The fact that there is almost universal recognition of a “manufacturing recession” not just here but spreading across the world is a significant change. After resisting and ignoring as much as possible for more than a year, economic weakness is now no longer unthinkable. This is, however, no mere academic exercise as there are very real consequences as the former narrative dies. That former story, contained in everything of “transitory” to “next year”, had very real economic impacts. We are just now starting to see the transition.

Last week, I paraphrased Winston Churchill in setting the context for the evolution of Citibank’s economics and rates teams going,

…from no risk (Dec 2013) to risk but no deviation in economic effect (Dec 2014) to now risk being fully and globally realized (Dec 2015). In short, where almost every other economics team and “professional forecaster” again works backward from “next year” (which means modeled guesses are, for them, more “real” than current conditions) Citi is at least factoring current problems as significant and quite meaningful; i.e., common sense. A manufacturing recession is not something you would typically just ignore, especially when less than a year ago it was “impossible.”

As more of these changing probability distributions are unleashed here in late 2015, business itself will have to undergo its own re-alignment with what is already a far different probability spectrum. The prior period, containing most of the economy up until now, was characterized in general business as “concern but holding out for the best case” and thus no large-scale actions in terms of production and adjustments in inputs. Like manufacturing, it has been more of a fine-tuning in order to wait out the “transitory” weakness. More widespread realization that “transitory” was never a real probability means that the recent awakening and realization is “the end of the beginning.”

No longer being able to deny that weakness is both broad and, alarmingly, sustained means taking the “next” steps to adjust. With no quick turnaround at hand, serious adjustment plans must be put into action; that means giving up on the recovery and being more realistic about the potential downside to the point of actually preparing for it. Hope is gone; prudence takes its place.

That will and has occurred first in the commodity industries, the very place that “transitory” as an idea was meant as a bulwark against all-too-realistic pessimism. More so oil than others, still the characterization of commodity crashes as temporary was surely the rational expectations theory component of stemming the difficult, possibly recessionary tide – dare I write, “contained” to just oil. The news this morning from Anglo American is yet another nail in the coffin of “transitory” and more evidence for the shift into the next phase after the “end of the beginning.”

The mining and commodities firm announced that it will be cutting its business by about 60% (which is why the move was covered widely, so jarring against the determined recovery and “transitory” ideas), closing mines and selling “assets.” The company’s CEO was plain about which parts of the business would be targeted in what is seemingly an unappreciated indication about both economics and the current state of finance combining to make this recessionary turn. Telling reporters on a conference call that, “Any asset that is cash-negative will not remain in the portfolio it is a strategic call and we are not going to look back”, this is clearly more than just giving up on Yellen’s delusional recovery idea (not just in commodity prices).

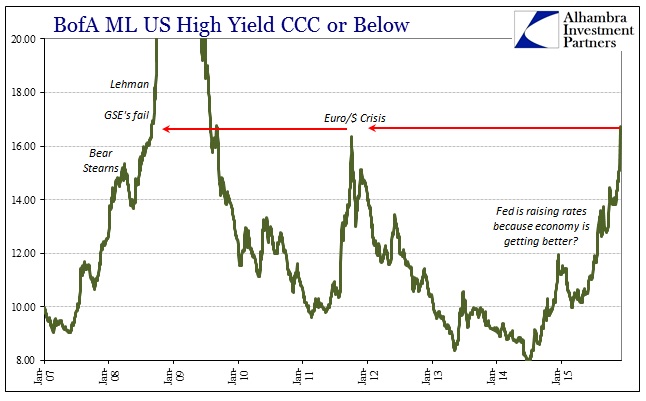

Targeting specifically cash negative businesses and business lines screams out financing, as does cutting the dividend in half. Is it any wonder? The junk bond market, and further erosion in spreads and now “investors” and banks paying a little more attention to details in financing arrangements (cov-lite and even covenant-less deals, all the rage in 2014, are gone now), more than suggests the dreaded credit crunch.

Anglo American is far from alone, as scores of oil, natural gas, and mining companies are feeling the pain from low prices. A number of commodity-related businesses have either declared bankruptcy or fallen behind in their debt payments. Even more frequent have been layoffs — more than 250,000 workers in the oil and gas industry worldwide, with more than a third coming in the United States.

Anglo’s CEO assured reporters that despite the drastic nature of the announcement, not all the 85,000 “cuts” would be jobs lost; the firm plans as much in divestitures and thus asset sales.

A company spokesperson said the job cuts would be made through asset sales and internal cuts: “Bear in mind that these include assets that we will sell, so the 85,000 jobs don’t [all] disappear as many will be employed by new owners of those mines that we sell.”

The problem with that thinking is that it assumes there is demand for those assets at a price that maintains the negative cash flow labor inputs. That is problematic on its own, but Anglo isn’t likely to have the restructuring space all to itself for very long.

“Anglo American, like all of its counterparties in the mining sector, has found there is no more fat to be cut and, as had been speculated for the last week, it had to face the reality that it could no longer pay out the dividend,” said Alastair McCaig, market analyst at IG.

“Where one goes, others will follow and the possibility that BHP Billiton or Rio Tinto might be forced into similar action now looks increasingly likely.”

If everyone joins Anglo on this other side the beginning, who will be left to buy all these firesale assets especially since there is not much of a “market” left to finance all that speculative and negative cash flow activity? Finance becomes economics and now moved out of hope and into realism events tend to quicken and deepen quickly. If it becomes apparent that “getting out” is not so easy, there tends to be a rush toward the exits – a fact that applies, again, to both economy and finance; real jobs and the debt that has kept them in existence this long. Perhaps Anglo has already glimpsed the first such rush?

Anglo American is just one company, but this is beyond purely anecdotal. With manufacturing closely following toward its own and related paradigm shift, there is this natural “contagion” to consider more widely.

1. Dollar doesn’t matter, indicates strong economy relative to the world

2. Dollar matters for oil, but lower oil prices mean stronger consumer

3. Manufacturing slump doesn’t matter, only temporary

4. Manufacturing declines are consumer spending, but only a small part

5. Manufacturing declines are becoming serious, but only from overseas

6. Maybe domestic manufacturing recession too, but the rest of the economy is strong

7. Rest of the economy might not be as strong as thought, but only an “earnings recession.”

8. Maybe full recession, but only a small probability.

9. …

The last on that list, #9, is “stop denying what is plainly in front of you and relying upon mainstream economic forecasts, and start making major adjustments while you still can.” Strong dollar indeed.

Stay In Touch