Statistics are notorious for being worse than liars, according to cliché, but under many circumstances there is more than an element of truth to that. The latest revisions to the July revisions are not quite the liars’ paradox (everything I say is a lie; that first statement is true) but there is something amiss that is missed in the narrow focus on what happens between quarters. Disassembling the pieces bit by bit after the major revisions in July shows that while growth rates look better recently, the economy is now smaller than previously believed.

Which is the “better” situation, where growth in the most recent quarters is assumed to be higher? That might seem to be so but then you have to look at the statistical impacts of what are known as base effects – particularly given these massive revisions that wholly reshaped economic history during the QE’s (still without much reason given for doing so).

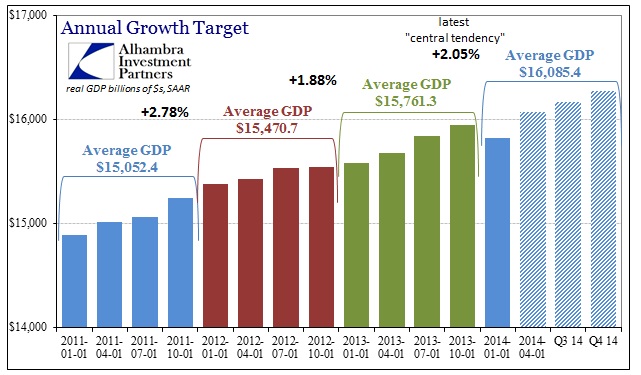

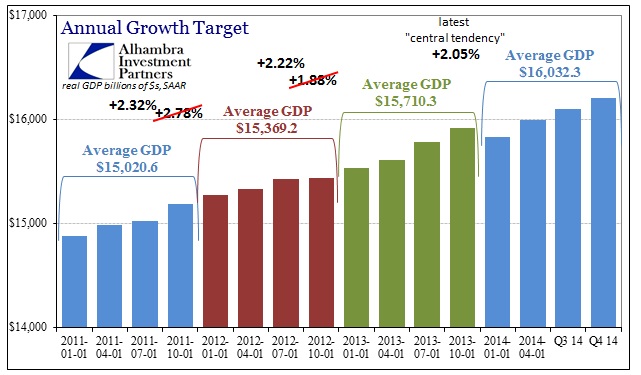

Before the July reworking, GDP’s trajectory looked like that shown above. Growth slowed from 2012 into 2013, with a very problematic expectation for growth to reach the Fed’s “central tendency” of 2.1%. With 2011-13 now looking far different, the trajectory of GDP has been reworked into a different set of growth rates.

Significant growth in 2012 disappeared and almost all of it was added to 2013 instead (which, however, now shows a steady and consistently lower growth path from 2011 through 2014). In the individual quarters remaining of 2014 to reach that “central tendency”, needed growth is not nearly as ridiculous as it would have been under the prior assumptions.

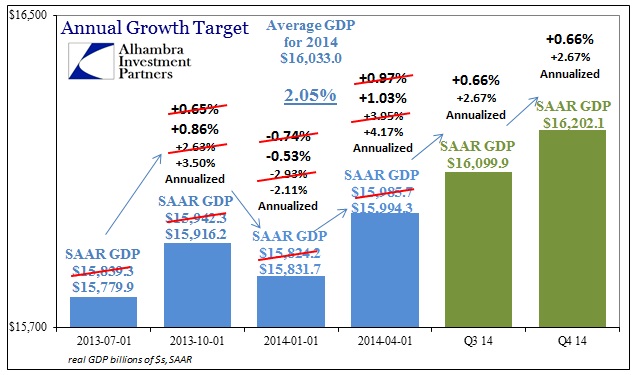

Before July’s revisions, where Q1 was at -2.93% annualized, it was looking like GDP would have to advance at a compounded annual rate of more than 4% in each quarter just to strike that reduced lower bound of the Fed’s central tendency projection. Under current GDP assumptions, the last half of 2014 will only need 2.67% in both quarters.

Of course, that is a very low standard to reach, and the cries for 4% and better have been a constant feature of the beginning of every year going back to 2010 (much more realism resided in 2009 when humility about so many things, especially monetary potency, was close at hand). But all that misses what actually took place under the revised regime.

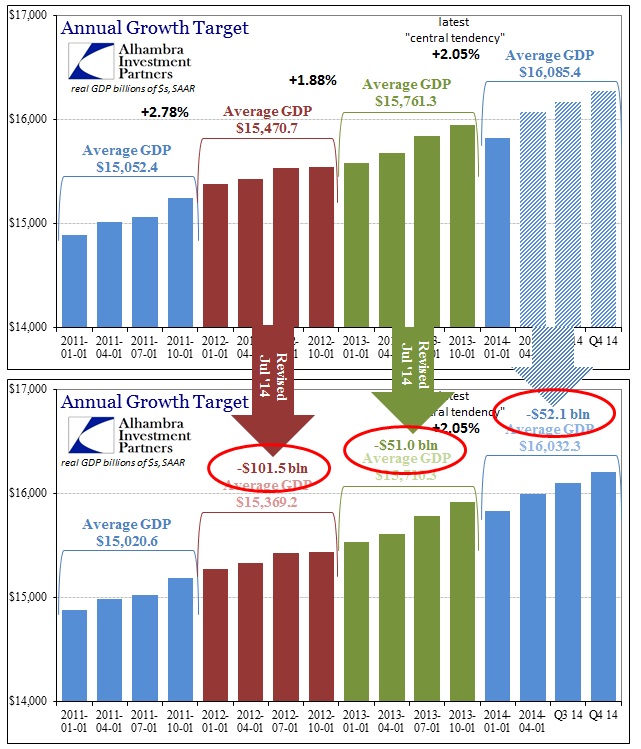

Looking at the pre- and post-revisions more closely, you note that despite “better” growth more recently, the average GDP figure needed to attain that 2.1% growth bound is actually $52 billion less now than before (and that is actually a greater gap by Q4, -$63.2 billion). The reason for that is because so much GDP was lost in 2012 (and some in 2011), and in a compounding situation that figures a lower trajectory that diverges more and more the longer the growth rate remains fully substandard. Since more than $100 billion was erased from 2012’s GDP, that meant despite 2013’s upward revision in growth rate it wasn’t enough to re-establish the prior trend. It is far better to get growth earlier than later, a fact left out of the current narrative.

Going further in time, even the assumed much better growth after the middle of 2013 still leaves the economy smaller than it was otherwise believed. That is itself a problem, again compounding “errors” explode over time, but it is particularly acute in the situation we find during this “recovery” period. In essence, the recovery action since 2009 is just a series of reduced compounded growth rates that continue to bend the economic trajectory lower and lower, further and further away from what is needed to be counted as a healthy system. That started with the stark asymmetry of the Great Recession itself, with a second “bend” in 2012 that, with these revised GDP figures, actually looks even worse now.

The net result of all of this is not just misleading interpretations and all-too-comfortable extrapolations (especially with another polar vortex due in September and the Farmer’s Almanac calling for another harsh winter?) it is a serious economic problem that goes way beyond the statistical inaccuracies and tendencies, lately, to move around so much.

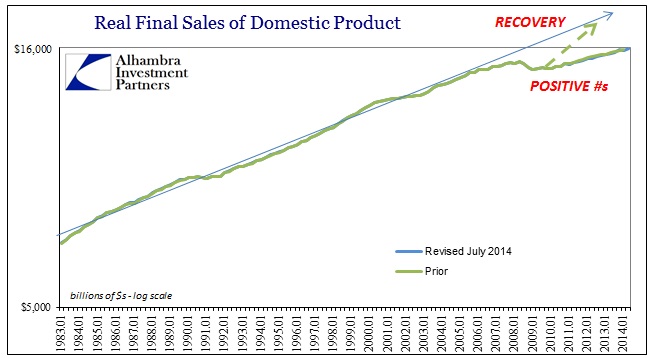

It’s difficult to see it in the chart above, but the revised figures at the upper right corner for real final sales are now running below the prior estimates due to the smaller economy. That simply means, despite whatever growth rates recently, the distance to what would be considered an actual recovery is that much greater than believed. That might be the final slogan for QE and monetary activism: leading and leaving us further astray.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@4kb.d43.myftpupload.com

Stay In Touch