Just a few weeks ago I went through the repo and credit markets with the idea that tapering QE was an act of necessity rather than convenience. Again, the orthodox practitioners at the FOMC will proclaim the economy healed when it clearly is not (an economy does not simply contract 3% and then go on its merry way) to set up the removal of UST and MBS purchases. This problem struck MBS first this year as the TBA market pipeline collapsed with mortgage originations (thanks to last year’s threat of taper).

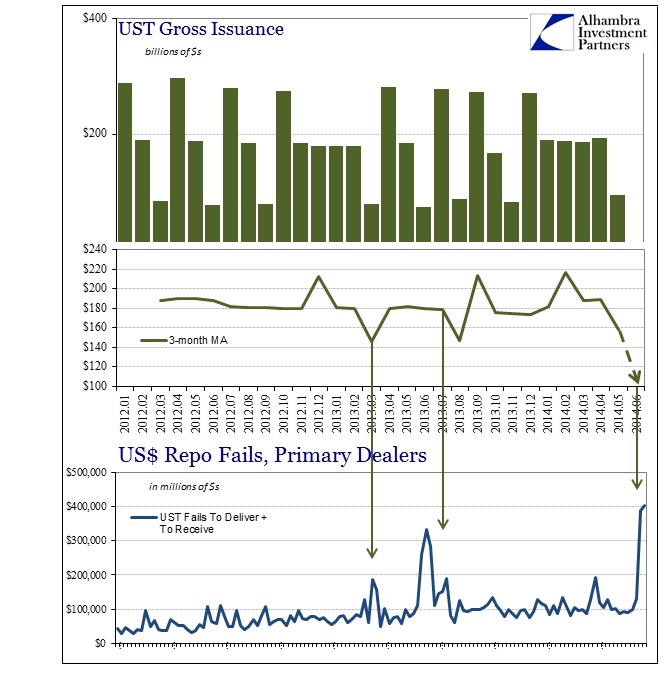

But the US Treasury has been issuing far fewer securities this year too. The net effect of lower net issuance plus QE’s removal has been scarcity, once again. In June, that inadequacy seems to have grown exponentially more difficult to navigate for funding markets, as the daily treasury report shows $336 billion in regular t-bills issued, plus an additional issue of $25 billion in the cash management series (which is highly conspicuous toward what I am talking about here – the UST does not need the cash, but it may be in response to market demand, i.e., shortage). Balanced against that has been gross redemptions of $423 billion, or a net decrease of about $61 billion in bills (on-the-run).

For repo participants, the decay of bill issuance means more pressure further down the curve, as bill scarcity will heighten the demand for notes (and even bonds). In time for that, treasury redeemed $103 billion so far in June, but issued $144 billion, changing the proportion of on-the-runs in that direction. I don’t think that was intentional nor an indication of acting in light of market preferences, rather it seems to be simply debt management. But this leaves the repo market overly dependent on notes rather than bills which have been the staple of the treasury repo market really since it began.

That is also where the Fed has been buying up UST too. Once again we see monetary policy unintentionally creating a bottleneck whereby function is impaired. The repo market is far too important to simply let this fester, and we know from last year’s experience that FRBNY’s Open Market Desk will adjust based on these kinds of stresses. Only in this instance there isn’t much for the Open Market Desk to do, only the FOMC can reduce the collateral takeout of QE.

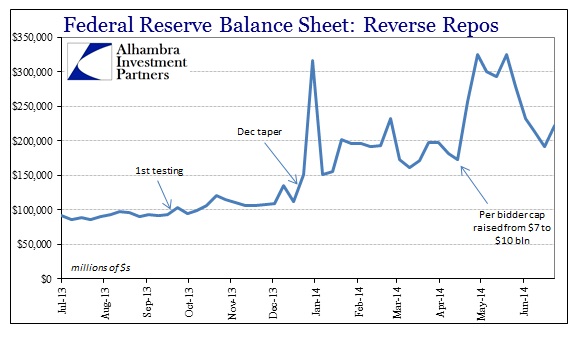

What is even more curious, the Fed’s reverse repo program, which is supposed to directly address this very problem, has seen its previously heightened usage fall away. Whatever collateral dealers have needed to maintain repo function is ostensibly not in the Fed’s inventory – which is exactly the problem I raised when the reverse repo expansion was announced last year. It all sounds good in theory, but in practice there are innumerable problems that can appear without much anticipation, and that is what markets are for. Centralized control workarounds may look like a perfect substitute in their modeled world, but in almost every case such stands very little margin for error in the real world.

So far, there haven’t been any noticeable downstream impacts from this dysfunction (looking specifically at gold more than anything), but that won’t be confirmed until more data becomes available for June (mostly, I think, in the form of lower security issuance – if dealers are having problems maintaining repo liquidity due to collateral scarcity, they are not going to be “renting” out balance sheet capacity in the primary market). That also leaves the credit markets even more vulnerable to potential disruptions, which, given the paucity of volatility lately, means a precarious position heaped with ultimate complacency.

Again, I think that is one of the primary reasons for tapering. It is clear by now that QE has failed its primary mission of the mythical monetary-driven recovery, so these net costs simply add up without much benefit (outside of asset inflation, which, as a direct aside, seems to have very little correlation with economic growth as well due to the extreme inefficiency of it as an economic tool). You take that funding market technical problem and add to it the idea of QE going while in recession, and it’s no wonder that the FOMC can’t wait to get out of dodge. Combined, these would be the end of the Federal Reserve’s credibility in both credit markets and the economy. That would be a positive result for the long run, but since such credibility (strained as it should be) is the one element animating the current paradigm in most markets, especially stocks, such a long run benefit comes probably with a high cost of transition (once again).

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@4kb.d43.myftpupload.com

Stay In Touch