I typically stay away from sentiment indicators and measures of “confidence” not just because they are of dubious construction but they often don’t mean what they are taken for. In the case of consumer confidence, you get both problems simultaneously particularly at the ends of each cycle. In other words, just as “confidence” is at its greatest point and economists, especially the FOMC, assert that as evidence for further economic gains the rug is pulled out, “unexpectedly”, and a precipitous decline just shows up.

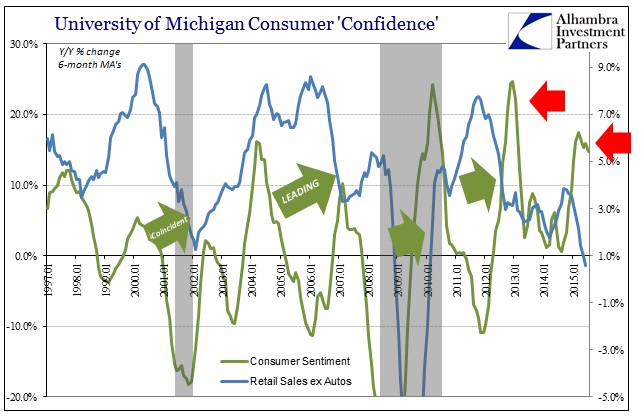

A few months ago I looked at the more recent break between confidence and spending. In past cycles, consumer confidence at least bore some coincident and even forward resemblance to economic activity, retail sales in particular. That broke down around 2011 as consumer “confidence” and spending have been unrelated ever since.

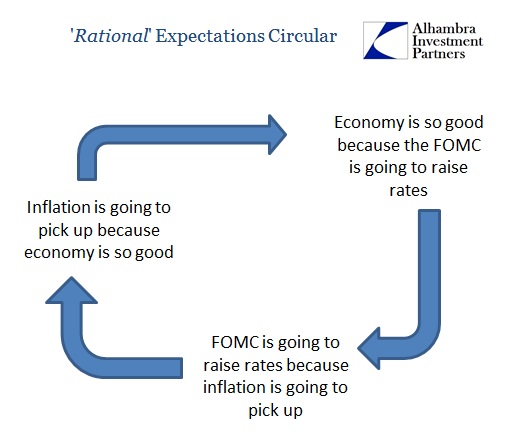

The reason the FOMC relies so heavily on confidence measures and surveys is rational expectations. The theory asserts feelings and psychology as more important than real factors, therefore it is assumed that influencing emotions is as much economically useful as even the helicopter option. The same is true of orthodox belief in the opposite, recession, as monetary policy attempts to banish “undue” pessimism as an answer to contraction.

With that in mind, the past year has offered what I think is a stunning rebuke to that theory. Starting in the spring of 2014, just after the nefarious cold winter, almost all the major indications jumped. The increases were questionable, and remain so, meaning that offers a useful control as far as attempting to measure the effects of pure numbers alone. Accounts like the unemployment rate, Establishment Survey and GDP surged without a matching increase in more “hard” data less subject to trend-cycle and non-seasonal seasonal adjustments. The response was striking in that the pure, number increases seemed to have worked upon at least consumer confidence (and, I would add, business confidence in the various business sentiment surveys).

A year ago, the surge began which is also a compelling contrast since the “dollar” and global finance started at the same time to retreat. That didn’t matter, of course, as all that seems to have penetrated was the constant drumbeat of the “economy is awesome.”

From July 2014:

Its [Conference Board] Consumer Confidence Index reached 90.9 in July, up from 86.4 in June. It was the third straight monthly increase and the best reading since October 2007. Tuesday’s report solidly beat economists’ median forecast for a reading in the mid-80s.

The report follows a five-month string of bright employment reports after a rocky start to the year that’s been mostly blamed on an economically-crippling hard winter. From February through June, the economy has added more than 1.2 million jobs and the unemployment rate has fallen to 6.1% from 6.7%.

“Strong job growth helped boost consumers’ assessment of current conditions, while brighter short-term outlooks for the economy and jobs, and to a lesser extent personal income, drove the gain in expectations,” said Lynn Franco, the board’s director of economic indicators. “Recent improvements in consumer confidence, in particular expectations, suggest the recent strengthening in growth is likely to continue into the second half of this year.”

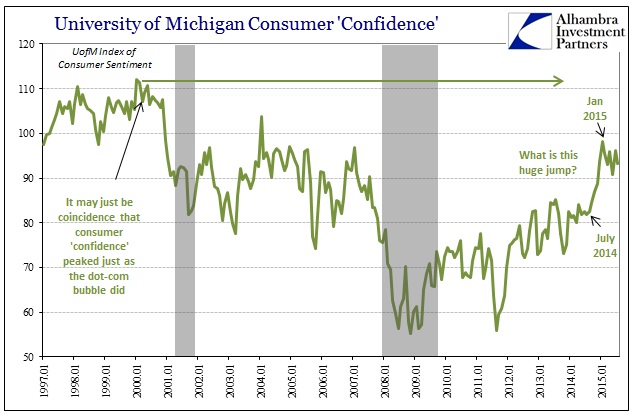

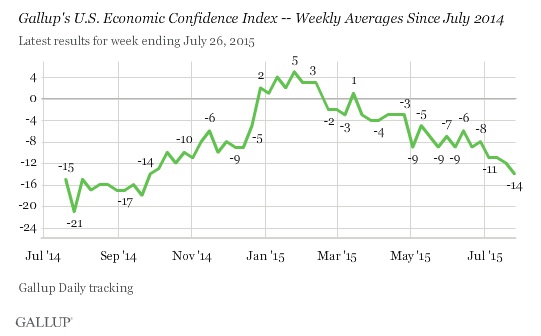

That seemed to be the case as GDP grew nearly 4% in Q2 (since revised up) and then nearly 5% in Q3; with that “convincing” Q3 release published in December 2015. It wasn’t just the Conference Board’s estimates that surged, as everything from the University of Michigan Index to various Gallup economic tracking polls picked up the same robust “happiness.”

It is difficult in these various accounts not to notice the sudden and lasting downward bend now to July 2015. There is a hard reality that has shown up this year in sharp contrast to all those supposedly interpretive numbers from later last year. As an experiment in the two parts of rational expectations, it does appear as if the first part works. It wasn’t just the quickly falling unemployment rate that was intended to be convincing of the recovery arrival, however tardy by years. Alongside that was persistent reinforcement of the narrative by policy “noise” that was undoubtedly meant to foster those perceptions; by tapering QE, then ending it and further asserting an “exit” from even ZIRP, the FOMC was inarguably trying to harden those happy acuities into a coalesced economic reality.

That part appears to be validated, again, by at least consumer confidence if not also business confidence and even some measures of business activity (especially inventory). The second part, the more important transition, however, has been shown quite lacking. For all the immense referral to confidence and emotion, the ubiquitous TV economists talking up that 5% GDP and “best jobs market in decades” at every opportunity, it appears to have mattered so very little. In fact, as noted in May, spending very much departed at the very same time as confidence was surging.

The retrenchment in consumer spending started during the fall but really turned downward during the Christmas holiday period; right when confidence was at its inspired apex. It has only gotten worse since that point, with actual, nominal retail sales nearly contracting (and actually doing so ex autos). Retail sales in 2015 are worse now than they were during the whole of the dot-com recession. Regardless of how you interpret that in the context of the business cycle, it is at least a disqualifying contrast to what rational expectations asserts of emotion – happy and optimistic consumers did not lead to actual spending renaissance but rather yielded to its opposite.

I think that rightly accounts for the round trip so far in the middle of 2015, as economic reality is more of a confirmed now slump that actually bodes much worse for the rest of the year. When consumer confidence was at its peak in January, the idea of a protracted decline or even recession seemed, in the orthodox-contained mainstream, laughable. Yet here it is, now entering the second half long past the “residual seasonality” and weather-drawn obfuscations (port strike still?).

Even the unquestioned payroll expansion has fallen to such degeneracy. The Conference Board shocked yesterday with its July 2015 decline, as the “expectations” portion of the index just collapsed from 92.8 in June to just 79.9. The reason, questionable labor markets:

“A less optimistic outlook for the labor market, and perhaps the uncertainty and volatility in financial markets prompted by the situation in Greece and China, appears to have shaken consumers’ confidence,” Lynn Franco, director of economic indicators at the Conference Board, said in a statement.

Americans’ assessments of current and future labor-market conditions deteriorated. The share of those who said jobs were plentiful dropped to 20.7 percent in July from 21.3 percent.

The proportion of consumers expecting more jobs to become available in the next six months decreased to 13.1 percent, the lowest since November 2013, from 17.1 percent in June. [emphasis added]

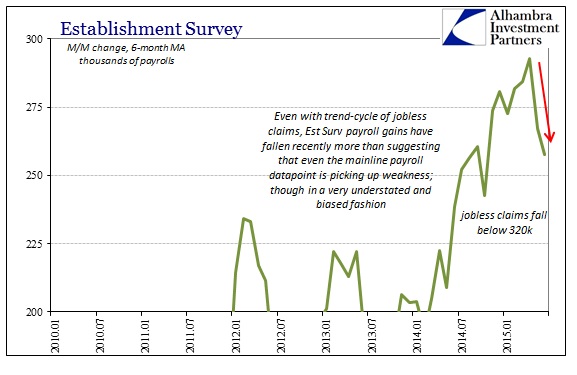

This is something that is unsurprising given 2015 in its more general sense so far. Even the vaunted Establishment Survey, still running at a high rate, has cooled somewhat. If you factor in trend-cycle, this disparity between feelings and activity becomes less surprising. In my view, especially in tandem with the break between confidence and spending, these are results of the “fake” recovery in total.

In short, policy constructs the visible façade of recovery in the expectation that businesses and consumers will then fill it out beyond, a mechanical response to only noticeable changes. In that way, the fiscal view and the monetary view are supposed to be highly complimentary, as the government redistribution creates spending transactions financed by the monetary, central bank redistribution through asset prices and debt (modern “money”).

Recovery is actually none of that, as what drives actual spending apart from forced redistribution is always opportunity; and that is not something that can be faked or reduced into mechanical, spreadsheet formality.

I think that last part is being proven by “confidence” , as everything was supposedly going right last year, the appearance at least of the recovery arrival was as strong as perhaps it was ever going to be. In the end, again, it amounted to very little, likely even less than nothing as there is attrition to consider that these primarily monetary experiments are not neutral. There is really nothing left of last year’s “inarguable” sentiments except renewed questions of veracity all the way down to even the most basic constructions. GDP may be revised up for Q1 and Q2 may actually be 2% or more, but neither is even close to what was promised and derived from 2014’s unbridled rational expectations “experiment.”

Hope, quite simply, just isn’t close to enough for a real recovery. Spending grew only worse during this “sample” period, and the fact that consumer confidence round tripped to that point shows that perfectly well. Confidence is still important to the economic system, but unlike orthodox expectations it is only a part and maybe even a small part. More than sentiment, there has to be actual jobs and wages, which I think the cycling trajectory of confidence is but another marker that those supposed job gains last year were, in fact, figments of statistical imagination. In short, the presentation of estimated job gains created broad hope in Americans not that jobs had already arrived but rather in how they thought that might signal jobs that would come. I think that is why the labor force never expanded as it should have, signaling more strongly that this was all just imaginary.

There is an undeniable element of troubling prevarication in the whole attempt to coax unearned optimism, as taken to the extreme it means that policymakers will never quite be honest about especially realistic downsides. That may even mean, in their zeal to “fool” consumers, they fool themselves on the circular logic.

Stay In Touch