If top level sales are not to ever become what economists projected, as retail sales left little doubt in December, then what is left is to no longer hold the line as best as possible on resources and inputs. With inventory already massive, production must be brought down to equalize sales at each level plus already accumulated(ing) inventory. With the Empire State Fed regional manufacturing survey crashing in December, it was a clear indication that the next phase of the adjustment may have already begun.

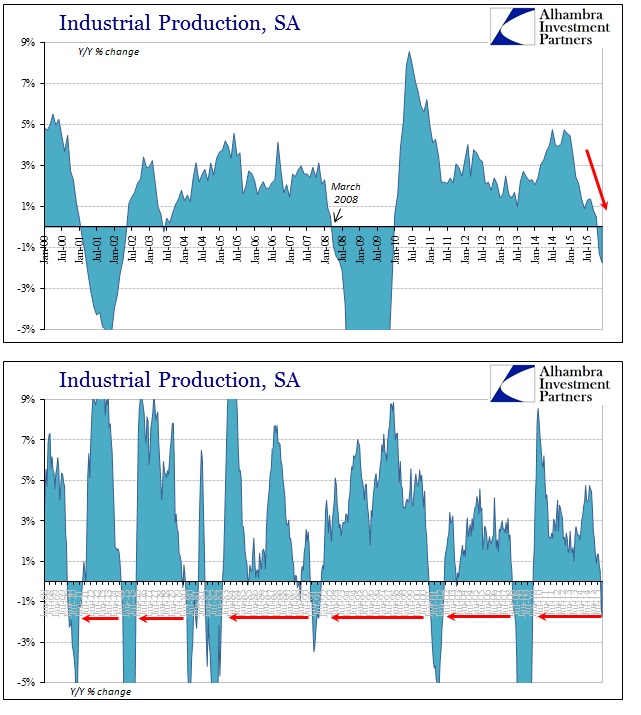

In November, US industrial production turned negative for the first time in the “cycle”; ominously being reported by the Federal Reserve on the same day that the central bank’s policymaking body attempted to suggest an opposite economic condition. At -1.2% (revised now to -1.3%), it left little doubt as to the overall economic implication; only three times in the 136 months (not counting Nov. 2015) going back to 1950 had IP been lower than -1% without immediate proximity to recession (and all three of those months were back in the 1950’s). December’s IP estimate leaves even less doubt, figured at -1.8% currently. Only 114 times (not counting Dec. 2015) has IP been less than -1.7% and every single one of those months is associated with full economic recession. There just aren’t any false positives – which is one reason the NBER looks to IP in dating cycle peaks.

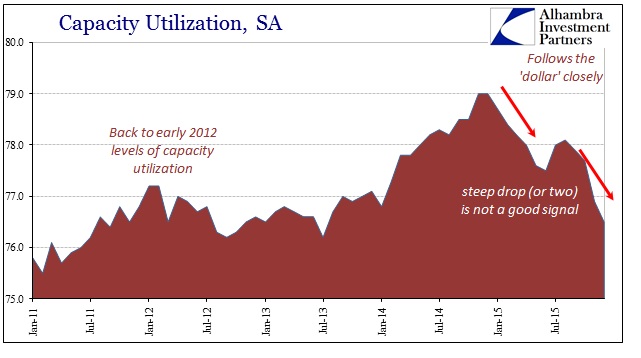

It isn’t just raw IP, either, that is concerning. Corroborating the drastic implications has been both the speed and scale in the relapse in capacity utilization. Measuring idle resources, essentially, the reduction in utilization is a hugely important measure of growing inefficiency which can only lead to a break in paradigm as I described above. The depth achieved already through 2015 is simply alarming, as capacity utilization in December brings US industry all the way back to November 2011.

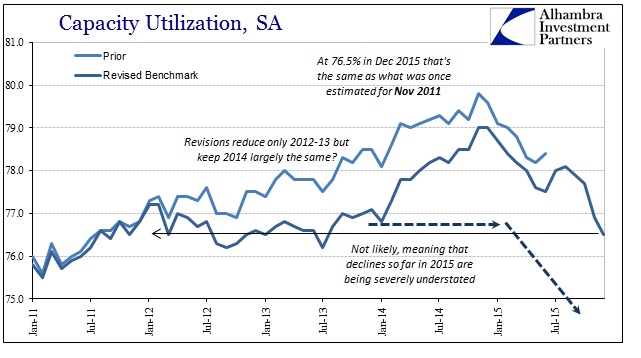

Revisions in 2012 and 2013 obscure, somewhat, just how much of a decline has been witnessed in the past twelve or thirteen months. The prior estimates for capacity utilization shown above are what a recovery trajectory should look like, so by comparison the dropoff in 2015 away from the traditional recovery track is more like a classic manufacturing cycle being completed.

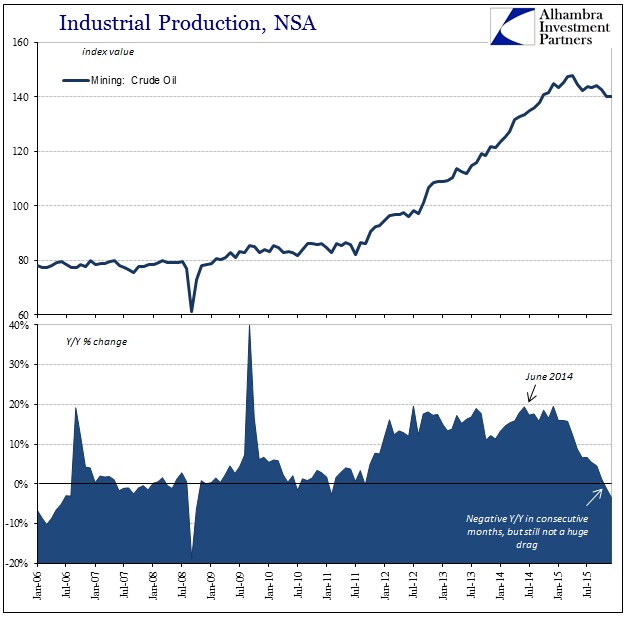

As has been the case all year, production in oil and energy has not yet become a significant drag on overall IP. Oil production has turned negative, but not yet dramatically so; meaning that broad industry is by itself already in contraction oil or not, but, more importantly, the oil industry is just now about to start exhibiting a significant downward pull.

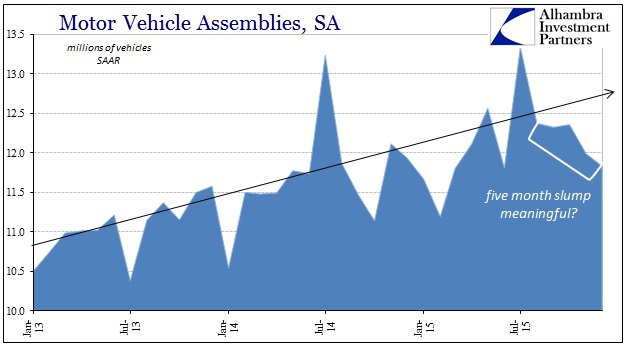

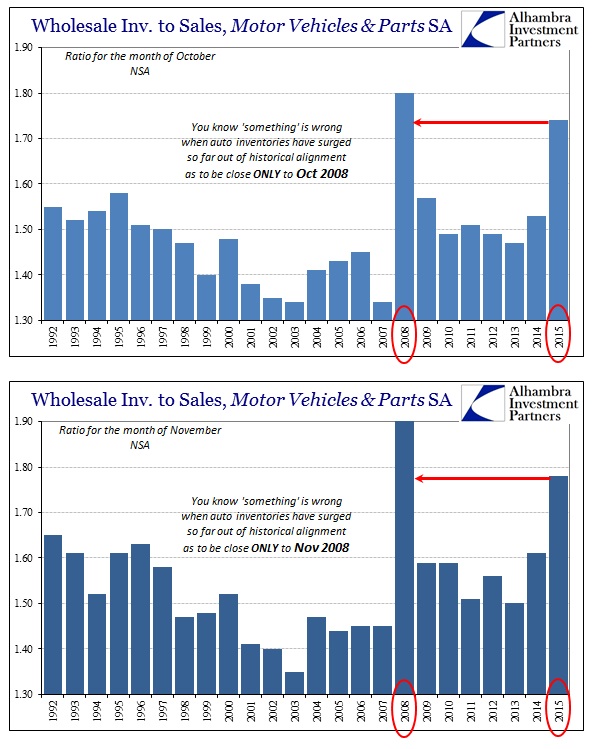

As ominous as the trajectory of energy production might be, the state of motor vehicles might be even more concerning. Everyone (now) expects production levels to fall in oil, but autos are still believed to be the bedrock foundation of whatever was of this recovery. November estimates of wholesale inventories of autos (which are counted as sold off factory floors) were quite alarming, then the first rush of estimates for December auto sales were significantly weak. The IP figures provide a glimpse at domestic auto production through assemblies which have slumped now for the past five months running. Auto production and assembly is notoriously volatile, so it is the duration of the downturn that is significant – especially in the context of, again, inventory.

If I were to characterize manufacturing and industry in 2015, it would have to be holding to the dreams of full recovery while adjusting in minor turns to the persistent disappointment. This year starts with that first recession-type phase perhaps already turned to a second, where adjustments are no longer so minor as hope and dreams fade to harsh reality. It’s a bitter inflection, no doubt about it, especially since the mainstream focus on payrolls seemingly assured something entirely different. With overseas economies sinking fast and hard, the fact that US consumers brought no Santa Claus is likely the last gasp. The IP numbers suggest the cleanup may have already begun.

Stay In Touch