Now that Janet Yellen is back in the spotlight trying to convince the world that everything is good and nearly normal, credit markets continue to persist in another frame of reference. The good Chairman might be herself convinced (though I have doubts about what she really thinks) of what she determines as a the “central tendency”, but past central tendency predictions have turned so wrongly that you can understand the reluctance of bond and dollar traders to simply submit as they once sheepishly did. The fact of circumstance right now argues, in a trend that predates Yellen’s ascension, that various “markets” expect plentiful dollars in the not-too-distant future.

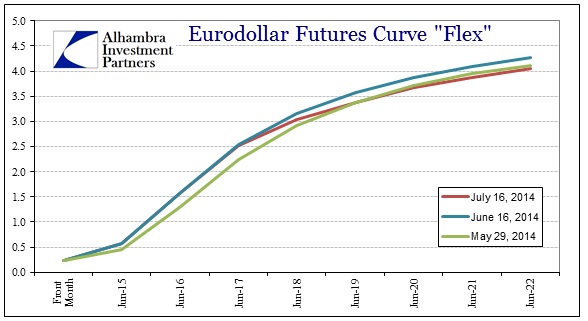

It is remarkable in the eurodollar market to see that course take shape largely since November 20 (when the Fed altered its Open Market Desk behavior in the 10-year). More recently, there was the sharp appeal to eurodollars and IR swaps to counter bad positioning as the UST curve moved back lower around the end of May (strike one against Yellen, as UST shorts that were “encouraged” by so much FOMC talk were taken out on a stretcher, with max pain appearing on May 29).

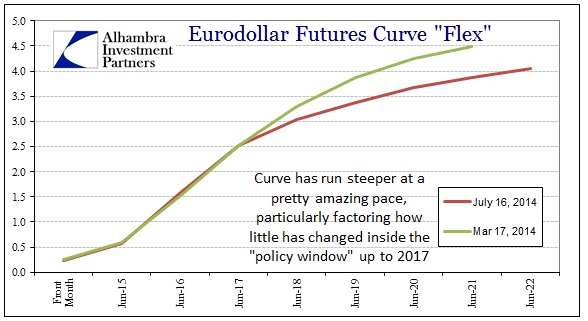

Since that momentum event, the eurodollar curve has run back to where it was in the shorter durations but, once again, conspicuously flattening further out. In wider context, back to the middle of March, the dramatic and remarkable change in the curve out past 2017 is surpassed only by the utter lack of movement up to 2017.

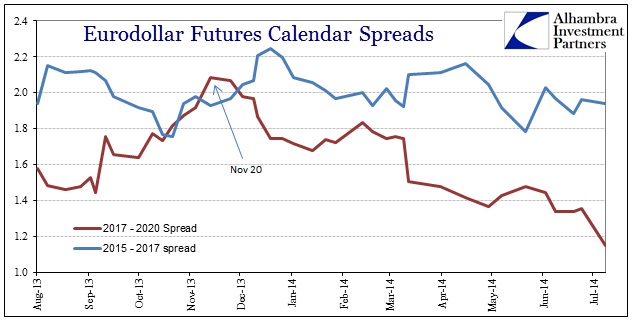

In terms of the curve shape (which are calendar spreads here), the relentless nature of the flattening, again dating to November 20, is telling a story far different than the cajoling and moral suasion that pervades mainstream commentary. If there is “normalcy” in our future, it looks increasingly likely that will pertain only to the reach of the Fed. No matter how much “they” keep stressing an interest rate hike and better days ahead, there is “inordinate” pessimism in the actual markets about the ability of the Fed to transition (which includes an economic assessment) and at best indecision about those rate increases (at worst, complete disinterest in those infamous dots).

Going all the way back to the violent credit event in the middle of last year, eurodollar futures have not much altered the view of policy “normalization” despite everything that has taken place since then. But beyond that “policy window” up to 2017, faith in the Fed has rapidly and steadily eroded here. I don’t see how you can reconcile what is taking place in dollar and credit markets with the FOMC’s positions on anything related to money and economy.

In broad terms, eurodollars now, and since November 20, are positioned for “plentiful” dollar availability. That is the opposite of a robust and growing economy which would provide a massive increase in usage of funds away from financialisms. In other words, if the Fed had created that “better” world they have talked about since 2007, then traders would be looking for “better” opportunities to place funds. Instead, they are going back into the same “bunker mentality” that has pervaded this period of economic deficiency – the more the Fed tries to change all that, the more nothing has changed.

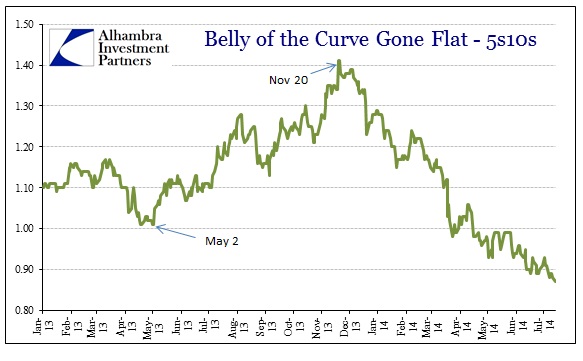

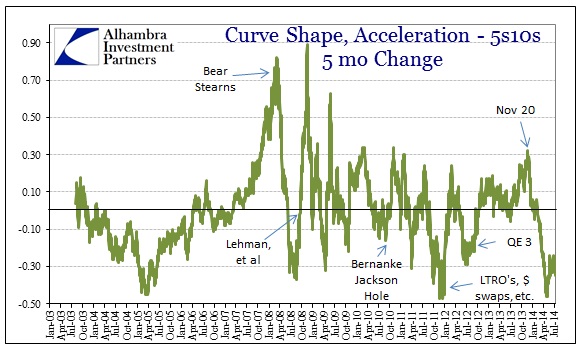

The noticeable flattening is not limited to global funding markets, either. The treasury curve continues to take cues from eurodollars (and other funding markets, like repo). It began in the belly of the curve, again timing right at November 20, 2013. The 5-10 year spread has been steadily compressing right alongside eurodollar calendar spreads in the same general positions.

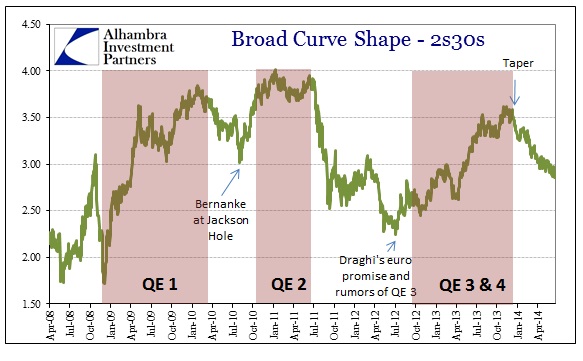

The broader curve, out to 30 years, took notice only as taper became a real event rather than remain a threatened policy “surprise.” To this point, the 2-30 year spread has followed almost exactly the same pattern as around previous QE endpoints.

Nothing has altered that track more recently, despite what appears to be a steady drone of optimism from policymakers about how resilient both markets and the economy are believed to be (according to their ultimately disjointed perspective). What is perhaps more revealing of the actual market positioning, however, is the speed at which this bearish flattening has been accomplished.

Again, this kind of “market” behavior is related far more to general and rising distress than “normalcy.” With a lot of optimism about the lack of curve inversion recently taking so much discussion, I fail to see how that relates to these conditions where the short-end (represented by eurodollars here) is unmoved by pretty much anything big or small. There is no possibility for inversion because that market piece is pretty much dead in terms of anything informational.

The rest of the curve, out away from the heavy and intrusive reach of Chairmen and their orthodox planners, is acting very much like an inversion in fact if not appearance. Furthermore, it seems as if timeframes have grown more compressed post-crisis. Whereas the curve began toward inversion around late 2005 and into 2006, leading the Great Recession by well more than a year, dysfunction in flattening, particularly as it related to discrete QE episodes, predated “trouble” by far less time.

Whatever you want to make of all this, none of it conforms to the ideas being put forth by the Fed and Chairman Yellen. The FOMC is attempting not only something unique in history, it is doing so during conditions that have completely failed to match prior expectations and predictions. That is not just starting blind and behind, it is a paradigm shift that hasn’t resonated enough in DC and NYC – at least not yet.

The one primary market “support” throughout has been belief (unearned, at that) the Fed would live up to its own standards and proclamations at some point. Now they are taking away that “support” before ever achieving anything of note, instead leaving behind quite a mess.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@4kb.d43.myftpupload.com

Stay In Touch