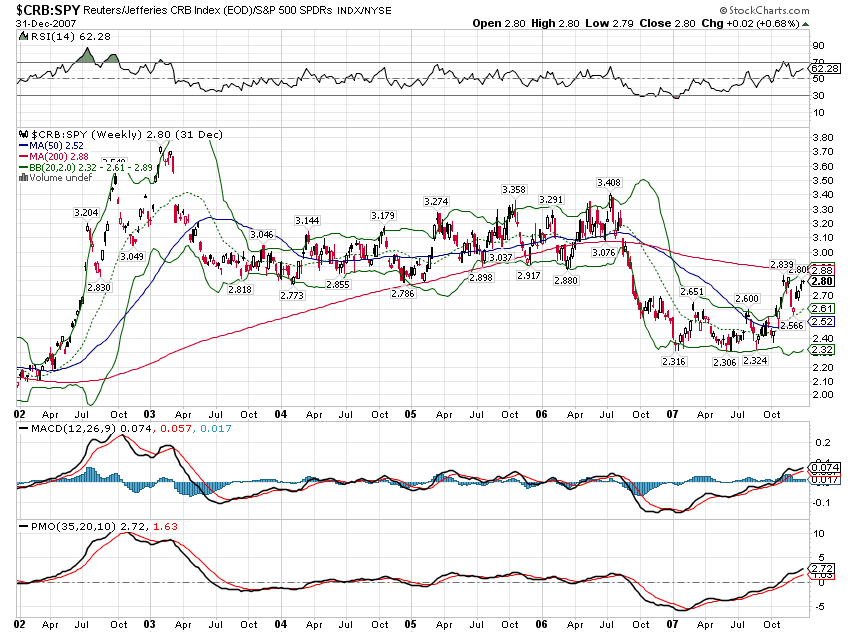

The weaker dollar also shows up in other assets. A weak dollar has a direct and fairly immediate influence on commodity prices:

A broad measure of commodity prices, the CRB index, has been moving higher as the dollar has moved lower and bond prices have moved higher. It is somewhat contradictory to see commodity prices moving higher even as the bond market prices in lower growth and inflation but the value of the dollar has a large and immediate influence on the dollar price of globally traded commodities.

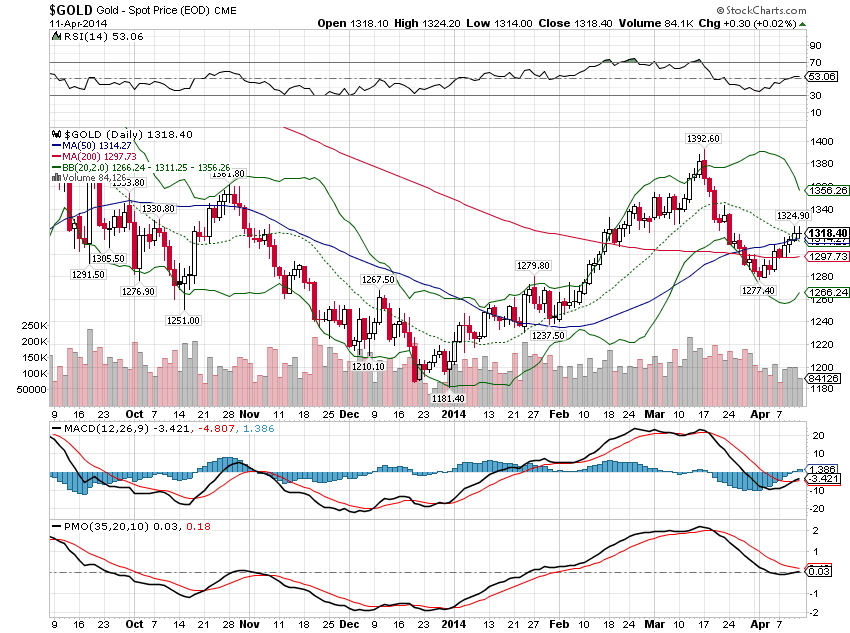

Despite a recent correction, gold has also been tracking the movements in the dollar. Gold could also be reacting to renewed expectations of weaker growth and further Fed action but there is no way to know the minds of all the participants in the gold pits.

I am not a technician and don’t invest or trade based solely on chart patterns but they are an easy way to get a high level view of what is happening in the markets. Often one finds that the market is sending an entirely different message than the one being proffered by the denizens of the sell side. In this case, the dollar index and the bond market seem to be saying that US economic growth is suspect while all the talking heads on CNBC keep talking about a re-acceleration. Who you gonna believe? Wall Street or your lyin’ eyes?

A weak dollar, no matter the cause, has implications for investors. Global capital flows move markets and currency trends tend to get reinforced. Momentum isn’t just about stocks and trends in currencies tend to persist and overshoot. The dollar fell pretty steadily from 2002 to 2008 until we reached a point where the imbalances were too large and had to be corrected. If this is the beginning of a new downtrend, a look back at that previous period may be instructive.

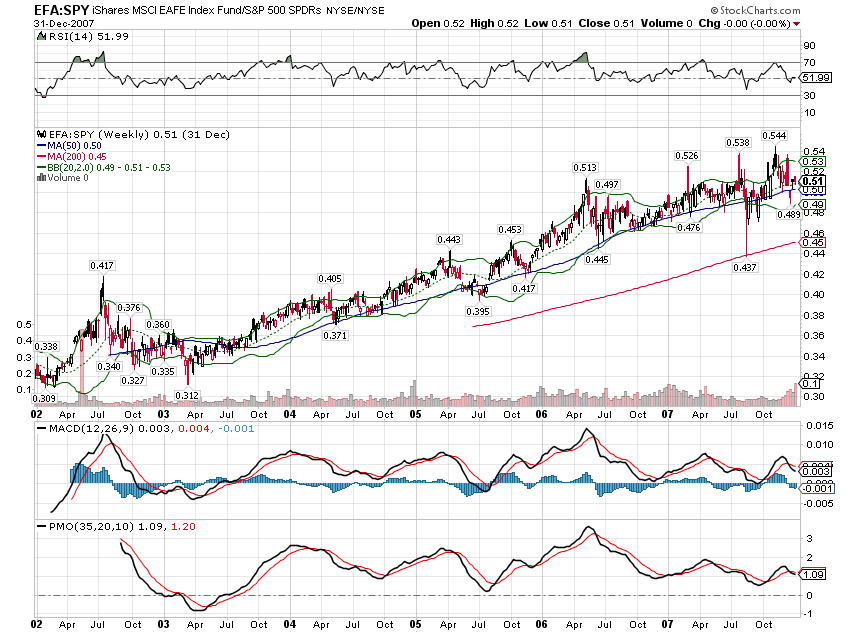

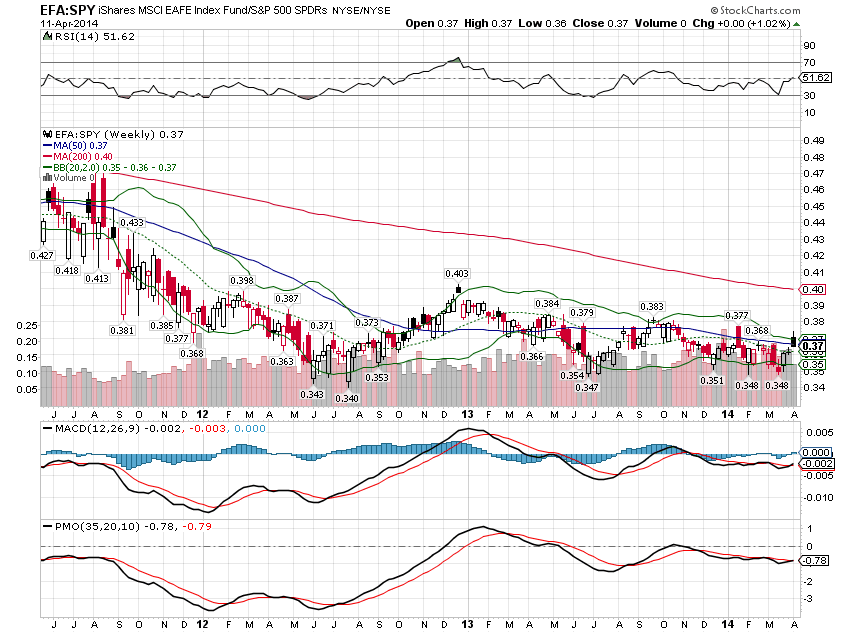

A fairly obvious implication is that foreign stocks tend to outperform during periods of dollar weakness. This makes sense as the flip side of weak dollar is a strong foreign currency which adds to an investor’s performance. In the previous weak dollar period, the EAFE outperformed the S&P 500 by over 60%:

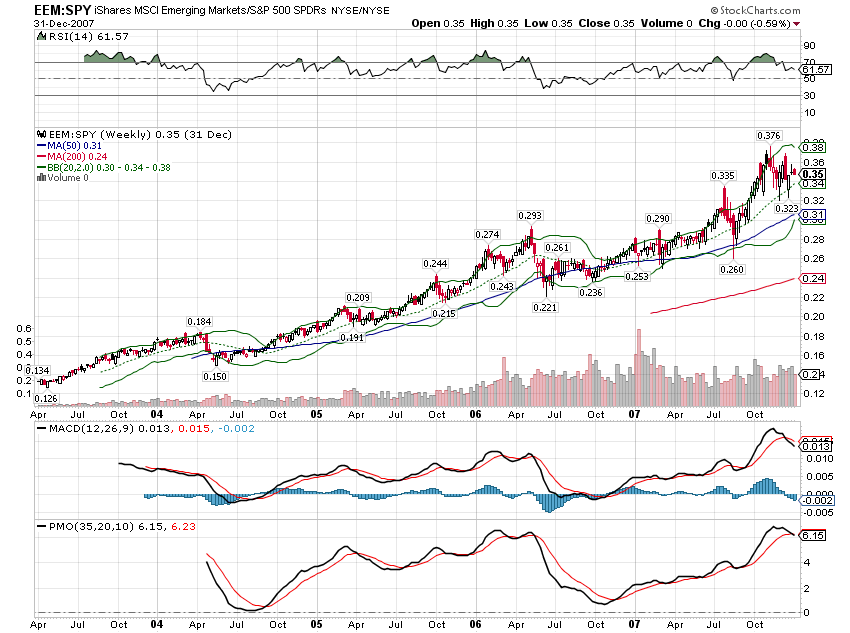

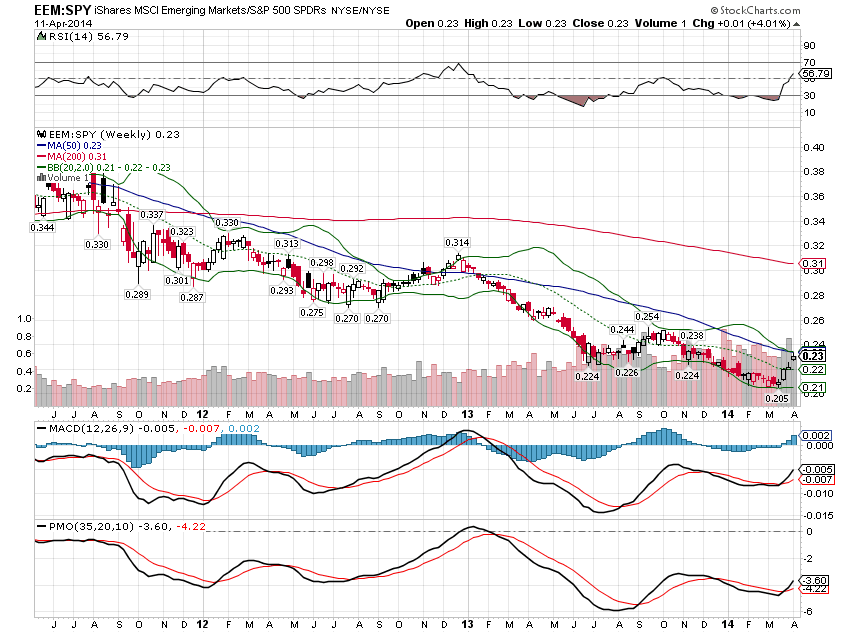

Emerging market stocks reacted even more positively:

Commodities and gold also tend to outperform in weak dollar periods but the correlation is not as strong. It seems that dollar weakness has a strong influence at first but then fades somewhat as commodity producers respond:

Foreign stocks are not yet outperforming their US cousins but they have at least held their own and the EFA:SPY chart has built a base:

Emerging markets, although they have outperformed very recently, haven’t yet broken their downtrend:

It does seem contradictory for foreign stocks to outperform if the message of the dollar index is weaker growth expectations in the US. Much of global growth is dependent on US growth, especially in emerging markets, and it is hard to see how foreign economies and markets might outperform if US growth declines further than it already has. I’ve never bought the decoupling thesis and if US growth falls to recessionary levels, the rest of the world will feel the pain. It may be though that the message is one about relative growth rather than absolute growth rates. One thing we do know is that foreign markets are generally cheaper than the US so shifting a larger portion of one’s portfolio to non US stocks would seem prudent regardless of the direction of the dollar.

I don’t know yet whether this is the beginning of a new trend for the dollar but it certainly bears watching. Investing during a weak dollar period is different than a stable or strong dollar environment. Generally with a weak dollar, one would want to favor foreign stocks and hard assets such as real estate and commodities or commodity producers. Stable and strong dollar periods are generally favorable to US stocks and negative for real assets. If this is the beginning of a new trend lower for the dollar, a lot of investors are going to have to adjust to the new environment. That may explain the recent weakness in US stocks as much as anything else as traders try to anticipate the emerging new trend. Another possibility is that the talking heads on CNBC are right, the US economy is about to take off and all this will get reversed in short order. Nah…

Stay In Touch