The rock of the Swiss banking position was its still-heavy relationship with the global “dollar”, a proportion of funding that diminished only somewhat post-crisis. The hard place was the euro, whereby pegging the franc to it meant the SNB was balancing euro problems with banking disproportion. It seemed like a good bet, for orthodox monetarists, in September 2011 because they figured whatever the ECB did later that year would “work.” I have little doubt that the SNB never expected to be stuck with the peg three and a half years later and that the lack of global revival would heighten that currency impropriety as “dollars” on offer slacked so precipitously with it still in full force.

Whatever reasons now colored by hindsight, there is no doubt that the Swiss takedown of their own financial mechanism, the peg, has occasioned relief in the wider “dollar” system. Ever since the deepest penetration of disorder, in the week between the peg’s removal on January 15 and the further disquiet that immediately followed until January 22, the global financial world is, on the whole, a much calmer place.

This is not to say that everything is “forgiven” and that the clouds have completely parted letting in the full sunshine of propriety and balance, only that the immediacy of dragging funding irregularity has been at least temporarily set aside.

Given the esoteric nature of all of this, and the fact that very few people seem to be even aware of these massive problems (which include systemic liquidity of all types) it is not difficult to discern why various “authorities” might actively seek the reopening of that disorder. In this specific case, there was a brief news item today tucked away mostly in “foreign exchange” news for forex traders where the Swiss Finance Minister officially discussed discussing the possibility of a new peg.

Of course, there were no details about at what level or even what specifically is driving this search for a reactionary move, but it almost does not matter as forex markets are already deeply unsettled by all of this (where funding markets, paradoxically, have been settled). While it is just speculation on my part at this point, I would imagine that any such “consideration” is being driven by economic “consideration.” In other words, removing the peg already contained more than a fair amount of economic risk, and I don’t think it unreasonable that the growing clarity of an emerging economic downside would lead to the exploration of a return currency trip.

That was always the tradeoff even from the very beginning of this new franc paradigm, as the disadvantage of keeping the peg (funding risk) was far more immediate, tangible and dangerous. Now that the immediacy of the funding problem has passed, it is very much human nature to think it is over – especially if that downside begins to seriously bite.

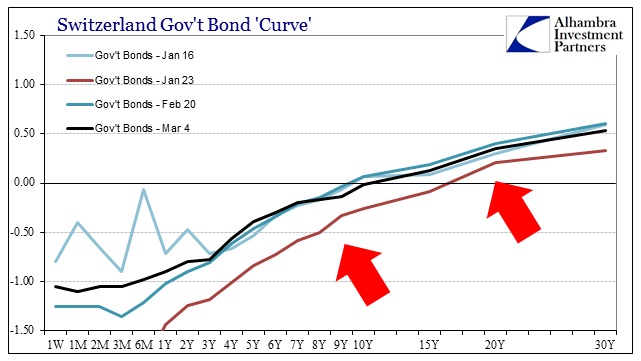

Again, mistaking calm for “normalcy” is both common and foolish. By no account is the Swiss “market” back on its feet, or even close to such a point where something like that looks likely. While the Swiss bond market is certainly better than the absurdity of January 22 or 23, that isn’t really saying much apart from, again, immediacy.

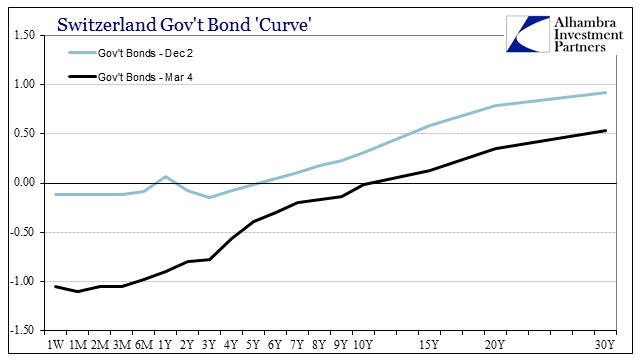

The Swiss Government curve is well above the lowest point, but not really that much inseparable from January 16 when things were really, really bad for the franc. And in comparison to the beginning of December when all this funding retrenchment really picked up, the Swiss are surely not anywhere out of danger as you can see easily below.

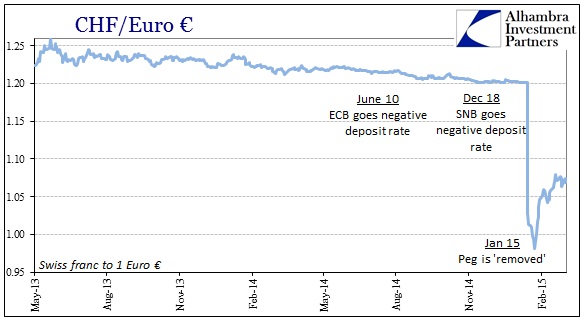

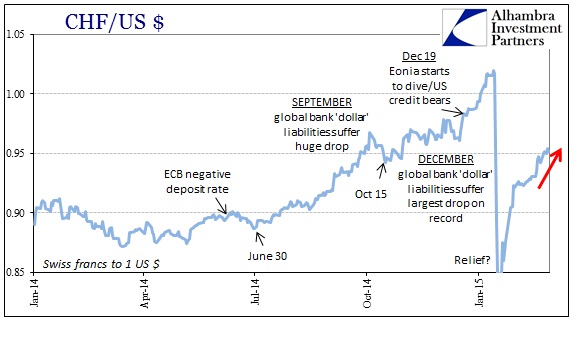

In fact, despite the “relief” of the franc against the “dollar” upon January 15 the trend has picked up again in the “wrong” direction. While it doesn’t show as much versus the euro, where the exchange is still only about 1.07 instead of the 1.20 peg, the cross of the franc to the “dollar” is again becoming a concern.

As it is, the franc/”dollar” is already back above (below) .95 which was the level around October 15’s global illiquidity spot. The last thing the Swiss, or the rest of the world for that matter, needs is an official disruption pushing funding problems back to the forefront. Hopefully, there will be further clarification about what the suggestion of a renewed peg not only might mean in specificity, but also whether it was a serious proposal in the first place. As it is, it may not even matter since the franc is already moving backwards once more.

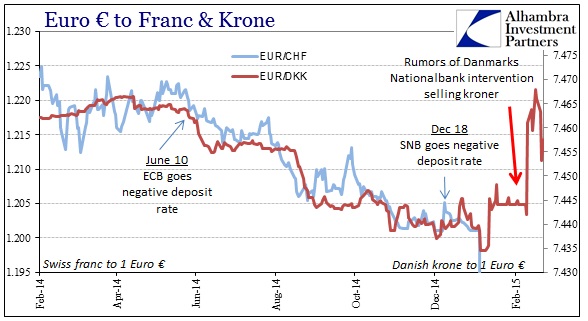

As if to put more emphasis on that recently, even the Danish krone has started to converge with the franc. The fact of their dramatic divergence was that the “dollar” problem was unique (among the two) to Switzerland, so a possible convergence is likewise a concerning signal of possible returning erosion.

Stay In Touch