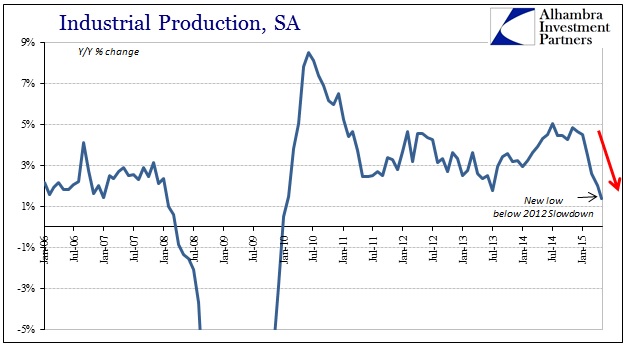

Another contraction in US Industrial Production has extended the slump to half a year. That includes, perhaps more importantly, serious and continued erosion in capacity utilization. There were some minor upward revisions in prior months though nothing to a significant degree, leaving May IP up only 1.37% year-over-year. That is the slowest pace of the entire “recovery” period, and a stunning deceleration since November 2014.

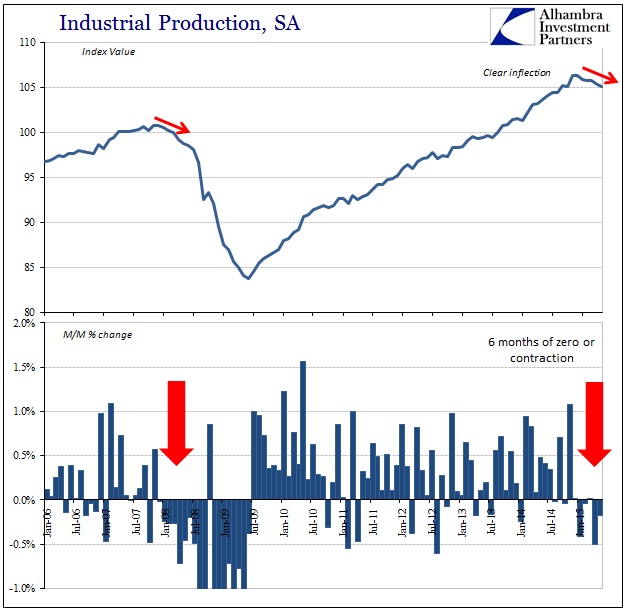

Month-over-month, IP fell slightly in May despite a sharp decline in April, meaning no rebound whatsoever despite all economists’ expectations about weather and “seasonality.” No matter the perspective, it is obvious that the economy has decelerated noticeably since around October or November. The only comparable six-month period in recent history was the six months right at the outset of the Great Recession (starting December 2007).

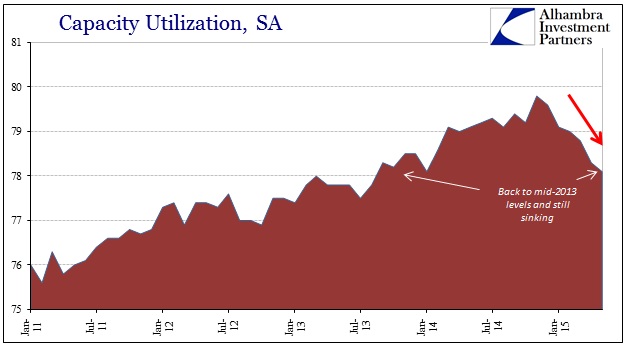

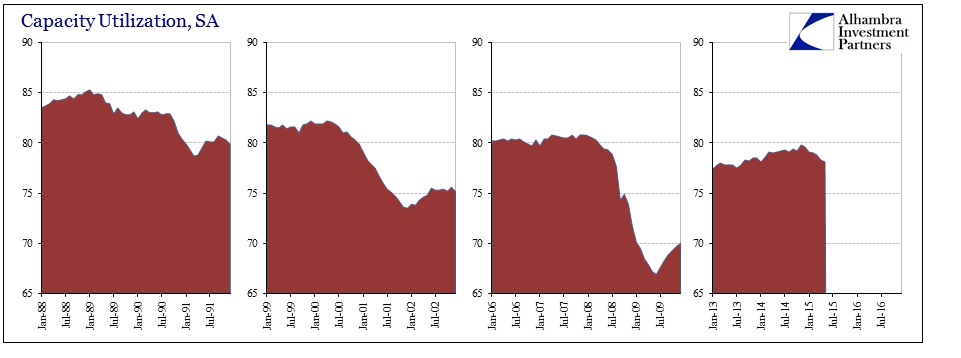

That view is echoed by the behavior in capacity utilization. While there were minor upward revisions to prior months here too, nonetheless the overall pattern remains; all that has changed is the estimated month where capacity really and truly sat idle. In addition to a sharp drop in January, there is now estimated a second decline of equal magnitude in April (with May not arresting that downward slide but going a bit further still in the “wrong” direction).

In historical context, capacity utilization is one of the most reliable recession indications even where timing isn’t as uniform. In other words, while it may not tell us exactly when a recession might be declared it is very useful as a signal for the presence of recessionary pressures. The downward drift in efficient production leads to downstream impacts in both capex and labor utilization. Unlike the orthodox economic treatment of “slack” in some ephemeral sense about labor competition, capacity utilization shows real slack which when retreating far enough will trigger the true recessionary responses – deep cuts to capex and layoffs.

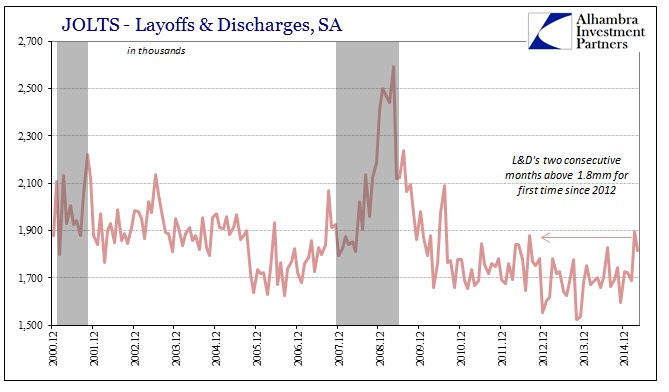

The drop in utilization rates shown here may already be having a negative effect. While the mainstream world was busy celebrating the unbelievable (perhaps literally) surge in job openings, the same JOLTS report estimated that layoffs and discharges surged to their highest (worst) since 2012 in March. That would seem to offer some complimentary interpretations about both that data point and what we see here in capacity.

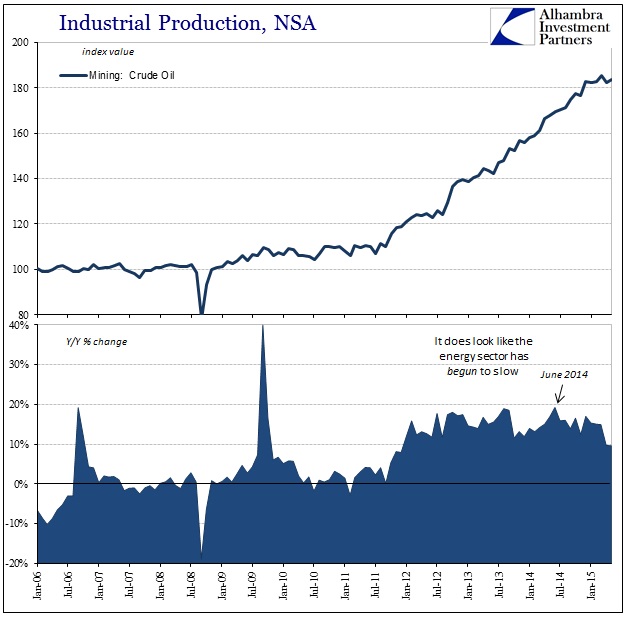

As noted in prior months, while all of these pieces of industrial production are concerning, they do not yet include a serious downturn in energy production. In other words, as bad as IP calculations are overall right now they are still being aided to a significant degree by oil and gas activity. In the energy sector, production has only just begun to slow, but is still advancing at a highly contributory pace. So where IP in oil “mining” may be growing at just less than 10% Y/Y, which is the slowest since the shale boom began in 2011, it is still growing relative to base comparisons both yearly and monthly.

That would suggest that the inventory overhang is proceeding as expected long before even the energy component is snagged by the “dollar.” If these negative trends begin to fuse then the recessionary pressure begins to grow not just in devastating summation but exponentially. In other words, the US economy already has a serious problem or “slump” that is quite corrosive, but still does not yet feature the typical combination of negative factors that create actual and outright recession – but that those negative factors appear to still be building now five months into 2015 far past now all proclaimed turning points. The extended duration is the most worrying signal, as accumulating declines in capacity utilization, for example, only heighten what amounts to reverse hysteresis; layoffs and cuts to capex aren’t linear, proceeding calmly and cautiously at first, but once a critical mass of negative factors is reached the flood gates simply open fully.

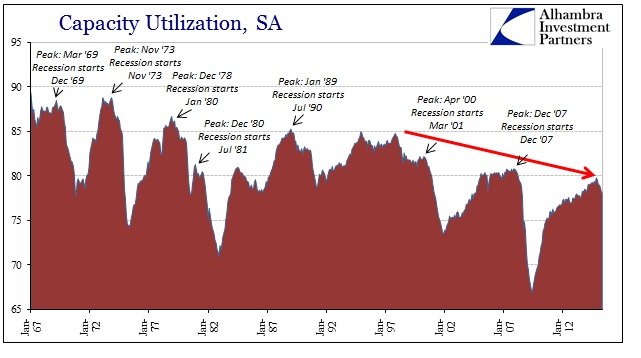

I think that is the interpretation of capacity utilization shown above. The peak in utilization again does not tell us when the recession might begin because we can’t know directly at what point that “critical mass” lies. Instead, the retreat in capacity shows that US industry is simply well on its way to that point.

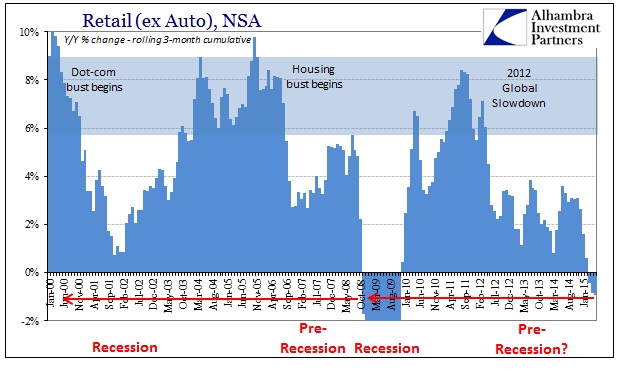

Unfortunately, the US economy in 2015 is still moving in that direction and already under extreme pressure from the top range of the supply chain: consumer spending and retail sales. From the figures here, it is all but assured that the massive inventory problem is indeed massive, having cut a great deal out of already wholesale activity and now into production and manufacturing itself (both here and abroad). That such a trend already began without a significant and open “trigger” (orthodox economics assumes that recessions require a “shock”) is cause for even greater concern (consumers that never left the bunker from the last “cycle”).

Stay In Touch