With the ECB openly admitting worries about its own QE trying to justify more of it and then China on Friday adding its own mix, the third consecutive “double shot” just since June 27, you can be forgiven for considering the idea that all this talk about a global economic downside is finally starting to be taken seriously. A little less than a year ago, everything was “transitory” and unimportant, but then smaller and peripheral central banks began to act contrary to that assessment. Beyond that, there were liquidity breakouts infecting in more systemic fashion, including the franc “event” that foretold of greater “dollar” issues further on.

You could appreciate all that in real time, the intensification from smaller to large, but in hindsight it is unmistakable. All that is left is for the Fed to throw in the towel on the recovery, even more so than it already has, and just declare either QE5 or coalesce further the whispers of negative nominal rates. Whatever the response, the trajectory and scope is clearly widening and deepening; central banks are still acting what they think appropriate for a large-scale defensive nature.

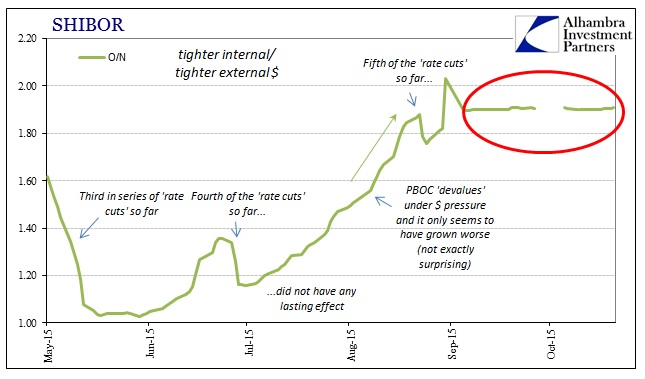

In China, for now, it is the “double shot” that is perhaps more relevant and concerning. That is simply the PBOC acting upon both the interest rate mechanisms (deposit and lending rates) as well as the bank reserve requirement. Last week, the Chinese central bank cut the lending and deposit rates by 25 bps but also opened the required reserve by a further 50 bps, for a total “easing” of 300 bps since February 4. Unlike the US, China still has a significant depository system that actually contributes meaningfully within the wholesale mess. Easing required reserves is supposed to have a meaningful impact upon money markets as banks are freed to utilize more of that excess.

Yet, there has been no trace of it anywhere so far. Further, September and October were supposed to be far more placid in terms of internal liquidity in yuan trading (both onshore and offshore). It was confirmed last week that such calm was in many ways misleading, so it makes further sense to question what exactly the PBOC is attempting in especially the reserve requirement this late in October. That assumption is only magnified by the internal/external reality of yuan connection, via the PBOC, to the “dollar.”

In other words, if the PBOC is again acting on the reserve requirement it is not unreasonable to assume that there continues yuan liquidity problems and therefore undeterred “dollar” issues. That much was surmised from the use of forwards going back to August, though we can only estimate what that might have been in September (perhaps even greater). Add all that central bank activity to whatever is taking place in yuan interbank (O/N SHIBOR) which has been obviously fixed by the PBOC, and the net result is the opposite of actual calm; it is hidden rather than open turmoil.

I believe that last possibility is the primary financial consideration about China; the central bank is increasingly desperate in its attempts to bury financial disorder, to reduce the visibility of great funding strain. From the condition of eurodollars, we can assume one and the same in terms of any source, but the increasing despondency points to what I was suggesting last week about the nature of deploying wholesale mechanisms as “solutions.”

They really don’t know what they are doing and China’s forwards put yet another exclamation on that point. That is why I have claimed these past few months that the central bank’s worst nightmare will be when wholesale exposure is revealed and appreciated as exactly the problem rather than the solution. Making Chinese banks “more short” the “dollar” is like giving a morphine addict keys to the medical locker and expecting the printed warning labels as enough to deter overdose.

In the PBOC’s Q&A statement accompanying last week’s “easing” the institution admitted as much in just that kind of provision (Google translated):

From the drop quasi point of view, mainly deal with foreign exchange generated by reducing the liquidity gap, to meet the needs of economic growth, normal mobility. A few years ago a lot of foreign exchange inflows, increase the number of foreign exchange, resulting in excess liquidity supply, so at that time to be hedged by raising the deposit reserve ratio. At present foreign exchange situation changes, a few months before foreign exchange decline a certain extent. Factors Despite the recent foreign exchange market expectations stabilized, the impact of foreign exchange liquidity substantially neutral, but the future impact of changes in foreign exchange is still some uncertainty.

They confess to a change in forex liquidity status (“dollar”) but then couch it in terms of stabilizing (which is what all central banks do for “communication”) before suggesting again that there isn’t a whole lot to depend on now (so much for stabilization) to be reasonably assured “it” isn’t actually over with. Taken together with the deposit the PBOC required, starting October 15, from only “dollar” forex and only client “buying” of “dollars” and you get the rather straight impression that the central bank is quite concerned, still, about “dollar” funding impacting yuan liquidity.

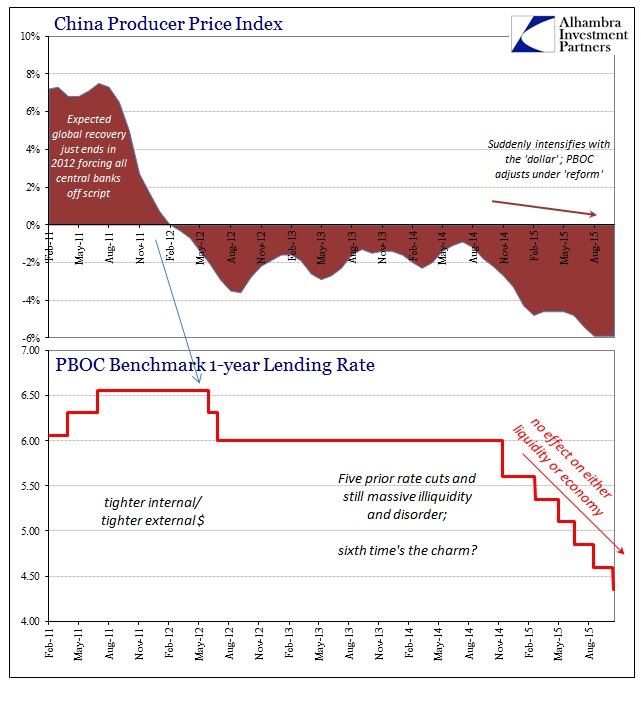

They have, of course, very good reason for that especially given how both economy and financial function has been determined in the past year. At least on the interest rate side, the raw economic slope is very easily established as “inflation” in China is as it is in the rest of the world. The benchmark lending rate lever is undoubtedly triggered by the trend especially in China’s PPI which links financial considerations such as oversupply with externalities like US “demand.” Thus, the combination is one of debt burden, supply burden and, apologies to Janet Yellen, global and US “demand” burden.

And here you grasp the utter futility that must be setting against each policy inside each of these central banks. Despite all that has been done, there doesn’t seem to have beeb any effect whatsoever in either wholesale function or economic trajectory. What good is a sixth rate cut that the prior five were not? At that point you can appreciate why the PBOC would take such pains to try, as best it might, to hide financial disorder; there is no alternative. By any reasonable conjecture, and this applies to all the other monetarist central banks, there is a looming sense of inevitability that is quite beyond orthodox capacity (and even extra-orthodox in the case of the PBOC).

They will not, however, allow themselves to do nothing even though that might be the only true path to recovery at this point. Central banks have been doing nothing but wasting time and building bubbles for which they might have (emphasis on “might”) delayed the unavoidable. The greater the anguish and distraction with which they act and contradict themselves the more irrefutable that realization by raw act of demonstration. As with the Fed and American QE, central banks have been put on the spot (especially 2012 forward) to start delivering upon their mythical status and all the power that has been assumed in them. Central banks have acted, continuously, but the more they do so the more they reveal themselves at least woefully inadequate (not quite the power and influence everyone assumed) if not purely harmful.

There is only one currency “war” and it is the “dollar” maybe now beyond all control and influence.

Stay In Touch