In March 2013, orthodox economists were brimming with optimism. There were some rough patches in 2012, to be sure, but the Fed stepped up with a QE3 in MBS and then a QE4 in UST. Since the power of monetarism is a central pillar of the orthodox outlook, the future could only be even brighter than it was. The lackluster recovery to that point was thought, even after an “unusually” cold and snow winter (the first of three, and counting), to be finally and completely accelerating. That was good news not just for the US but the entire global economy:

The improved job market can also benefit countries that sell goods and services to U.S. consumers and businesses.

“All you have to do is look at the trade numbers,” says Bernard Baumohl, chief global economist at the Economic Outlook Group. “The strength in the U.S. economy is leading to faster growth in imports.”

Imports rose 2 percent in January from December. Those from China surged 7 percent.

A stronger U.S. economy, Baumohl says, will also help a battered Europe, which is contending with high unemployment and a debt crisis. The United States is the No. 1 market for exports from the 27-country European Union.

“The extent to which the U.S. is recovering and potentially the labor market is improving is potentially an important dynamic that Europe would welcome,” said Nick Matthews, an economist at Nomura in London.

Hollywood might not have been able to propose a better, more uplifting script. The happy ending was at last in view and economists were the heroes. Stocks surged as did the corporate bond bubble, leaving behind what they were already calling at that point the bursting pessimism bubble. As if right on cue, gold was just about to crash which only furthered the certainty to which all this was given.

Just two years later, most, if not all, of that is gone. Gold (and later credit) was not occasion for giddy but a stark warning that “something” wasn’t right with the screenplay. Europe, Japan, China, Brazil, etc., have not seen any translation from the purported labor surge as none of it transitioned into wage growth and then spending growth. In fact, the only part left of the March 2013 celebration is the raw job count and even that is slowing.

There are a great many wrongful assumptions that have to be made to be on the wrong end of all this. In terms of making such predictions, there were grave warnings even then that should have accosted the economic carnival. The alarming slowdown in 2012 was the first, as why did the Fed “need” two more QE’s in the first place? It has taken a few years, but even GDP now shows the reasons for it – it was a severe downshift in economic fortunes right at the moment economists were claiming the opposite direction.

Even though contemporarily GDP was much more charitably disposed, there were many other serious incongruities. Despite an assumed payroll surge, the pooling labor force did not rush to join. There is a surprising apathy in true labor mechanics against that assumed backdrop, as the great hole left by the Great Recession did not permanently alter the willingness of labor to participate but seemingly instead their ability; demand not supply. In other words, while the BLS may have measured more job growth the lack of forward momentum in joining the labor force argued quite more forcefully against it.

That naturally has created a world of problems not just in the real world but in all the downstream and bridging statistics. I have discussed at length the idea of productivity in exactly this light, how productivity is a spotlight on the fact that recovery expectations are and have been so very far out of place.

It hasn’t gone unnoticed by the orthodoxy; quite the contrary. But their notice amounts to further evidence of all that is and has been wrong. That starts with the fact that economists take these productivity figures at face value, and then develop interpretations from there. It’s an odd and backward approach, but it makes sense since nobody in the mainstream will ever challenge the mainstream statistics even when it leads to opinions that stray further and further from lucidity.

The dropoff in productivity — a trend that’s occurred worldwide — is a more daunting challenge. No one really knows why it has slowed.

Since productivity as a concept (rather than purely a statistic) is vitally important to any and all economies it wouldn’t just be unusual, such an outcome should develop great skepticism from the ground up. Instead, again, it is just accepted.

Throughout its history, the U.S. has been a productivity powerhouse. The amount of goods and services produced by American workers increased by a healthy average of 2.7% a year since 1948. It even grew by a whopping 3.3% annually from 1998 to 2005.

Yet productivity began to slow about a decade ago and it’s grown by a meager 0.6% annualized average in the past 21 quarters.

“That’s a scary number,” said Gad Levanon, managing director of economic and labor market research at the Conference Board. “Productivity has never grown that slowly.”

Economists offer a variety of explanations.

So there is something highly unusual, in fact “never grown that slowly”, that dates to around 2006? In fact, the “explanations” that have been proposed are, in the main, just silly; that easy innovation, the lowest hanging fruit of industrialization, has already been plucked; demographics and the Baby Boomers; globalization; not enough “optimal outcomes” meaning more centralization. And so on.

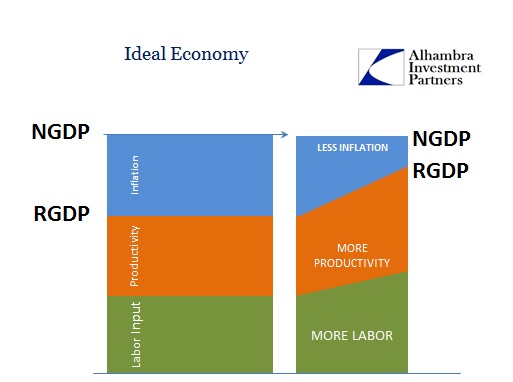

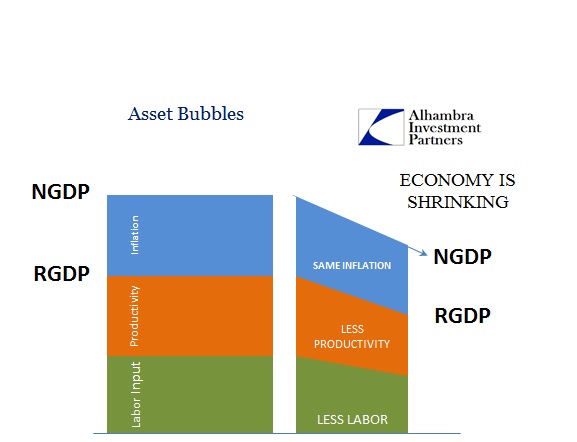

The trajectory of productivity, as a statistic, offers quite a compelling story that more than suggests a misguided focus. Starting from the realization that productivity as an economic measure is only a plug-line calculation between the BEA’s “output” and the BLS’s labor stats, it is really the balancing variable in a three variable system – the third being “inflation.”

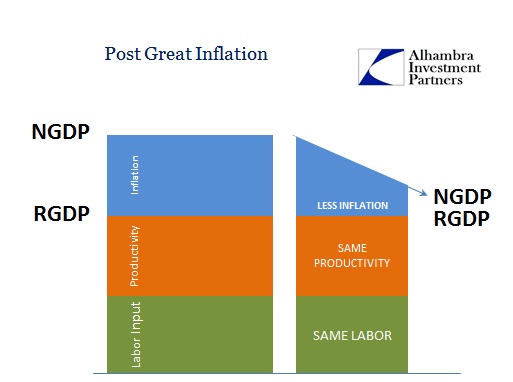

In a truly healthy economy, there would be less “inflation” (consumer prices) for a given nominal GDP regime. That would mean, and the statistics would calculate, more “room” for both productivity and labor utilization – the best of all worlds for both business and labor. That hasn’t occurred in our history since before the Great Inflation (first clue). Instead, even during the PR-coded Great “Moderation”, NGDP has been falling. With that topline decline, that means at least one of the three components had to likewise shrink. Economists convinced the world they had found the secret recipe with which to only shrink “inflation” while leaving the others to offer better than “moderate” prosperity.

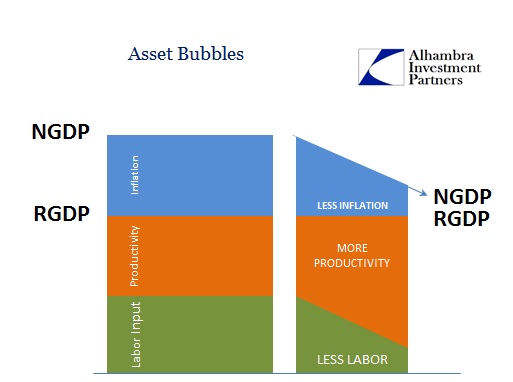

That may have actually been the case, at least during the first burst of expansion out of the double dip episode of the early 1980’s. Somewhere, though, that consistency was lost. We know this without question because of the “sudden” appearance of huge asset bubbles in the 1990’s (as well as an entire monetary evolution and regime alteration, the eurodollar standard’s speculative phase, but that is a separate, if still related, topic). Asset bubbles are a tricky prospect particularly in an age qualified as “moderation.”

In our general terms here, the asset bubbles simply propose strong evidence of orthodox economics being wrong about their models and these assumptions – being able to manipulate only inflation while leaving labor utilization and productivity as “market” determined-advances. That discrepancy has become wide open in the 21st century, with productivity at its center.

First, as noted two days ago, labor gains (wages as one very prominent expression) parted historical experience at the dot-coms. Since the orthodox figures assumed less “inflation” too, the gap was bridged by what appeared to be much higher productivity (this is taken as “globalization” efficiency). Given the labor element, it might instead propose that GDP itself was overstated, if also in combination with the undercount of “inflation.” The asset bubbles themselves propose no less, as asset inflation in raw economic terms is highly, highly inefficient. When accomplished through vast expansion of debt, the rise of productivity is at best an illusion of that debt (which is, again, one form of inflation). Borrowing funds from home equity (the inflation) to pay for goods imported from China is not high productivity except for China (if artificial).

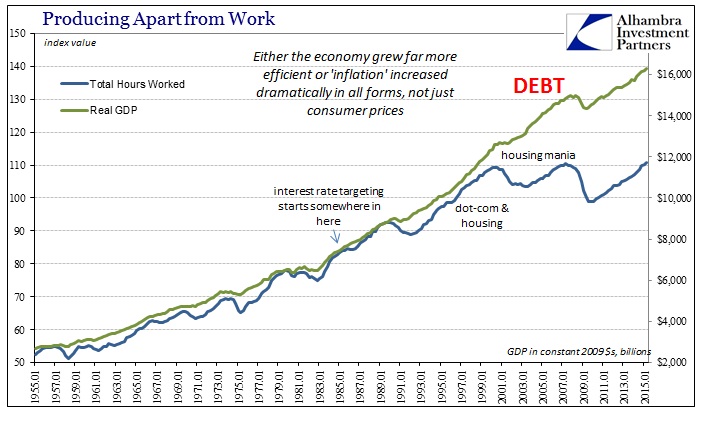

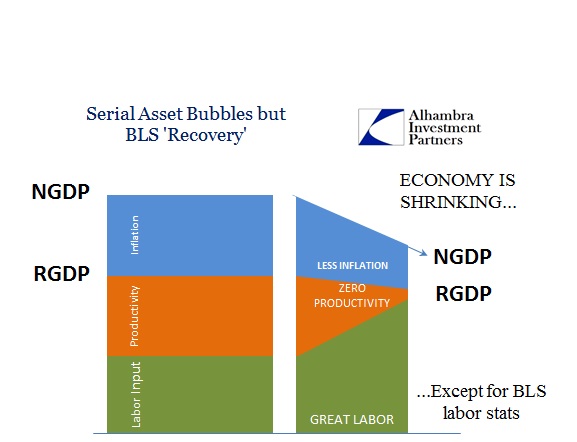

In actual function, away from what are presented in the statistical calculations, the economy was likely more closely resembling this:

Thus the assumed economic gain is all or nearly all illusion of that “money” circulation as altered by redistribution. The “other” side of the Great Recession bears that out, and highlights this modification quite well – in addition to calling out these various statistical oddities.

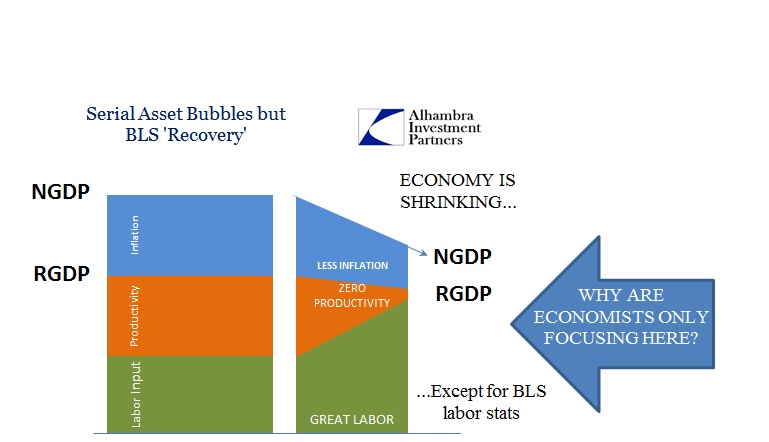

Now we have NGDP shrinking yet again, and by a large amount (even more than what is shown in the NGDP chart above; the average for the latest period does not inlcude any measured recession as the other averages do), less than even that which prevailed during the pre-crisis era, but the BLS is adamant that the labor gains are large and continuous. The only way to reconcile these conflicting views (along with still-lower inflation) is to shrink productivity to zero or negative. So the focus on the labor component as distinct from the productivity component is, in the end, quite misleading. Taking no productivity is to simply accept these numbers for what they appear, with no regard for how they have been consistently revised, and attempt to reconcile from that assumption.

Under a more general view, one that is more aligning and thus appropriate, these “problems” are simply means by which the real problem is being expressed.

The problem of productivity is that the economy is shrinking and these statistics are not constructed to incorporate it. It was never assumed this was possible, and so it is simply not factored into either the numbers or the interpretations of the numbers no matter how odd and perplexing they (both the numbers and the interpretations) become.

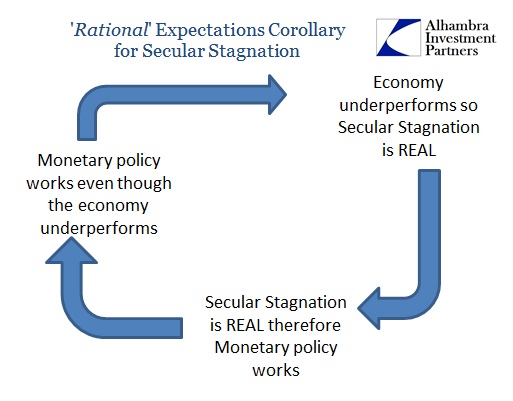

For economists, again with productivity, they see the results but not the causation. In other words, they see that the economy is “off” but do not propose as to why that may be except captured within the picture painted by these statistical malformities. Secular stagnation is exactly that, an effort to recognize the problem without actually seeing it; to say that productivity has slowed without admitting the entire economic system has been altered by interference.

Economics thus does not allow itself to consider beyond its own self-imposed subset. The productivity “mystery” has become, in secular stagnation, a defective economic system all its own, completely and totally sapped of vitality for now and for the long-term. Because they can’t see beyond the flawed figures, which are even telling them to look beyond, the depression becomes all that there is and could be:

Private economists and the Federal Reserve predict sub-3% growth over the next three years. Looking beyond, the nonpartisan Congressional Budget Office predicts the economy will expand by an average of just 2.1% through 2025.

“I am not going to say we can’t get to 3%,” said John Silvia, chief economist at Wells Fargo and a former senior economic advisor in the U.S. Senate. “But 2% to 2.5% is probably the best bet, at least for the next few years.”

The more economists have attempted to manage the economy the less economy that has resulted. The equation of correlation there seems to be quite straightforward and does not need an alignment of productivity or inflation, though they would in this view be far more intuitively coalesced and consistent. In other words, orthodox economics is a useless tautology that is revealed even under their very philosophy; managed and planned economics creates less economy therefore there is less economy. Seeing the first part as the real problem opens up the world to tremendous possibility and optimism that is not constrained by what is limited to whatever inflation central planning can bend and redistribute.

If you believe you are the ultimate, global hero, it is almost impossible to entertain the idea that you are instead the villain. Economists see themselves as the “good guys” doing the world a great favor, but even their numbers are telling them to look in the mirror.

Stay In Touch