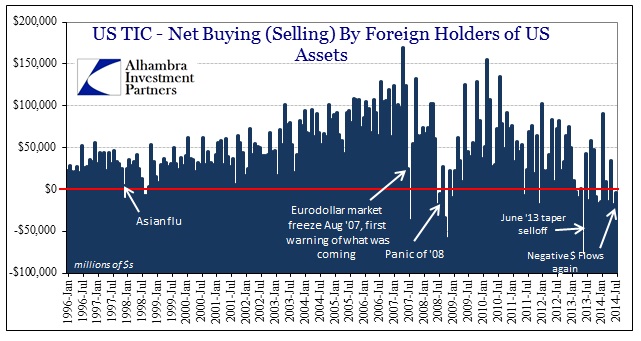

For the conspicuous lack of drama surrounding currencies in 2014 vs. 2013, there does not seem to be much by way of actual change. Perhaps the only real difference this year (through July) compared to last is how central banks are responding to what they perceive of dollar availability. It is entirely a different perspective of “private” markets, though, in that there is a clear diminishment in “excess” dollar supply.

To some, their attention immediately turns to lower trade volumes. I don’t want to totally dismiss the lack of trade expansion out of hand, especially from an absence of actual economic progress in the US, but dollar flows in the eurodollar system (some call it petrodollar, but that is far too narrow to really apply) are about finance more than actual trade – and that is the problem.

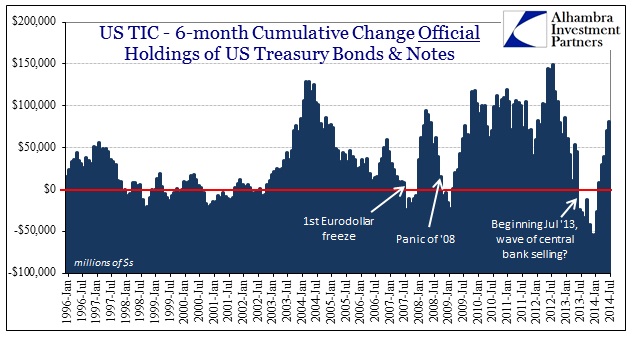

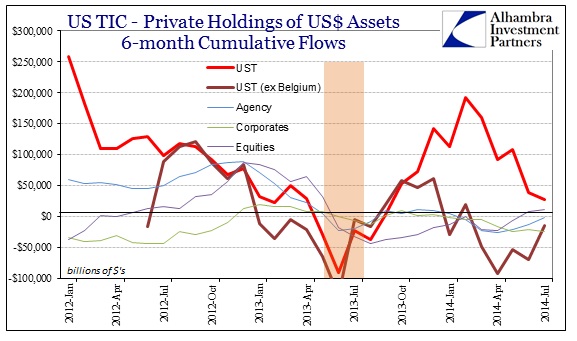

As I mentioned, the chart immediately above shows just how much central banks (the “official” sector) have been “able” to reverse the dramatic dollar issues tied to then-Fed Chairman Bernanke’s taper threats. While most of the developed world quietly shrugged in the apathy of the “recovery” and plausibility of “global growth”, that only hid what was really a violent and ugly episode for most global participants in the eurodollar schematic. As is seen below, not much has changed since then.

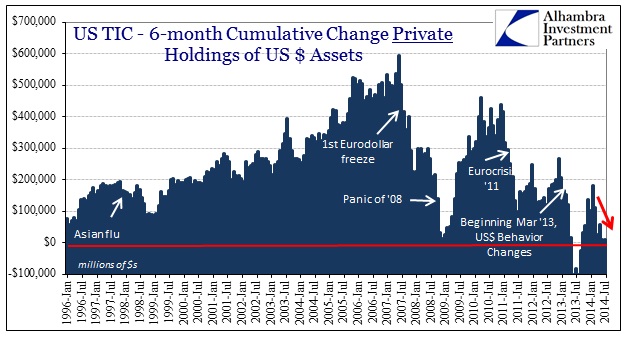

The private sector continues to disfavor dollars, or, to put it more precisely, is far less assured of their availability. And even that is understating the major shift that occurred in 2013 (that traces back actually to 2007) because of the anomaly in global banks likely transferring their derivative operations to Europe (and Belgium, more specifically, where Euroclear resides). That one-time operation has actually made it appear as if the private dollar “market” was once again enthralled when it was nothing of the sort.

Last year’s selloff and dollar “tightening” marked not just a massive shift in the dollar (though the dollar here is just a unit of account used globally) but what appears to be something permanent. This has very serious implications for not just global trade and global finance, but any “dollar” market in existence. As I showed the last time when speaking about dollar problems, reduced dollar participation due to whatever reason is the same thing as narrowing the exits for whenever selling pressure might arise (and it will eventually).

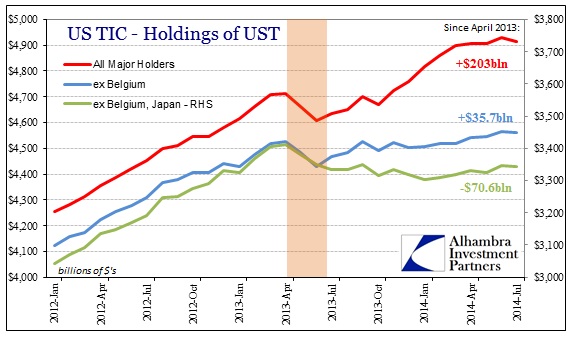

Again, however, the change in dollar behavior is actually much more drastic when accounting for Euroclear (deep red line above vs. red line). Without the Belgium interference (what looks to be a transfer of securities, not buying of them), dollar buying in UST, and thus overall, has been totally subdued after the taper-induced selloff.

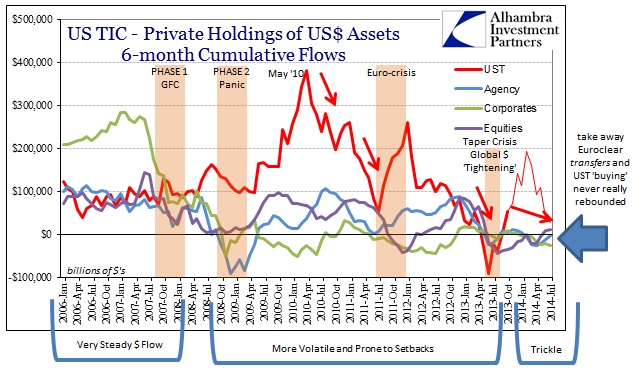

With a longer-term perspective it is clear that dollar participation is almost non-existent when adjusting for Belgium. You only need to glance in the crisis period above to see what happens when you combine a lack of dollar participation with negative sentiment turning onto fear. As dollar shortages spread in 2008 (especially heading toward Phase 2), participation dropped and so did dollar asset prices of everything.

Investors may be indifferent about the lack of negative sentiment today “thanks” to central bank action suppressing what is really natural instinct about prudence, but that does not mean we should not be aware of the huge shift in dollar participation. There is a whole other discussion about whether that is supply (eurodollar banks) or demand (changing the dollar as a reserve currency), but it simply cements the notion that the eurodollar system as it existed prior to August 9, 2007, for all intents and purposes ended. We have little inclination yet, even seven full years later, how that will be resolved. May and especially June 2013 were another seismic swing in that process; nothing having altered that this year despite the perpetually optimistic central banks.

Click here to sign up for our free weekly e-newsletter.

“WEALTH PRESERVATION AND ACCUMULATION THROUGH THOUGHTFUL INVESTING.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@4kb.d43.myftpupload.com

Stay In Touch