The call for minimizing the onrushing downdraft has continued, particularly in the wake of yesterday’s huge disappointment in the ISM. Where the “12%” figure had slowly entered the mainstream lexicon before, it has fast become fully incorporated into any article’s template. There are hardly any pieces about the curious manufacturing recession that don’t mention it, as it has evolved into economists’ shorthand for “nothing to see here”:

With manufacturing accounting for only 12 percent of the economy, analysts say it is unlikely the persistent weakness will deter the Federal Reserve from raising interest rates this month.

“Manufacturing is being pummeled by the stronger dollar and the weakness of global demand, but the other 88 percent of the economy continues to perform well. This won’t prevent the Fed from raising interest rates at the mid-December meeting,” said Steve Murphy, a U.S. economist at Capital Economics in Toronto.

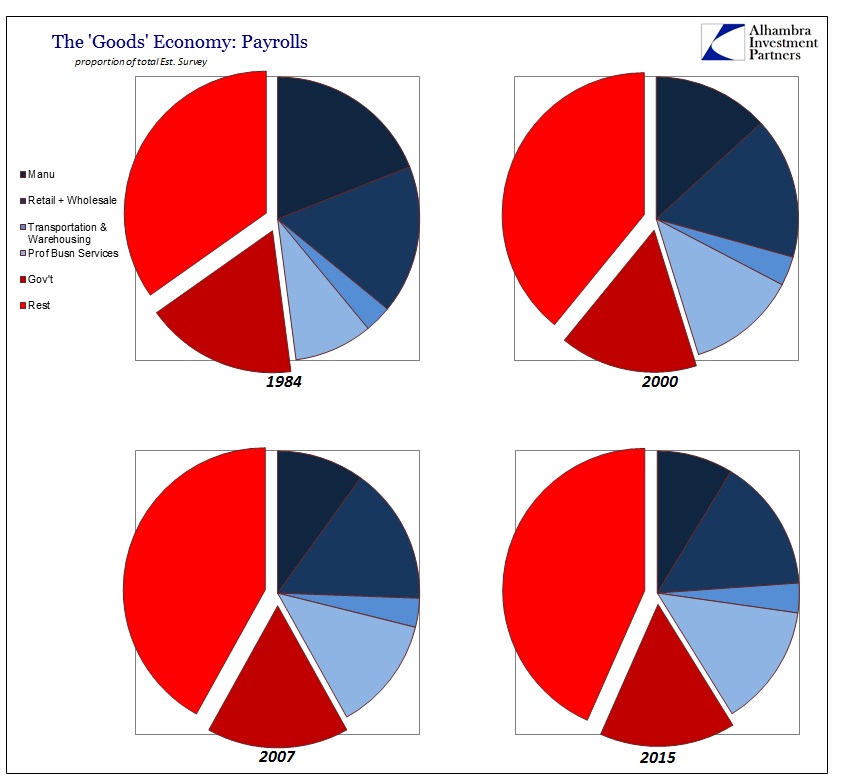

It’s an intentional fallacy, of sorts, because manufacturing isn’t the end of the process. If we are strictly speaking of the “goods economy”, the 12% is woefully undercounting. There is a whole range of activity that precedes manufacturing (relevant, of course, to commodity prices) and even more that follows. Raw material has to get out of the ground and then all of it, whatever stage of processing, needs to move around; several times. Beyond that lies the heart of this “recovery”, the retail jobs that have become the synthesis and staple of monetary redistribution in the cracked financial age.

As noted previously, the number of jobs devoted to some element of the goods economy is almost exactly in the same proportion now as it was in 2007 just before the Great Recession started – in the goods economy.

While most economists remain steadfast in working backwards from “next year”, it is incredibly important to note that this, too, is changing. Citigroup’s strategists and economists have completely “evolved” in their expectations, and not just for China.

The outlook for the global economy next year is darkening, with a U.S. recession and China becoming the first major emerging market to slash interest rates to zero both potential scenarios, according to Citi.

As the U.S. economy enters its seventh year of expansion following the 2008-09 crisis, the probability of recession will reach 65 percent, Citi’s rates strategists wrote in their 2016 outlook published late on Tuesday. A rapid flattening of the bond yield curve towards inversion would be an [sic] key warning sign.

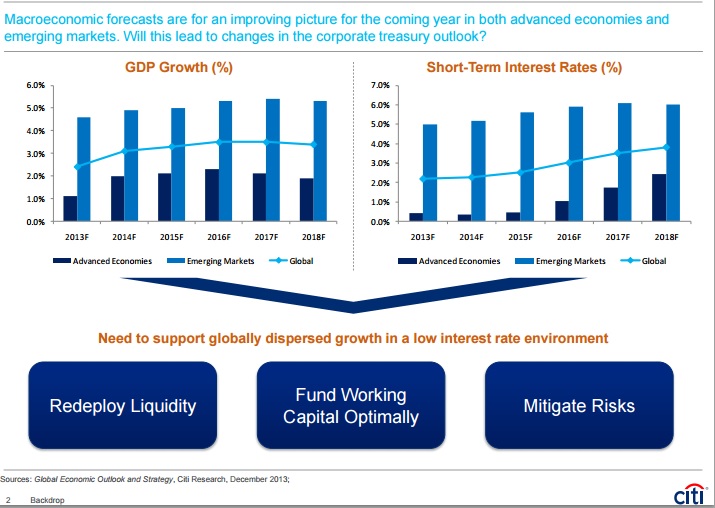

This is a dramatic shift from Citi’s prior predictions about US economic health not that long ago, and it follows the “dollar’s” increasing contagion. In their December 2013 Global Economic Outlook and Strategy, Citi called for steadily rising growth in both developed economies and, somehow, emerging markets. The reason for that is obvious, as these economists completely misread the events of 2013 as prefiguring Bernanke’s success (next year) rather than the final breath of the eurodollar standard’s last gasp (the QE lie).

In their next Global Economic Outlook and Strategy, Citi’s economists drifted into recognizing what the eurodollar was doing first overseas (without recognizing the eurodollar’s clear role). Thus, at December 2014, EM’s were starting to be forecast under duress but without much expected deviation for developed economies, especially the US.

The improvement from 2015 is likely to be led more by advanced economies rather than emerging markets. Growth in the US and UK is likely to stay around 3% in 2015-16, and we forecast modestly higher growth for the euro area and Japan.

They predicted US growth of 3% in 2015 and nearly that for 2016. For all the bluster about EM concerns, they actually predicted a slight improvement in collective EM GDP for 2015! Thus, these “singular” instances of financial disturbances remained, to Citi, just risks at that point.

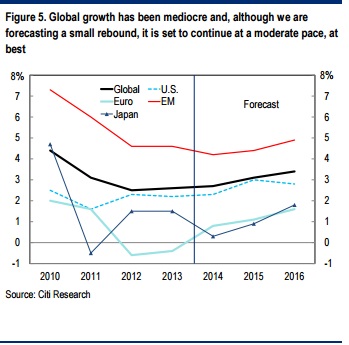

In Citi’s evolving observations, then, they have worked from no risk (Dec 2013) to risk but no deviation in economic effect (Dec 2014) to now risk being fully and globally realized (Dec 2015). In short, where almost every other economics team and “professional forecaster” again works backward from “next year” (which means modeled guesses are, for them, more “real” than current conditions) Citi is at least factoring current problems as significant and quite meaningful; i.e., common sense. A manufacturing recession is not something you would typically just ignore, especially when less than a year ago it was “impossible.”

This evolution in prediction and outlook in even Citi’s stance is remarkable just in the past few months. Less than two months ago, Willen Buiter, Citigroup’s Chief Economist and lead author for its Global Economic Outlook and Strategy, was interviewed on CNBC talking about further recessionary possibilities but still only in EM’s. In other words, he remained gripped by contending little risk of truly dark US conditions as recently as October 13:

He [Buiter] added that countries like the U.S. and the U.K. might not feel the full effects of a recession but said that global growth would be “well below trend” with a “widening output gap.” He said there would a whole range of other “dysfunctionalities” that have been building up since the global financial crash of 2008.

What has changed since? For one, Citi seems to have sensed that the Fed’s role is only to make matters worse, thus their citation of yield curve inversion. More than that, the “manufacturing recession”, for whatever proportion of the economy it might directly effect, has become real not just in more indisputable fact but more so in what it suggests about the direction of the economy, services and all. Citigroup may still be lagging financial indications, especially the “dollar”, that were suggesting this fate long ago and projecting it into commodity and fixed income markets, but at least they appear to be approaching it with a refreshing accountability to something other than Yellen’s models and “next year’s” certainty.

The rest of the class of economists will have to be dragged kicking and screaming, downplaying and belittling, all the way into the looming darkness.

1. Dollar doesn’t matter, indicates strong economy relative to the world

2. Dollar matters for oil, but lower oil prices mean stronger consumer

3. Manufacturing slump doesn’t matter, only temporary

4. Manufacturing declines are consumer spending, but only a small part

5. Manufacturing declines are becoming serious, but only from overseas

6. Maybe domestic manufacturing recession too, but the rest of the economy is strong

7. Rest of the economy might not be as strong as thought, but only an “earnings recession.”

8. Maybe full recession, but only a small probability.

9. …

Brazil, Canada, Russia, China, Japan…that’s a pretty good mix of both DM and EM recessions, not to mention Europe that, at best, straddles the line between open contraction and but a lack of it (which counts, these days, as a recovery) and all without any detectable reaction to innumerable monetary “inputs.” Global trade in freefall, manufacturing in the US already in “recession”, retail sales domestically (which links it all) among the worst in the entire series all year and the continued confusing case of crashing currency and financial disruption. Truly nothing much to worry about?

That now even one bank’s orthodox economics team is realizing the possibilities is highly significant, especially as the “impossible” becomes more and more just the start. If nothing else, the trajectory has gained more than enough clarity to see where all this, US and the rest, is heading. To paraphrase Churchill, this might be the end of the beginning.

Stay In Touch