In looking last week at some stress mechanics of the interbank markets I intentionally left out one piece, the Overnight Index Swap. OIS is often viewed as another measure of liquidity risk, keyed off matched maturity LIBOR, to give us a sense of order and good function. There is an OIS rate for every major currency regime, predicated and cued to the relevant central bank rate. That is because OIS is the price at which a counterparty will pay for the fixed leg in a funding swap.

In an example, a money center bank could pay 1% on a 12-month deposit CD, but only wishes to take the funding dependability of that while reducing the overall funding cost. In other words, the bank wants to keep the 1-year term but swap down to the ultra-short overnight rate. The OIS allows the bank to do that as it will receive, say, up to 50 bps on the fixed leg in the swap. If the overnight rate, tied to the federal funds target rate in the US$, is expected at less than 20 bps then the bank will be accruing liabilities at 70 bps, saving 30 bps on funding.

Since the swap is only an exchange of cash flows on the difference between expected payments, with, as other derivatives, no actual notional value exchanged or at risk, the OIS hedges are almost pure expressions of interbank liquidity and its relation to the monetary policy rate.

The FOMC in 2008 favored the LIBOR-OIS spread as a measure of interbank effectiveness of its own policies, which I think was a huge mistake. I think overdependence on OIS has been the cause of a lot of monetary policy problems, which has further implications in interbank settings (even recently). In other words, I don’t believe OIS tells central banks what they think they want to know, and instead may end up being at least partially deceiving.

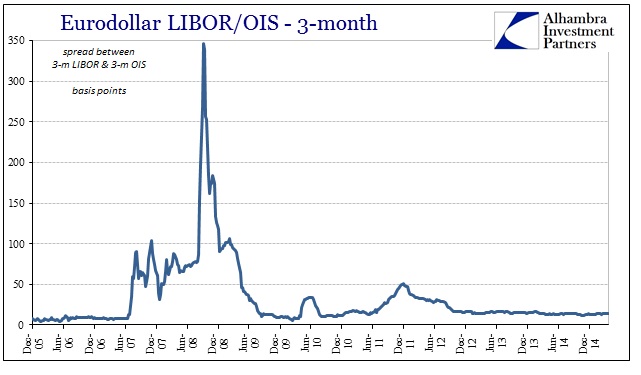

To get a sense of that, we can go back to the summer of 2007 and see the various pieces in action. Clearly, LIBOR-OIS (usually 3-month maturity) holds some value in displaying serious distress.

Zooming in toward August 9, 2007, the OIS rate began to drop while LIBOR expanded. From the OIS perspective, that meant interbank counterparties were willing to accept lower fixed payments because there was a growing expectation for central bank rate cuts (which would reduce the OIS reference). That is, at least, the predominant interpretation as OIS is assumed to be a function strictly of hedging term funding costs related to central bank policy.

Like all the other interbank rates, there is a smooth and deliberate hierarchy prior to August 9 (or 8th in the case of LIBOR), 2007 – thereafter noticeable discord and an elevation of chaos-like functionality. For this mainstream interpretation, what matters is the green line on the chart immediately above sinking after the first rumble of crisis. That meant OIS hedgers were expecting a sharp, especially around December, decrease in the federal funds target which the FOMC believed(es) amounted to an increase in liquidity provisions.

However, the dark red line, 3-month LIBOR, did not initially follow OIS, thus coming out as a widening spread. Again, that is interpreted as the inability of the interbank market to translate expected policy “easing” into term function. In fact, if you follow interbank function further into 2008 there are all sorts of anomalies persisting throughout.

On two separate occasions, both lasting several weeks, the 3-month LIBOR rate fell below the effective overnight federal funds rate. In other words, termed eurodollar funding was less costly than overnight funds in the supposedly highly-connected and FOMC-driven federal funds market in NYC. The FOMC, for its part, took that as a positive signal, as St. Louis Fed Chief Executive William Poole noted in an intermeeting conference call on January 28, 2008:

Second, this action will not be viewed in the marketplace as anything other than a direct response to the stock market. I understand the comments about the other strains in the financial markets. Although the thing that we have most commonly pointed to, and it has occasioned the most market discussion, has to do with the behavior of the LIBOR rate, LIBOR seems to have settled down. It is trading below fed funds, and the further out you go in the future, the lower is LIBOR. So it seems to me that that situation has largely returned to normal.

That is the doctrinaire approach to these kinds of things; that the LIBOR rate was below federal funds and thus all is well-behaved when in fact, as Bear Stearn’s and others’ failures only a few short weeks later would prove, this dis-array in money market rates was signaling high distress. There are various reasons for that that are beyond the scope of discussion here, but as it pertains to LIBOR and OIS there are other interpretations that do not so easily align with that dogmatic assessment.

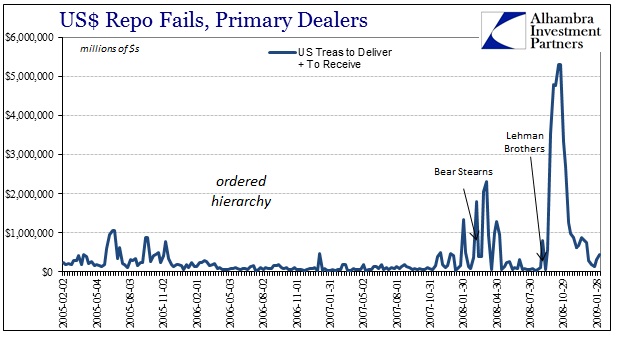

For one, OIS trades often relate(d) as much to repo markets as to federal funds. Term repo rates are notoriously illiquid, so a repo participant wanting to lock in a termed out short rate without having to pay up a huge liquidity premium in the GC repo market could use an OIS swap (or a blended curve). You finance a bond in repo rolling the overnight GC while paying the fixed leg in a termed OIS out to the desired maturity. The net funding cost becomes, then, the term OIS rate minus the average spread between GC and federal funds.

If we put that relationship into the strange occurrence where LIBOR was trading below the federal funds rate (on two occasions, including the weeks where all those March 2008 failures took place), it seems a different interpretation of events emerges. The drop in the OIS rate, rather than echo policy expectations for deeper and deeper rate cuts, may have been reflective of growing illiquidity in repo markets and an increased desire to term out funding at (almost) any cost. The desperation for OIS brought LIBOR down with it, as a means of arbitrage in spreads, more than suggesting that high stress and extreme repo difficulties were responsible for what Governor Poole thought was “normal” LIBOR.

The wholesale system does not follow “money supply” indications and interpretations, and in so many cases it is the cumulative ability of bank balance sheets to absorb risk or deliver risk transformations that counted(s) as much as “money supply” as actual dollar bills and numbers in the FOMC’s “reserve” accounts. Indeed, we know that to be the case as repo fails up and into the Bear Stearns weeks were an order of magnitude change in liquidity stress.

What we can take away from this episode is that OIS may be a good indicator of monetary transmission under “ordered hierarchy” but it isn’t nearly as straightforward under high degrees of stress. And that, I think, is the main point of emphasis in that interbank markets under true “normalization” are those that follow an orderly arrangement; any deviation is cause not just for concern but heightened curiosity about what all these rates and figures might actually mean in a realistic sense that may be apart from what we thought they used to mean. Like cornered animals, a high degree of liquidity stress forces financial participants to act in ways that are not wholly expected, so mainstream and orthodox interpretations of these numbers may not only not apply but end up highly misleading.

Stay In Touch