We ran into this complication during Bernanke’s partial “confession” about his brand of QE, namely that what failed was not the power of the Fed overall but rather to extend the power of the Fed beyond merely the financial. He is trying to claim that QE wasn’t really impactful after having totally assured anyone who would listen contemporarily that it was beyond potent. The evidence in the US suggests this dichotomy where asset bubbles are tracing to these financial susceptibilities but that asset bubbles aren’t much help especially those not directly within their line. For all that was amassed under its umbrella, we still cannot tell if the economy in the US has recovered while it now teeters close to another potential abyss.

The experience of Japan is well on its way, with Nikkei 20,000 celebrations aside significantly downgraded wages, to likewise proving this limited range. It is entirely too early in Europe to suggest definitively about that economy, but all indications so far at least provide more evidence that QE does indeed have enormous and distortive financial properties.

In Europe, QE has been so powerful that it has already been scaled back without much applause from the usual commentary.

More than one quarter of the securities in the Bloomberg Eurozone Sovereign Bond Index have yields below zero, data compiled by Bloomberg show. France’s five-year note yield fell as low as minus 0.004 percent on Friday.

As part of its quantitative-easing plan, the ECB has pledged to buy 60 billion euros of assets, including government bonds, on a monthly basis through September next year. The central bank reported buying 41.68 billion euros of sovereign debt in March. Policy makers are next set to meet on April 15 in Frankfurt.

In other words, March’s buying pace was only about two-thirds the intended value, even factoring that the ECB didn’t start right on March 1. Despite undershooting intentions, these monetary fingerprints are still all over the continent.

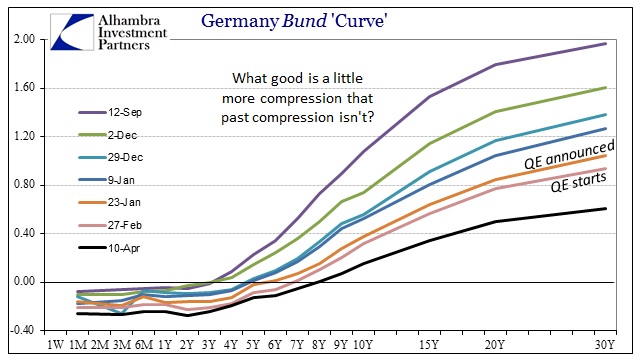

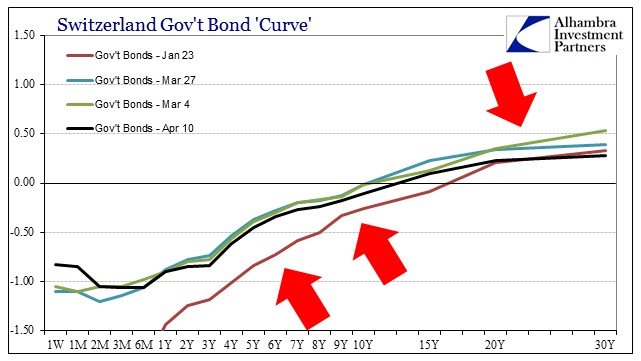

Germany’s bund curve has depressed even beyond the depression levels that have existed since December. There is clearly an effect, as even the 10-year moves toward zero indicating the fact that the ECB has almost eliminated (what was left of) the time value component of financial benchmarks in a matter of just months. And it isn’t just Germany, as even the Swiss, who were for a time seemingly delinked from this mess, are seeing the same longer end compression even though the ECB doesn’t apply and the SNB delinked from the euro almost three months ago.

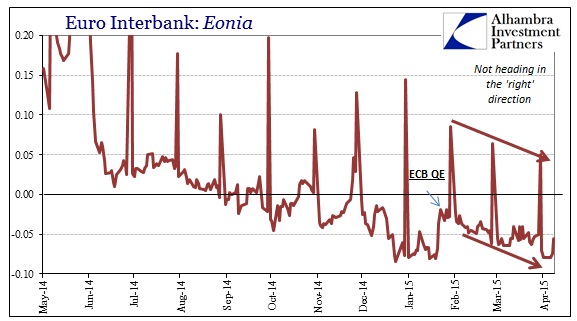

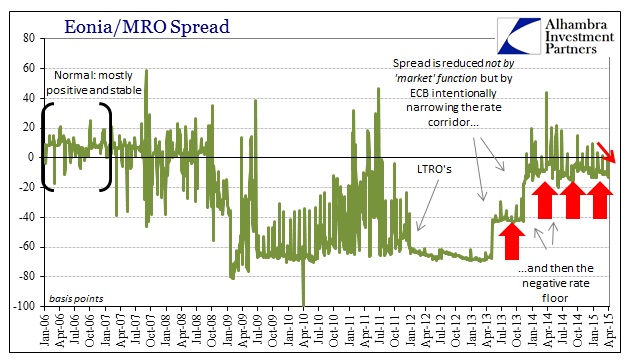

Further, interbank rates in Europe continue to slide, too. Eonia keeps drifting lower into negative rates, a condition that actually and significantly denotes the opposite of what the ECB intends. In other words, there isn’t as much ambiguity in a negative Eonia as there might be in a negative 7-year German bund.

Eonia is an unsecured rate which is supposed to anchor to the ECB’s MRO corridor midpoint, which is a secured, repo rate. To have a deepening negative spread indicates, again without vagueness, that “money” “markets” in Europe remain profoundly unhealthy and are getting more so despite the “tonic” of QE.

I think from there we begin to really understand where this mainstream theory about QE falls apart. It is simply assumed that any “portfolio effects” based on heavy rate repression of all varieties will take place. And there is no doubt that some take place, though it is not at all clear they do so in the manner and variety that monetarists intend or want. The draw of the various government bond curves in Europe more than suggest that QE does have power on this first part, but Eonia more than suggests that it isn’t a governable influence.

So we are still within the realm of finance and QE has already been rendered more and more uncertain about its downstream impacts. From that we can easily infer that the influence upon finance at the front door does not directly flow out the back; instead there are innumerable distortions in any flow or processes that the “portfolio effects” are degraded well-before any real economic impact. To be sure, even monetary practitioners acknowledge the possibility, but they downplay it as minor and unrelated “costs” to undergoing such “stimulus.” What they should be doing is reading this process from QE into finance and out into the economy (if it ever gets that far, with so much of this more than suggesting that financial distortions simply bounce around inside finance without ever much leaking out into the economy at any point) as so unclear as to be unable to at least make a sound judgment about potential benefits to what are becoming very known costs. You can insert any joke about dart-throwing monkeys here and it would be consistent with this generic program.

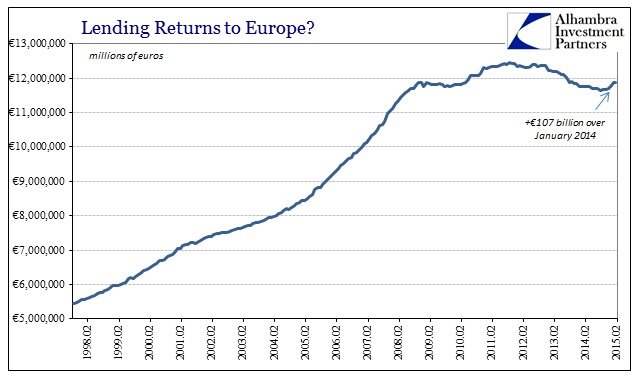

Here again I think that is almost purely observable in the trajectory of lending in Europe. I don’t make as much of a distinction between QE and everything else the ECB has been doing, I do think there was at least a break in first turning last June to a negative rate floor. In that respect, QE and everything in between is a continuous attempt at massive manipulation all in favor of creating first “portfolio effects.”

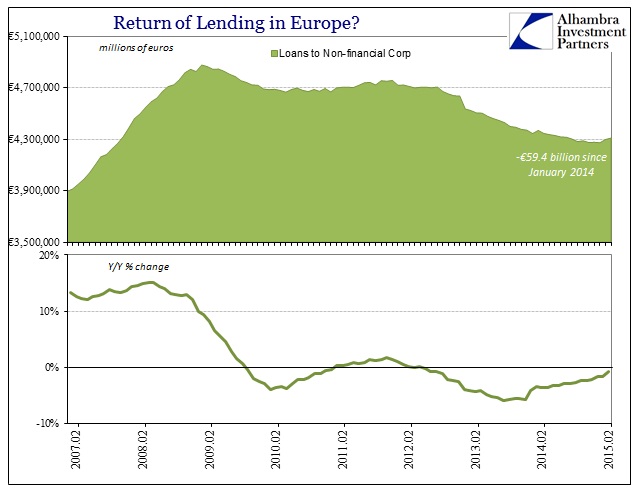

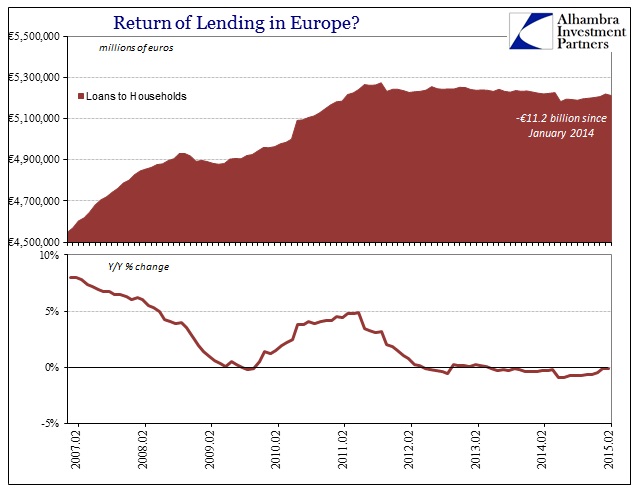

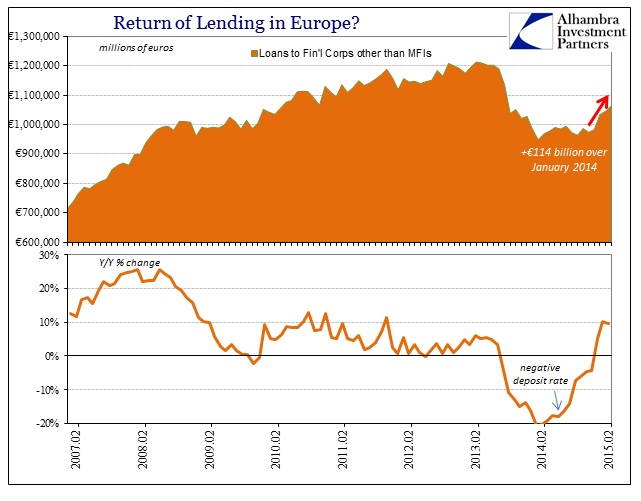

As I noted last month, it appeared that lending in Europe had sharply returned and that there was finally success in meeting expectations. However, the January figures, as with those of February recently released, show conclusively exactly the kinds of distortions shown above; namely the increase in lending is contained solely within finance yet again. Households and businesses continue to see shrinking credit resources available to them while there has been a serious and huge run-up in lending toward interbank conduits that are still unclear in capacity and structure (as well as intent). You can bet, as I would, that this jump is entirely related to the post-June ECB heavy hand.

There can be very little doubt left that central bank interference through the QE-style methodology deeply penetrates and impacts financial existence, thus rendering Bernanke’s suggestion of total impotence completely wrong. Where this monetary theory gets invalidated is in the next step(s) where the idea of “portfolio effects” are clearly and almost totally unpredictable and nonconforming to the very generic assumptions of orthodox theory. Under that theory, economists simply expect that QE (A) leads to a better economy (B) without ever considering the massive complexity that stands in between A and B.

If there is ineffectiveness in monetary policy, with more and more evidence proving this point before Bernanke’s very belated acknowledgement, it is in its total adherence to unrealistic simplicity. A good part of that relates to the heavy reliance on econometrics, which requires overwrought simplification just for the math to be computable, but also the fact that orthodox theory remains stuck attached to a monetary system that hasn’t really existed in decades. If only it were as easy as printing money, but in the 21st century you have to consider the exact form and countereffects of where it all ends up, in whole or in part. QE creates obvious and observable financial distortions including bubbles with little else, and its proponents are left not long afterward (Draghi will get here at some point) trying to claim it doesn’t do anything just to deflect any blame.

What a wonderful and perfectly representative dichotomy of where monetarism stands. We have the former, massive practitioner of QE telling the world how it does nothing much while at the exact same time the latest tells the world its super-healing and supporting properties. What’s reconcilable about those two positions is simply asset bubbles, as they are what stand against the former and remain the only, dim hope of the latter.

Stay In Touch