The FOMC statement changes seem to have initiated knee-jerk reactions undoing the interpretations of the March statement. In other words, the first blush of FOMC obfuscation appears to be trending back toward “hawkishness” in clear defiance of last month’s clear “dovishness.” The basis for that seems to be the references to what the Fed is still proclaiming “transitory” factors, to the now-preclusion of any references to actual economic figures.

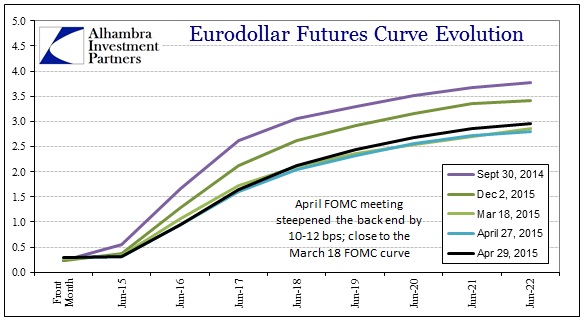

The line seems to be one of that the FOMC is not yet convinced the gathering “slump” is a slump. From that there are indications that take perceptions back to a 2015 end to ZIRP. That seems, again at least initially, how the eurodollar market has reacted, with determined selling out past the policy window. The back end of the curve steepened almost as far back as to what it was on that last March FOMC meeting.

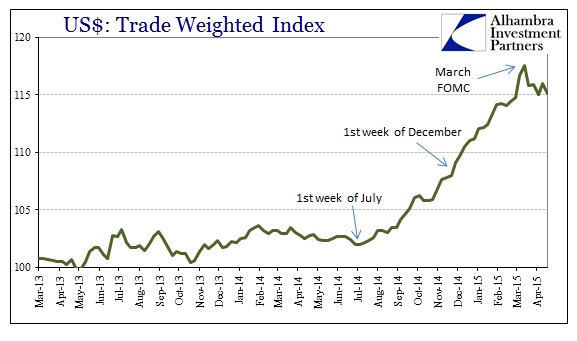

With the front end still much lower, it seems that the curve is suggesting that, in contrast to March, the Fed will be raising rates just not necessarily in the next few meetings. The danger in that shift is obvious, with the March 18 FOMC meeting clearly offering a release of “dollar” pressure. Almost every major funding indication shows a pause originating around that date. It is far too early to tell at this point, but if these “markets” are back into a pre-March 18 frame then the risks of the “dollar” may turn yet again.

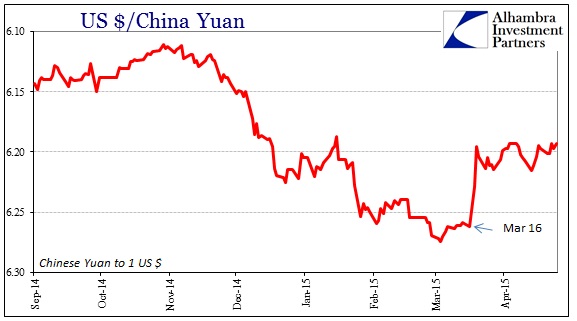

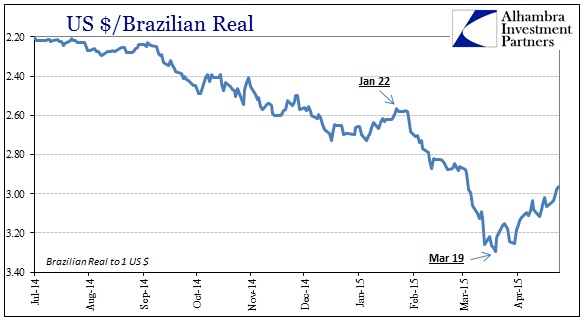

That would be a seriously unwelcome inflection, as most other “dollar” markets have been retracing under this pause. Even the Chinese yuan has become far more stable despite the rash of nasty economic indications and even more uncertainty about what the PBOC might or might not do about it. In other words, forget what is happening in China, the yuan is all about the “dollar” in the purest financial sense – and since the March FOMC that has meant a far more placid existence.

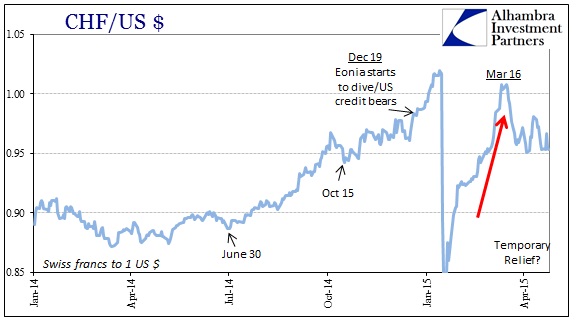

The same sentiments are echoed in other “dollar” connections to funding margins.

As I mentioned last week, this shift/non-shift by the FOMC may have been anticipated by wider credit markets. The UST curve, for instance, has been almost completely unmoved during the March/April pause in the “dollar” despite these other indications that there was some serious relenting. Perhaps credit markets anticipated this “game” of FOMC policy guessing back and forth, as it almost seems as if they were expecting the “dovishness” as nothing more than a ruse (maybe the FOMC is channeling a little inverse PBOC in this back and forth?).

While UST’s sold off a bit in the past few days, nominal rates remain largely in the same post-December range while the curve shape remains highly bearish/flat. We will see how these markets react now that the FOMC is back on track, if the “dollar” turns once more toward disruption – there is a good chance that it will not, as the June/March surge may have been enough already, certainly unleashing as-yet unfulfilled problems almost everywhere.

Stay In Touch