This may be a more globally universal problem than specifically limited to just Japan, but since the Japanese have been encapsulated here by far the longest it has lost almost all meaning. At some point, there has to be a penetrating numbness that becomes downright debilitating which is why a degree of sympathy is called for despite it all. There is no other way to explain why democratically elected governments would for a quarter of a century do the same thing over and over and over to absolutely no avail.

I’ll save that ugliness for another post; for now just the figuring. As is usual, GDP has become as volatile as “market” prices used to be. There really is no counting them from one quarter to the next and expecting consistency anymore, so any interpretations laid out here come with a government-defined expiration date. That is as much about the false pursuit of precision in a complex system, so it pays to stay away from the short-term changes and follow trends and trajectories.

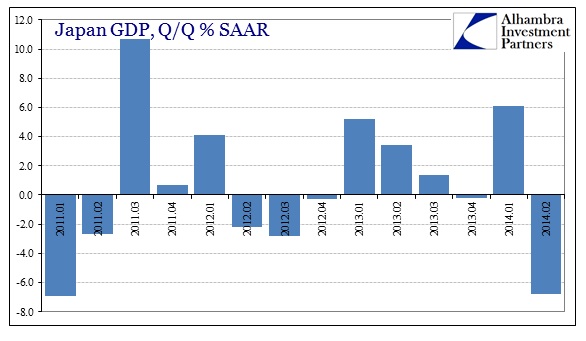

No matter how much is further revised down the line, the second quarter can no longer maintain the illusion of the QE-driven recovery. Sure, expectations are continuing toward growth in the second half, as they are elsewhere, but even the most staunch defenders of the BoJ and Prime Minister Abe have been shocked into something like doubt, if not the edge of disbelief.

That should have been no surprise given that it has been well more than a year that the initial expectations for QQE (as they call it at the Bank of Japan) were laid out: recreate Japan Inc via export-driven favor in devalued yen, leading to a higher labor utilization and ultimately wages driving spending. There are no points awarded here for getting the supply side first, as even in the right order the central bank fails to understand the nature of nominal changes vs. true wealth.

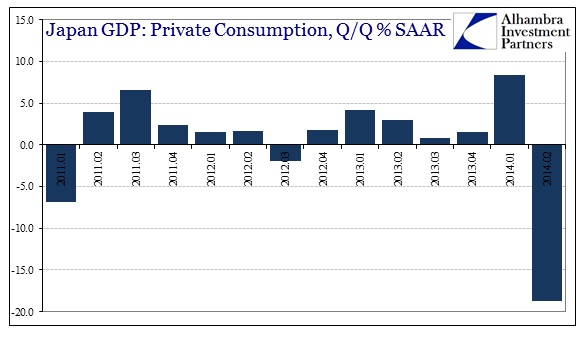

Essentially the second quarter more than offset the first, but that isn’t even the worst of it. Taking the GDP approach by parts, private consumption fell by the largest amount in the data series, much greater than even the aftermath of 2011’s tsunamic implosion.

Household consumption simply collapsed, and at a far worse comparison than even after the infamous 1997 tax increase (why, again, was this supposed to be different this time? It was different, after all, just not in the direction faith assumed).

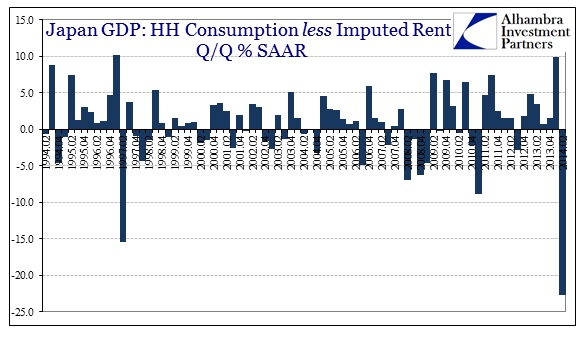

Where household spending, less the Cabinet Office’s imputation for owner’s equivalent rent, was up 10% in the pre-tax quarter, it dropped 22.7% thereafter. That creates something of a mismatch, however, as private demand forms a high proportion of GDP calculations. With Household Spending contracting to such an immense degree, a -6.8% estimate for GDP actually seems more than a little tame.

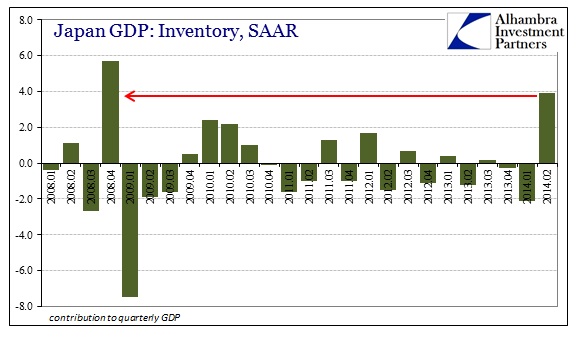

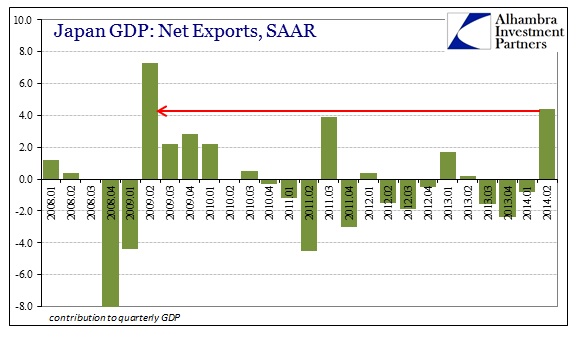

In that respect, the GDP figure was actually “saved” somewhat by inventory and net exports, but in the manner that would create no silver lining in this ubiquitous dark cloud. Rather, through the quirk of measuring second derivatives, inventories and net exports “added” 3.9% and 4.4% each to GDP, respectively. These were both “positive” contributions to a degree not seen since the Great Recession. Absent them, GDP would have been around -15% or at least something closer to the -12.5% “contributed” by household spending and private consumption.

Taking the inventory piece, clearly there is volatility surrounding the tax hike but that does not alone explain why inventory would grow so far so fast afterward (even factoring in potential second derivatives). That is, unless businesses were expecting a far less dramatic slowdown in the months after the tax change. That would seem to suggest that Japanese businesses, like their American counterparts, are far more attuned to economists’ projections than their customers. That leaves a very large overhang to either generate a drag on the coming quarters or to be revised away by future “estimates.”

As bad as the inventory problem is, the situation in net trade is actually worse. The only reason GDP contributions here were so highly positive is that imports were less worse in Q2 than Q1 where they were of epic proportions (again, contrary to all orthodox “laws” regarding currency devaluation). That does not change, however, the fact that Japanese trade is still imbalanced to such a highly impoverishing degree, only that second derivatives matter more here than in the real world. That is plainly evident in contributions of trade from the first quarter which subtracted such a minimal amount despite the disaster.

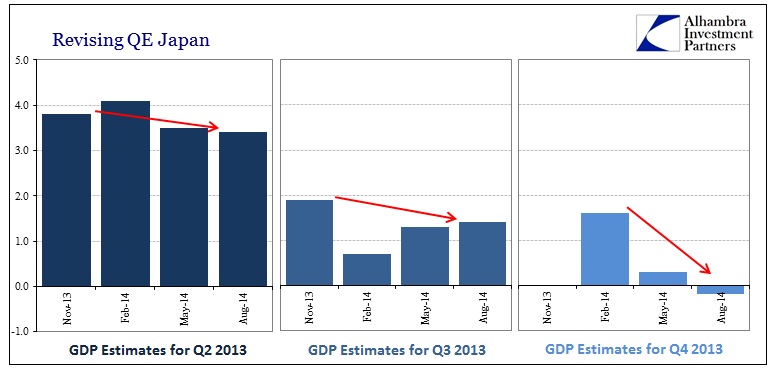

In terms of trajectory or trend, I think it pretty clear that economists have once again misjudged the impacts of “stimulus” to a high degree. That includes, as it turns out, all the quarters so far under QQE. The latest revisions included with the August preliminary figures for Q2 2014 show a rather stark difference than just six months ago. GDP growth in the last nine months of 2013 (those under QQE) have all been revised downward.

It is the fourth quarter that should gain more attention. When first released in February, the initial estimate of 1.6% was somewhat disappointing to expectations of 2+% in continuation of what was believed to be growing optimism about Abenomics. Inflation, poorly defined here, was once again positive and it appeared as if all was going to plan, though there were a few cracks (notably trade) that were cast off as lagging indications that would eventually come around. If that disappointing 1.6% had instead been released as the -0.2% that current figuring says is correct, it would have totally changed the complexion of analysis surrounding such optimism and likely been thought of as a disaster (though for “markets” it may have actually pushed the Nikkei to new local highs given the perversion of asset prices and their relation to what the Bank of Japan might do for an eleventh time rather than the economy).

But in the context of current estimates as of August 2014, the Japanese economy has contracted for two of the past three quarters, with the latest quarter more than canceling the positive number in between. In short, Japan has at least stalled out for more than nine months now, with GDP down from start to finish. And really, if you go back one quarter further to Q3 2013, the trend has been lower from now a lower starting point. But that is not a static procedure, as redistribution has actually made the Japanese system far more impoverished for the trouble – and now to no calculated gain.

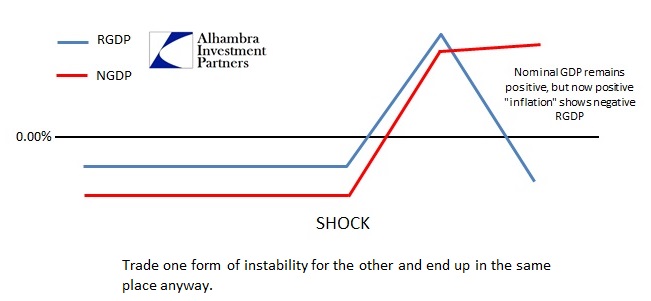

Given the second derivative nature of GDP, there is probably a good chance that Q3 comes in positive, just as Q2 did in the United States. However, as shown here and elsewhere, these are nothing like recoveries. They are simply the accumulated and highly corrosive redistributions of central planning trying the same thing to greater and greater command. In Japan, it seems more likely that my “template” for the inflation “shock” of last year is becoming reality. Simply trading one form of instability for another still ends up in the same place.

It may appear to work for a fleeting moment, but the negative factors catch up eventually while leaving a much weaker base upon which to attempt to build the next “cycle.”

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@4kb.d43.myftpupload.com

Stay In Touch