There may be something to December after all. It was credit markets that shifted downward (bearish yield curves and credit spreads) dramatically around the end of November and the first few days of December. Given the persistence of large players moving credit and funding markets, this may not be all that hard to fathom with the close proximity of credit desks next to, say, lending desks or high yield trading. If high yield issuance is any good proxy about marginal conditions, the erosion there is as much about an economic trend as it is some semblance of restoration of fundamental sanity.

It is too early to define the shape of the economy right at this moment, though needless to say that there is far more uncertainty than there was even a few months ago – just before the Christmas letdown.

The Dow Jones Industrial Average plunged more than 350 points on Tuesday after weaker-than-expected data on durable-goods orders and disappointing earnings reports from bellwethers, such as Microsoft Corp. and Caterpillar Inc. sparked fears that economic growth is slowing.

Durable-goods orders fell 3.4% in December, raising questions about whether businesses are really ready to ramp up investment in 2015.

This will all be very “unexpected” to economists who have spent the better part of 2014 vehemently assured about that growth trend. In the case of durable goods, there was certainly a pickup in mid-year, but any extrapolation from that was always misplaced since it was the same mini-cycle that plagued 2013. What looked like growth to those who pay no attention to context was instead artificial, and thus unsustainable, in every way.

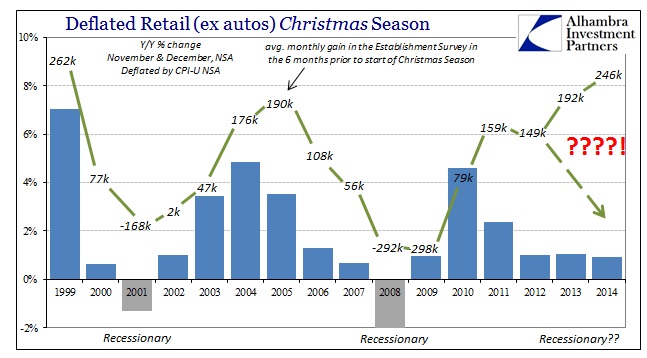

The main economic narrative is derived from the FOMC, a policy body that itself was forced to admit that there was no true expansion in wages last year. Given cost pressures (as opposed to “inflation”), the lack of wages acted repressively on economic activity, a major factor in what we are seeing with these unsustainable mini-cycles. A real economy produces wage growth, regardless of some mythical “slack”, therefore the lack of it measures the true state of progress or deficiency regardless of what GDP says.

It wasn’t just energy either, as that has become the excuse du jour with anything that goes wrong lately.

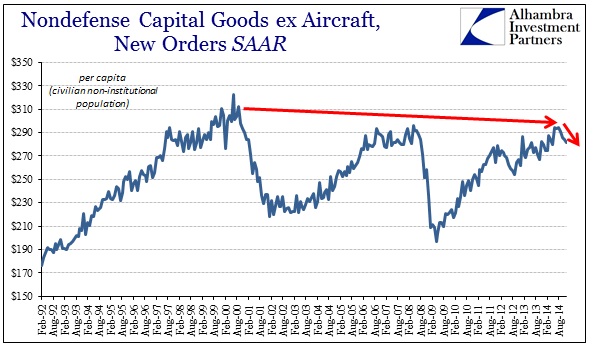

There was also weakness in a number of areas, and a key category that serves as a proxy for business investment plans edged down 0.6 percent in December after a similar decline in November and a 1.8 percent fall in October.

Even if the oil and gas sector was responsible for the decline in capital spending, that only confirms the artificial state of any prior advance. A true economic recovery or growth period would be broad and durable enough to withstand any slowdown in any single area. If the end of the artificial energy “boom” is enough to push the economy off its assumed track, it was never there to begin with.

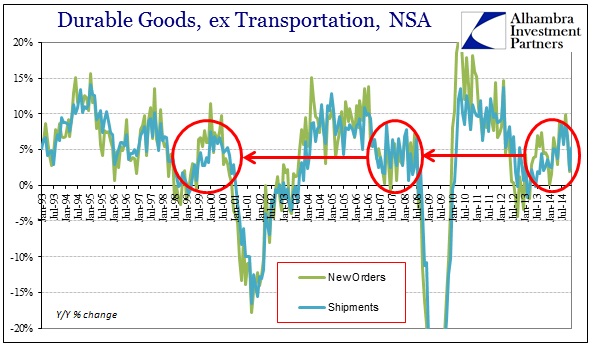

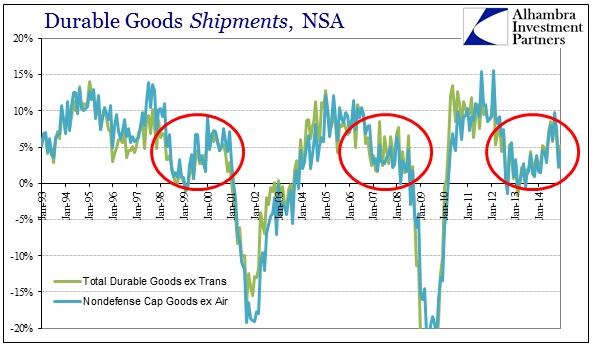

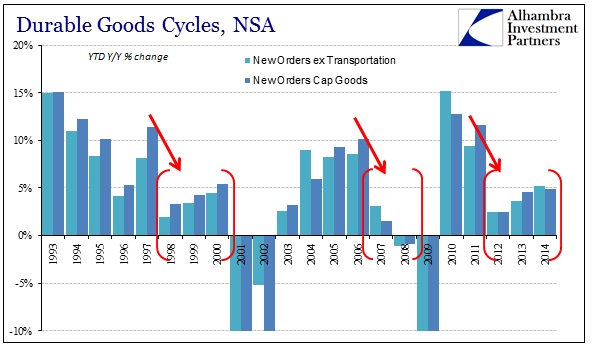

What’s remarkable is that we have seen all this before, increasingly looking like a third repeat of prior behavior. While there are numerous similarities with the 2007/early 2008 period, including the sharp, artificial runup in energy before its collapse, it is actually uncanny how much the last three years echo almost exactly the global slowdown after the Asian flu in 1998.

There are certainly mini-cycles contained within those years, but overall this shows the elongated cycle quite well. I think conventional “wisdom” about the last two years of the 20th century are colored far too much by the dot-com bubble, nobody seemed to notice the actual economy as it was all just too much fun to stop believing in, because when you pull it apart the slowdown in global activity was broad and serious. It was repeated again in 2012, as the last two years since that slowdown have been rife with confused economists and “unexpected” starts and stops – not to mention significantly higher equity valuations.

This time, however, the global slowdown has fewer places to hide. Perhaps we can “thank” monetary policy for that, highlighting deficiency wherever “extraordinary” policies have been proclaimed as highly “necessary.” In other words, the very fact that a central bank has “had” to institute something as disruptive as QE is not much of a solution but rather a marker of everything wrong. I do think that is the evolution of at least credit market thinking on the subject, viewing the decrepit state of the actual economy now more appropriately; moving in the “wrong” direction. There is, again, perhaps something to that sharp bearish turn in December.

Stay In Touch