In looking at policy expectations, I continue to believe the shift in the Fed is both dramatic and durable. On the one hand, QE without Bernanke is toast, as the growing consensus appears to be that the economy is running here and now at or above “potential” (explaining in an orthodox manner why the unemployment rate is falling so precipitously at such low GDP growth). That sets the path of short-term interest rates against the economic grain – lower growth is not supposed to mean higher short rates. Rules based proponents would undoubtedly agree, and that includes Yellen.

But these are unusual times where the short end of the curve is nothing if not artificial to the very end. Thus any shift in stance, even an exceedingly minor one, can set off short rate violence.

At the long end, by contrast, the lack of expected future growth reduces the expected path of interest rates. The Yellen “shift”, such that it may exist, thus may render short rates as at best volatile and unappealing (taper to tighten) and long rates attractive as Bernanke-optimism leaves office with him.

I think that is the best explanation for the behavior in money markets and the treasury curve – particularly since many of these indications showed up right around Yellen’s coronation. Economic growth expectations are being reduced all across the complex at the same time monetary policy is heading toward tightening biases. That was never supposed to be the case, as rate “normalcy” was supposed to be accompanied by more historic levels of economic attainment. It was such an element of unequivocal faith among Fed and orthodox adherents that it is now being discounted as a valid narrative and explanation. The recovery idea dies hard.

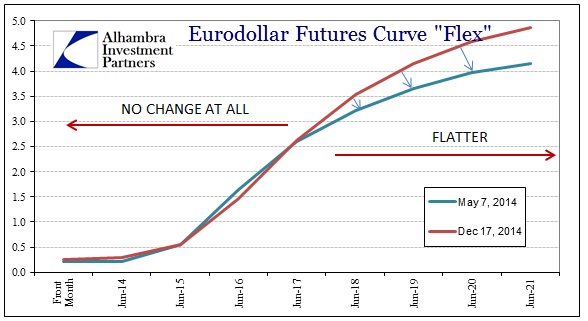

Yet that is exactly what we see in eurodollars and the treasury curve. The flattening portends future interest rates far less than previously assumed, while the short end holds no movement at all – the FOMC’s “dots” are proving to be a strong anchor. That is confirmed by the pivot: 2017 and out. That is the maturity where policy ends the “emergency.”

In terms of the eurodollar curve, such flattening is nearly unambiguous in its interpretation about future interest rates. Given the convexity of money markets, hedging “requires” buying more on the curve where rates are expected to fall. That plus swap spreads produce little doubt, to me, that institutions are preparing for lower rates in the future.

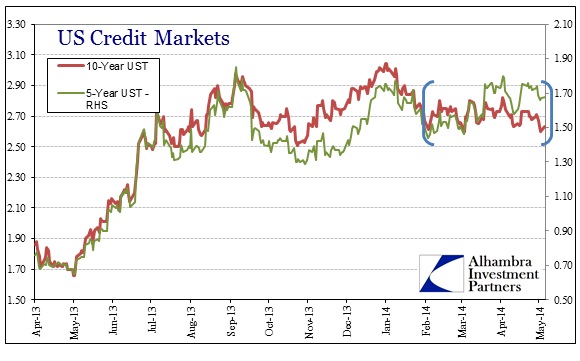

I don’t think it ends up as simple and orderly as all that. You cannot simply downgrade the efficacy expectations for extreme monetary policy and expect the absence of disruptions. That is particularly true given how monetary power has reigned over these “markets” for years now (decades going back to the idea and institution of interest rate targeting). To say that even mighty QE is unable to present a “normal” recovery will undoubtedly have downstream implications. That, again, offers a good explanation of the recent “stasis” evident in all these credit market factors.

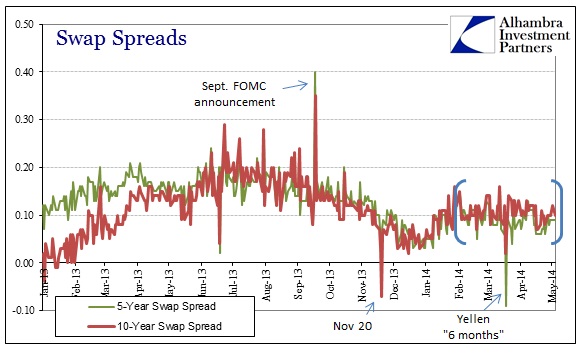

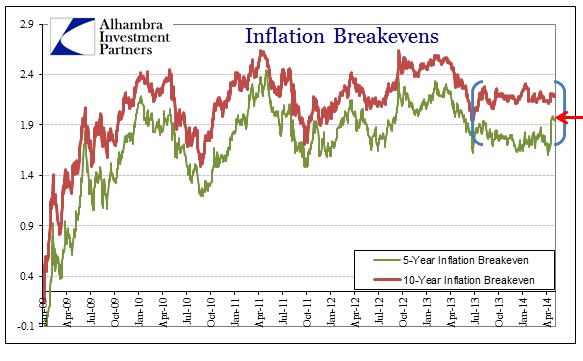

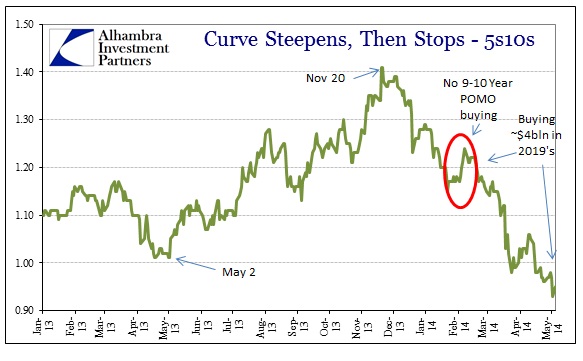

I think that is why the 5-year remains most active while the rest of the credit markets remain constrained. The prospects of lower growth and uncertain policy projections upset the driving narrative that has been in place for as long as investors’ attention spans. It has been developing for some time, as I have highlighted frequently the curious indecision over inflation breakevens (even factoring the most recent trading in 5-year TIPS). Whereas policy projections end in eurodollars nearest 2017 maturities, on the treasury curve it is somewhere further out.

We will likely see in future trading just how far “in” these reduced expectations for growth travel. It’s one thing to say that GDP may now only grow at 1.5% to 2% for the next decade, and another to say it may not grow at all this year or next. The problem, at least for these parts of the credit markets, and very much for the Yellen Fed, is that those two possibilities are not mutually exclusive and may, in fact, be one and the same, reinforcing each other. I tend to believe that is what is driving taper, in the economic sense, as I laid out on Friday.

I think credit markets are positioning for the possibility that the Fed no longer believes in an economic upside, but we don’t yet know what they believe about the downside. In either case, bear flattening more than suggests it far more significant than mainstream observations that still cohere to the Hollywood ending.

Unfortunately, it appears nothing has been learned from the Japanese experience. The correlation of low growth “potential” and blatant and steady monetarism is exceedingly high and unlimited as to geography. As long as orthodox economics and monetary “sciences” cling to the faithful belief that monetarism is neutral in the long run, they will never diagnose that causative connection. In other words, credit markets see “mysterious headwinds” for the foreseeable future, predicated on an ideological dedication to remaining blind.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@4kb.d43.myftpupload.com

Stay In Touch