Typically when any statistic gets way out ahead of itself it will eventually revert toward its prior state. That is the nature of stochastic modeling in economic accounts and it presents a great weakness. It is not unshared, however, as that is nothing more than recency bias applied to a quite dynamic world. The great flaw in any stochastic model is that very starting assumption – that the future will look reasonably like the recent past.

From that structural standpoint, you can begin to appreciate the problem at various agencies in dealing with the aftermath of the Great Recession. Since this “recovery” looks nothing like any others, assuming statistical trajectories that conform to prior versions is not just a potential mistake it may be highly misleading. That point has already been stated repeatedly and is still being revealed with further benchmark revisions.

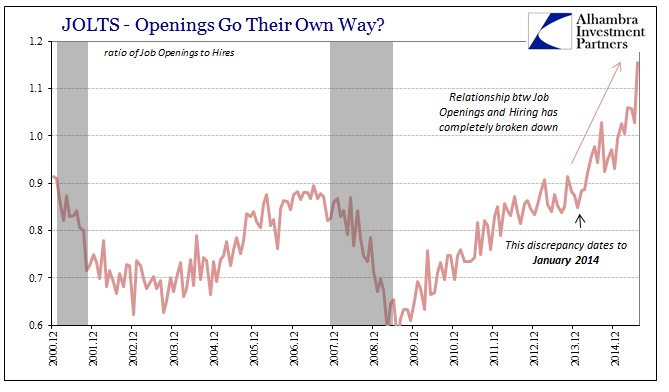

That brings us to the case of the BLS’s JOLTs survey and the utter chaos in the Job Openings component. Dating back to January 2014, we are supposed to accept that businesses suddenly and sharply deviated from their prior “recovery” doldrums to gain employees at an outlier pace. While that has been more or less the case for the past year and a half, the BLS just published an estimate for July that does not revert toward something more sensible but rather pushed unbelievably toward a world all its own; job openings apparently surged by 430k in July alone to more than 5.7 million!

Every orthodox economist will take issue with any negative assertion here, as the job openings series is supposedly confirmation of the main employment picture. But already there is a problem with that interpretation, as job openings are to some degree circular confirmation of the Establishment Survey since it is the CES that “contributes” a benchmark variation upon JOLTS in the first place. From the BLS Handbook:

The total employment value is obtained from the CES survey for the basic estimating cell for the month for which estimates are being made. The CES employment estimate is estimated using a much larger sample than JOLTS and is therefore considered statistically more reliable. The CES employment estimate serves as a benchmark for JOLTS employment; benchmarking JOLTS employment to CES employment increases the statistical reliability of all JOLTS estimates.

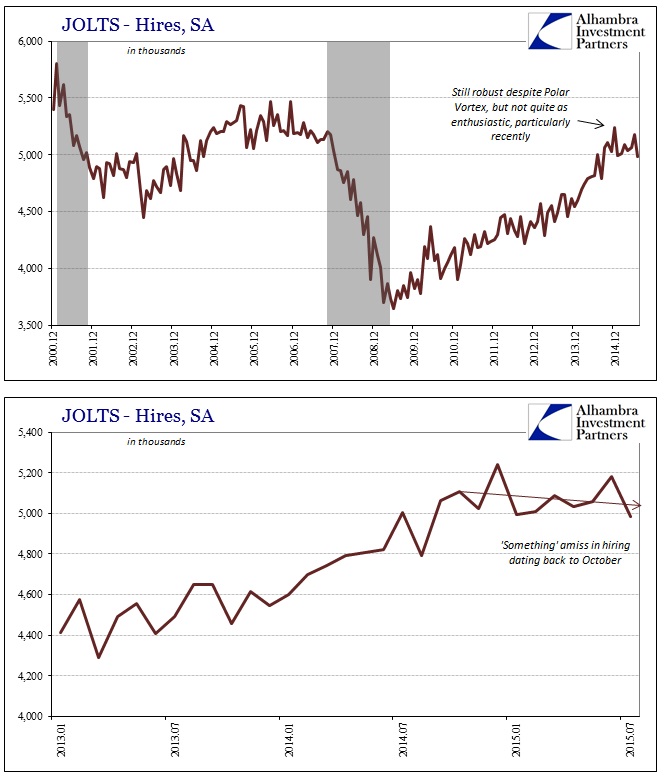

Straight away, JOLTS cannot confirm the Establishment Survey or main employment data but merely supplement it in a different but clearly related fashion. That benchmark “contribution” applies not just to job openings but also the Hires subcomponent. It is here that the statistical problems really stand out.

You can see the trend-cycle emphasis on hires dating again to January 2014; however, by October 2014 the hiring trend apparently started a sideways to slightly lower trend that still persists more than half into the current year. That would be more consistent with even the overall direction of the Establishment Survey which, while still quite positive because of trend-cycle subjectivity, has certainly and sharply decelerated of late. The implication then of the Establishment Survey thus applies to Hires – that the deceleration is likely worse than is shown.

So what, then, are job openings showing us in a statistical sense if not real? The fact that job openings and hires really diverge right at January 2014 is a telling clue, which more than suggests something else within at least the adjustment benchmarks for Job Openings separate from Hires (while both experience the same CES trend-cycle).

Stepping back first, assuming that all these numbers are statistically valid the interpretation of those two differing labor views is a structural shift. In other words, if job openings are truly surging but hires are slightly falling then we can only conclude that there is a labor force disparity within a robust economy; businesses are trying to hire employees but cannot find enough or enough that are qualified (or enough that are qualified at the pay rate they are willing to pay out). In many ways, that would seem to describe the current view on long-term unemployment arising out of the Great Recession’s massive hole.

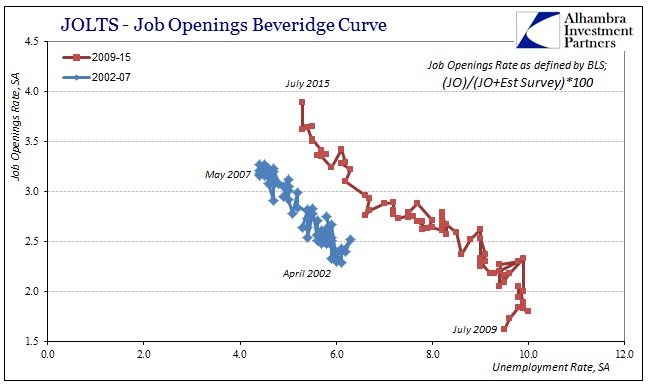

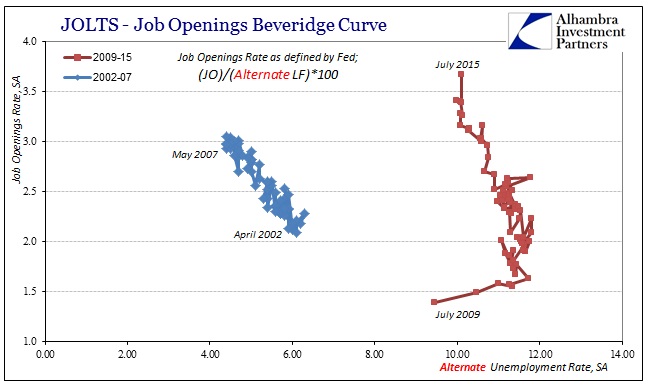

In the 1940’s, William Henry Beveridge devised a method to try to estimate any such structural economic changes by comparing the unemployment rate to some measure of generic job openings (Help Wanted ads in those days). The Beveridge Curve asserts that very relationship, meaning that there should be an inverse relationship between unemployment and Help Wanted. Plotted, this association and correlation should follow a downward sloping line where the X-axis is the unemployment rate and the Y-axis some version of business demand for labor.

The entire point of JOLTS to begin with was in that effort; to harmonize this view of labor demand into the more rigid and standardized BLS framework. As you can see plainly above, the outline of the Beveridge Curve seems to hold with some notable deviations in the current “recovery” cycle. Most prominent is that the prior cycle was much more compact and uniform, itself a clue to the difficulties arising in this period mentioned at the outset here.

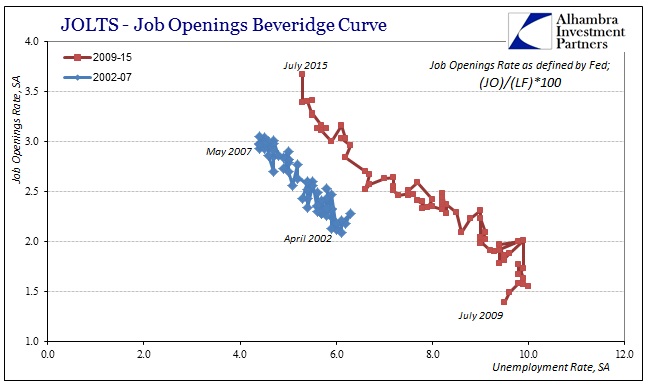

The BLS defines its Job Openings Rate that forms the Y-axis as the quotient described in the chart above, which uses essentially a comparison to the Establishment Survey. As noted, that may be compromised as a basis because of how the two data points are related, sharing some of the same “root” benchmark. The Federal Reserve’s economists define their Job Openings Rate slightly differently, comparing Job Openings instead to the Labor Force. That change in denominator offers only minor deviations (which, again, suggests the commonality in statistical benchmark root).

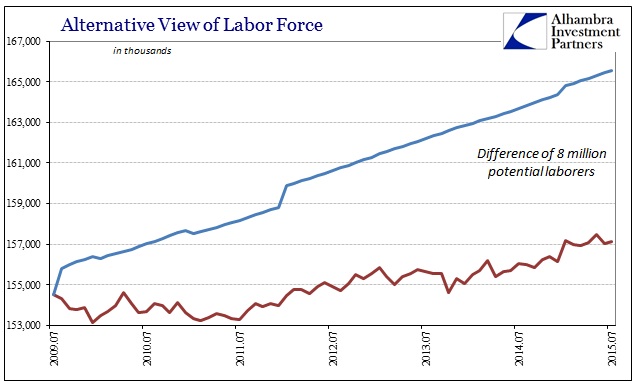

Using the Labor Force as a basis of comparison is obvious in its deficiency given the participation “problem” evident almost everywhere outside of these numbers. To offer a potential correction to that recency bias, we can supplement the labor force by “forcing” a constant participation rate thereafter the bottom (for the Job Openings Rate) in July 2009. As is well known, this adjustment is greeted in hostile fashion by economists but accepted quite widely on “Main Street.”

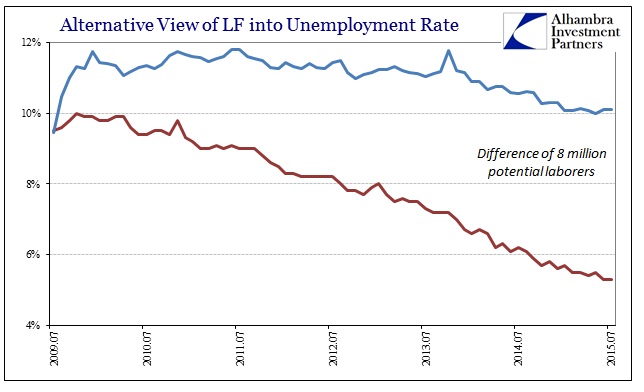

Using a participation rate of 66%, that which prevailed in the last cycle (which was still below the 67%-67.3% participation rate from prior to the dot-com bust), shows 8 million potential laborers no longer counting in the statistics. That alone should give pause about the blanket foundational assumptions embedded at the core of all these figures. But if you adjust the labor force by this view that will force an adjustment upon the unemployment rate too since it forms the denominator there.

Far from being close to “full employment” (as if there could be such a concept, or that it might be relatively static), this alternate view suggests quite little improvement in labor demand. Whereas the official version shows a recovery from 10% to just 5.1% in August 2015 (as the LF declined once more), this alternate (which still includes the trend-cycle subjectivity in the numerator) contributes a much different economic interpretation; going from about 11.5% in January 2014 when all these statistical outliers began to just 10% and flattening rather than surging or even improving more recently.

My point here is not to argue what the “true” unemployment rate might be but rather to use these alternate suggestions as a point of comparison in the structural argument of the Beveridge Curve. Plotting both the alternate Job Openings Rate (with the alternate LF in the denominator) against the alternate Unemployment Rate is quite different than the official versions.

In fact, the Beveridge Curve as it “should” exist entirely disappears, meaning that there is little or no relationship between Job Openings as they are in the BLS’s formulation and the unemployment rate that actually accounts for all potential labor. That distinction, I believe, is the central point here, namely that there are only two consistent interpretations. First, that the BLS has been entirely proper and that there is a surge in labor demand but that structural deficiencies are preventing full realization and thus that is the reason for what Janet Yellen sees and interprets as the mysterious “headwind” of slack upon wages (that are universally agreed to be still lagging and troubling).

The second interpretation is that the statistical relationships themselves have broken down sufficiently that the BLS is simply trying as best it can to conform to what is still believed to be “how it should look.” The primary clue for this interpretation is how all these measures truly depart right at January 2014, where new subjective benchmarks have been set under trend-cycle estimations not yet encumbered by benchmark revisions that will probably in time look like those that removed so much “growth” from 2012 and 2013. The fact that all these numbers (Job Openings, Est. Survey, GDP) might be doing the same at the same time derives from their statistical root, including how they are to some degree (which isn’t at all clear as it isn’t disclosed) derived from the same set of assumptions.

Given all that, it is the Hires subcomponent of JOLTS that is likely the most important piece. Since Job Openings may truly be in its own statistical world free of attachment to the actual economy, the fact that Hires under the same conditions are slightly sinking may be quite revealing of what might be happening in 2015 in an understated fashion. I think the difference between Hires and Job Openings comes down to the amount of CES benchmark applied to either, and I have begun to seriously suspect that the trend-cycle estimations in Job Openings seem to be following just a little too closely to the Beveridge Curve. In other words, failing all else in actual data and statistics, the BLS is using its view of the Beveridge Curve as valid in order to define at least the contours of where Job Openings “should” be.

Thus if the economy really is declining even somewhat in 2015, with a shrinking labor force defining a significant part of the unemployment rate, then with the Beveridge Curve as a kind of template Job Openings would have to surge to maintain that forced consistency. And so we arrive once more with upside down statistics, where especially the most heavily adjusted are “forced” to accelerate because of how they are produced quite opposite what almost everything else is saying about the economy. The latter part includes, ominously, even the Hires number from the same statistical “family.”

Stay In Touch