Economic Reports Scorecard – 11/6/15 to 11/20/15

The economic data continues to come in largely less than expected with the manufacturing/industrial parts of the economy faring worst. In what may be a developing trend, housing starts were less than expected and with last home sales reports makes for a short string of weaker reports. Generally, real estate has been trending slowly higher for the last few years and this is probably just a blip but it is certainly worthy of our attention. The labor market continues to be steady if unspectacular but weekly jobless claims may have finally bottomed out. They aren’t yet in any kind of uptrend though so nothing to worry about just yet. My biggest concern continues to be the inventory situation which got a little worse in the latest reports. That might explain the slowdown in port activity that has been recently reported and will likely weigh on production further at some point.

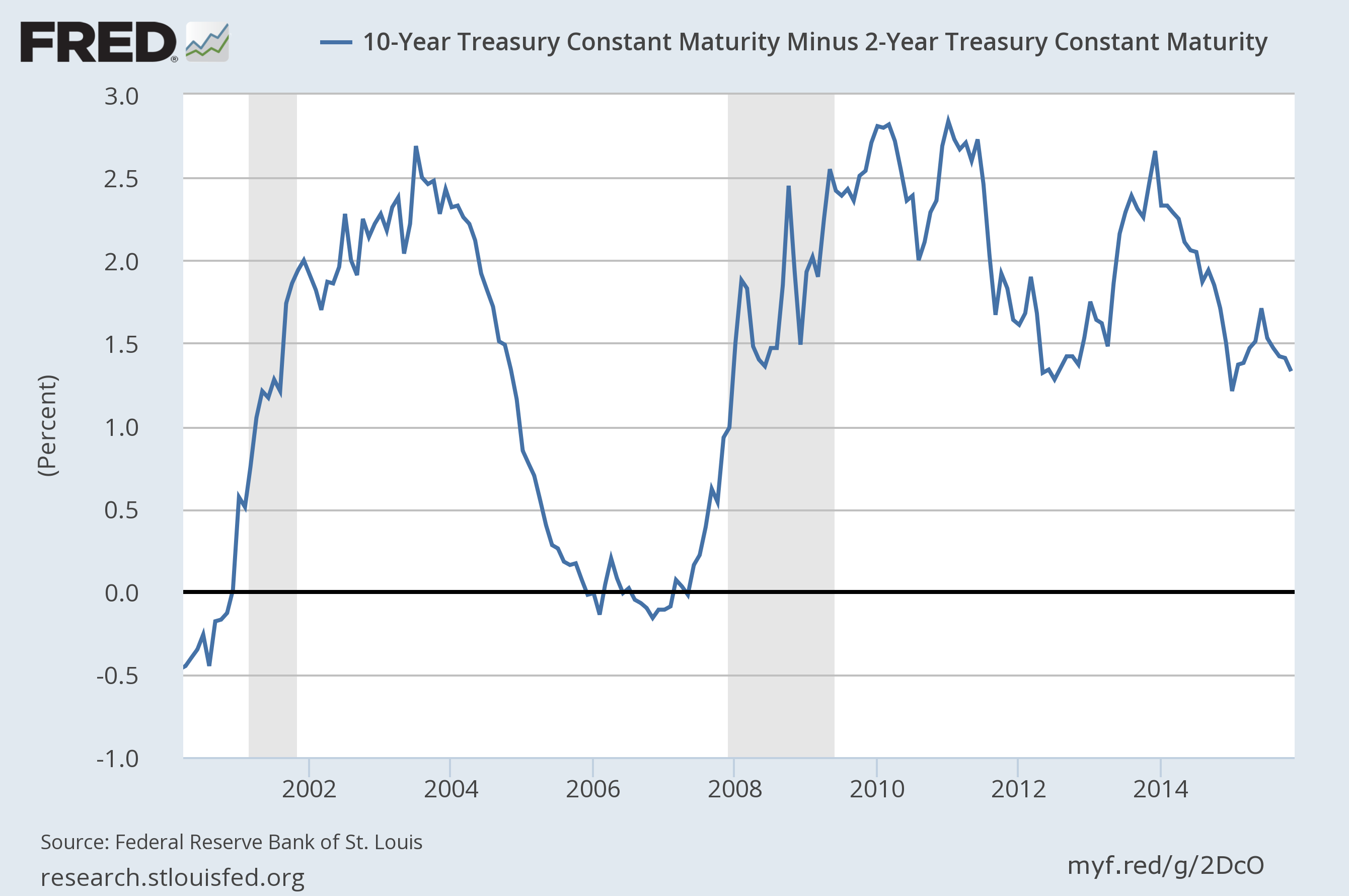

Market based indicators were about as mixed as the economic data which makes sense. Long term treasury yields fell in the context of a generally flattening curve. The curve is still in the middle of its historic range and as I’ve said many times, we don’t know if the curve will get to flat before the next recession. Actually the sign that the market is seeing and anticipating more economic weakness would be a steepening curve where short rates collapse faster than long rates. That has traditionally happened from a near flat curve but there is nothing that says it can’t happen from here.

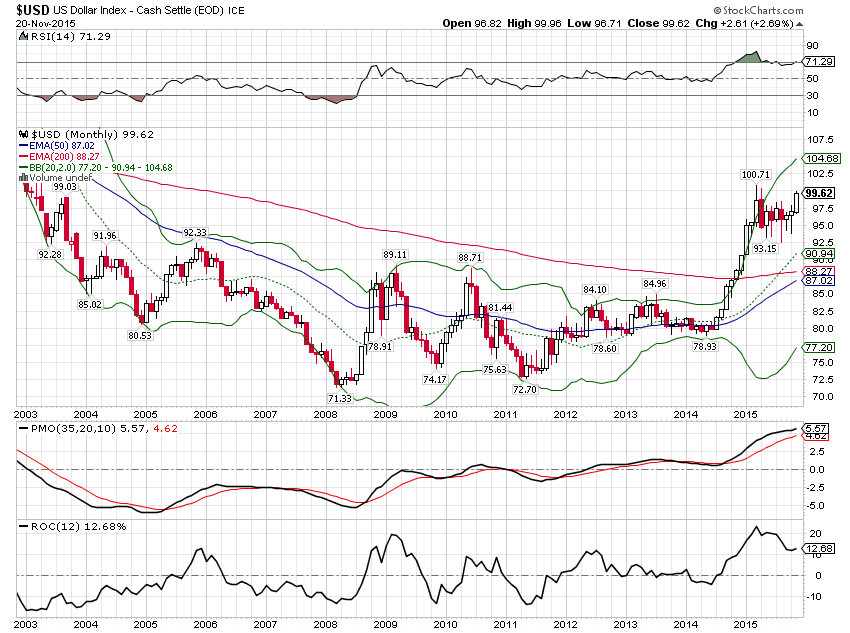

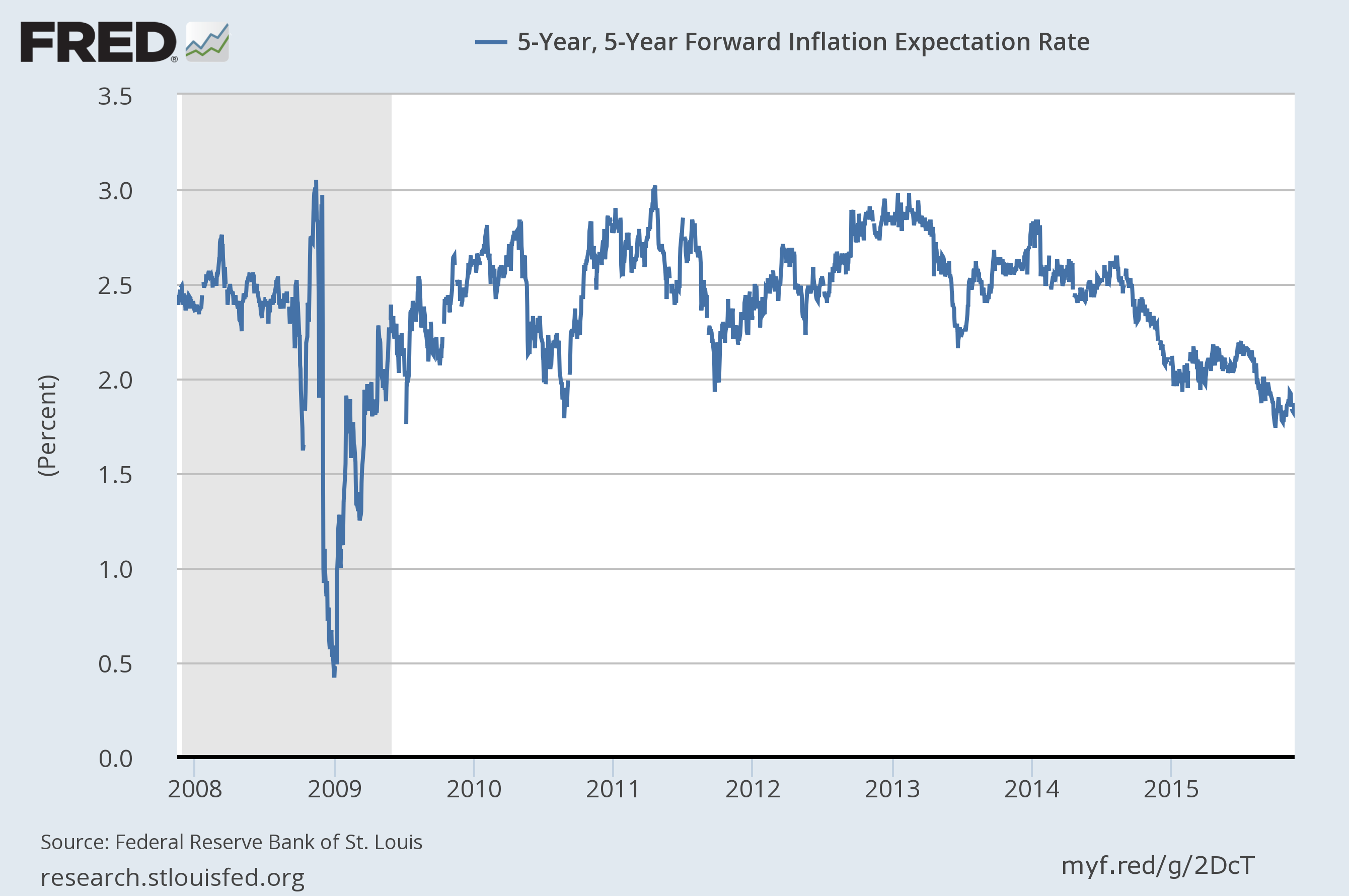

The dollar was essentially flat since the last report although there is an obvious bias toward strength. Sentiment is very bullish on dollars though and the lack of follow through ought to worry the bulls. For now though, long term momentum still points higher. That ought to continue to push down inflation expectations and be supportive of longer dated bonds. It should also continue to attract capital to the US and with little in the way of actual investment opportunity, it seems probable that it will end up in financial markets. It wasn’t coincidence that the dot com bubble happened in the midst of a strong dollar period.

The market, as I pointed out in the last report, has a much rosier view of the future economy than one would expect from the current trajectory of the data. In a sense the economy is being held up at this point by autos, housing – which might be weakening – and services. When one considers that the manufacturing/industrial side of the economy is already in recession with autos booming one can’t help but wonder what the economy would look like if they weren’t. If for any reason auto sales start to slow down, we could have a very big problem on our hands. As for services, it is a category that people talk about all the time as if it has no relation whatsoever to the manufacturing/industrial side. But of course, that makes no sense at all. To some degree, all services are dependent on the manufacturing side of the economy. It might have also escaped some people’s notice but a good part of the continued rise in services is just inflation, specifically in healthcare and rent. Which might also explain the recent rise in the use of revolving credit as incomes haven’t been rising as fast as those costs. The point is that while one is probably correct to assume the economy will continue on its current, secular stagnating, new normal 2% growth path, it wouldn’t take much of a shock to knock it off course.

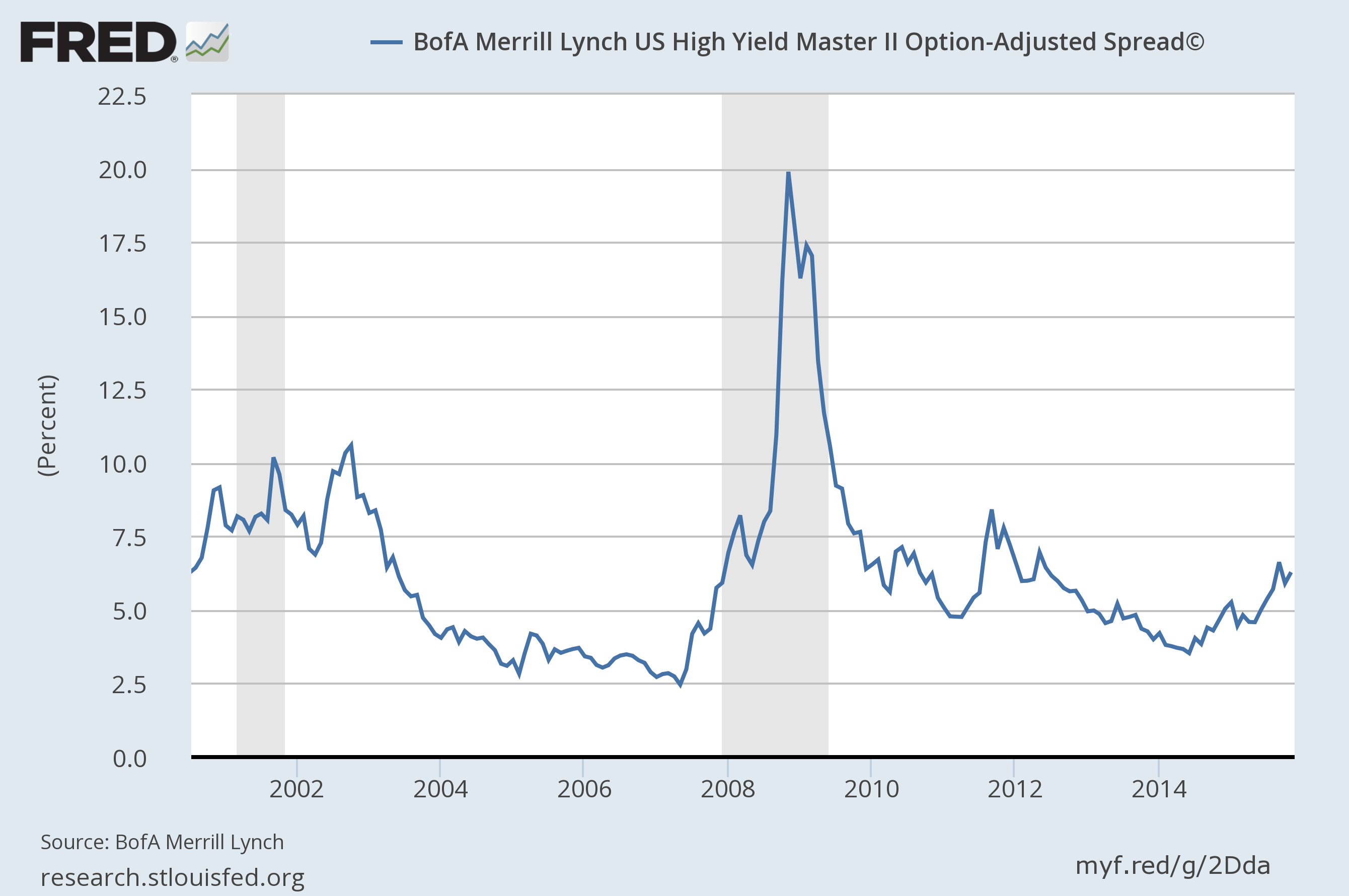

One area that is a good candidate for that shock is the bond market where credit spreads resumed their widening over the last two weeks. There are also signs of stress in a variety of money markets, a subject our own Jeff Snider has been writing about for a couple of months now and has recently caught the attention of the WSJ and Bloomberg, among others. Negative swap spreads are not supposed to happen and while the reasons for it are a bit murky I think we can say with a great deal of certainty that it doesn’t signal anything good. If I read the situation right, the movements in swaps and repos are basically signs of illiquidity regardless of why they come about. And when liquidity goes away it is replaced with volatility so expect some more.

As for the more mundane high yield credit spreads, they are back to levels higher than the start of the last recession and with the dollar rising and oil falling that seems likely to get worse before it gets better.

The Fed continues to send signals that it intends to raise interest rates at the December meeting but they also say they are data dependent. Unless they are seeing different data than I, then I don’t see how they can possibly hike in December unless it starts to get better soon. That is if they truly are data dependent, something of which I’m not convinced. It seems more likely they are concerned, and rightly so, about the potential financial instability consequences of their extended stay at the zero bound. It is unfortunate they’ve waited so long to get panicky about it though since if the data doesn’t improve and they follow through anyway, they’ll be hiking right into the teeth of a slowdown.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, Joe Calhoun can be reached at: jyc3@4kb.d43.myftpupload.com or ![]() 786-249-3773. You can also book an appointment using our contact form.

786-249-3773. You can also book an appointment using our contact form.

This material has been distributed for informational purposes only. It is the opinion of the author and should not be considered as investment advice or a recommendation of any particular security, strategy, or investment product. Investments involve risk and you can lose money. Past investing and economic performance is not indicative of future performance. Alhambra Investment Partners, LLC expressly disclaims all liability in respect to actions taken based on all of the information in this writing. If an investor does not understand the risks associated with certain securities, he/she should seek the advice of an independent adviser.

Stay In Touch