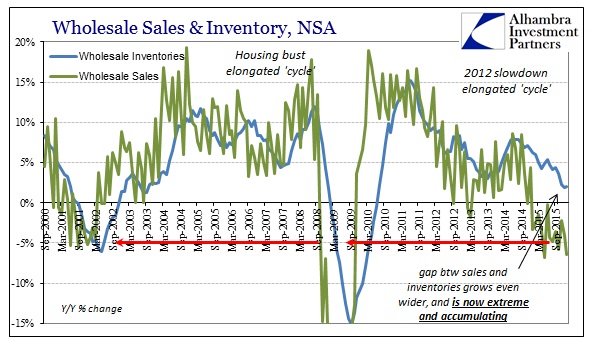

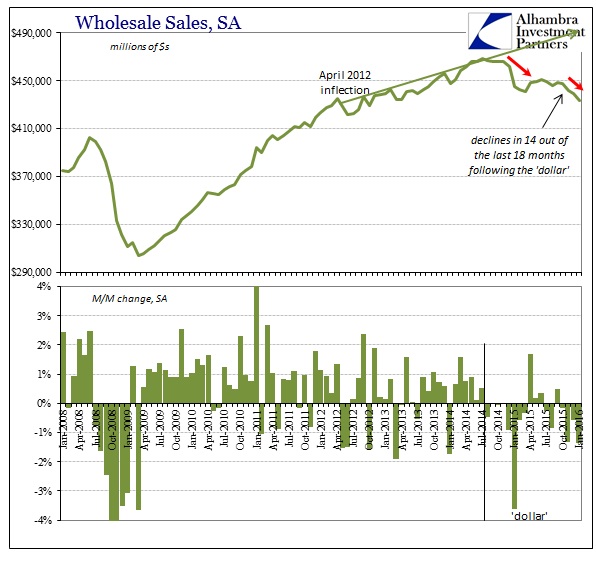

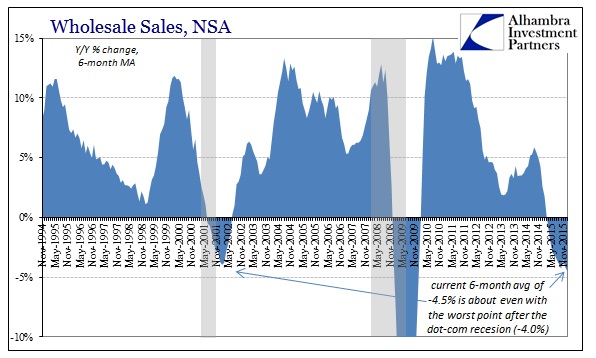

Unlike retail sales in January, wholesale sales won’t need revisions to become highly negative in either the seasonal or unadjusted versions. On a seasonally-adjusted basis, wholesale sales declined rather sharply in January (-1.35% M/M), the fourth consecutive decline, sixth out of the past seven months and making fourteen of the past eighteen since all this began. On an unadjusted basis, wholesale sales dropped by 6.4% which was the second worst month of this “recovery” period, meaning consistency no matter the format.

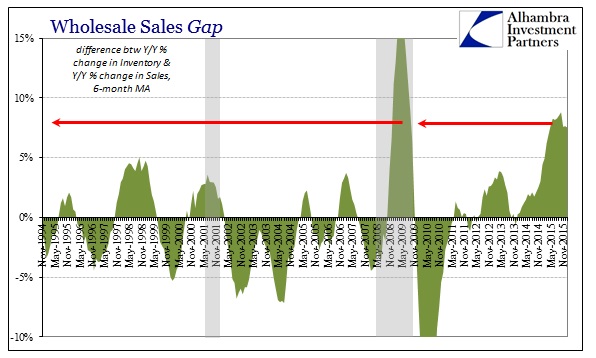

Yet, inventory grew in January for both terms. Seasonally-adjusted, inventory rose 0.3% M/M after being flat in December, while unadjusted inventory accelerated slightly to +2.0% Y/Y in January following 1.8% (more consistency). Immediately the disparity seems like petroleum and oil prices but the broader range of wholesale sales, in particular, have come under sharper and more acute pressure in the past few months. In fact, non-petroleum wholesale sales have contracted for the third consecutive month in January.

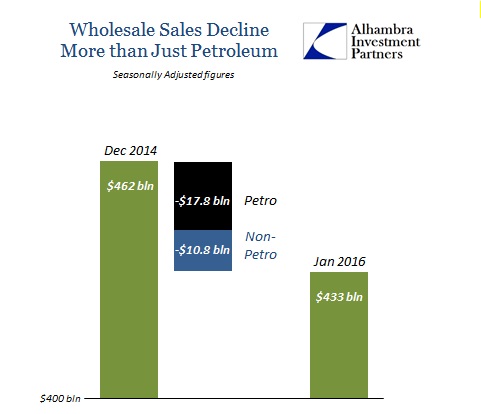

Since the start of 2015, on a seasonally-adjusted basis overall wholesale sales have declined by about $28.5 billion, from $461.7 billion to $$433.1 billion in January 2016. Of that contraction, $17.8 billion was due to petroleum sales and prices while a rather alarming $10.8 billion was wholesale sales elsewhere. In the wholesale level of the supply chain, contraction is widespread and growing which means the inventory problem is too.

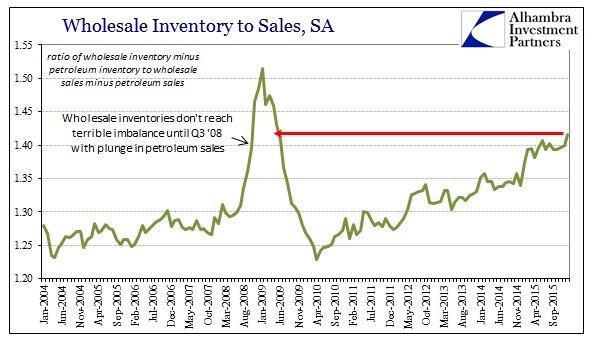

As wholesale sales continue at a contraction slightly worse than the dot-com recession, inventory grows at every point and in every category. Additions to inventory have certainly slowed, but it does not yet suggest full-scale cutbacks despite production cuts in manufacturing (and whatever might be happening on the retail level). The imbalance only drags on further, mimicking more closely the extremes of the Great Recession.

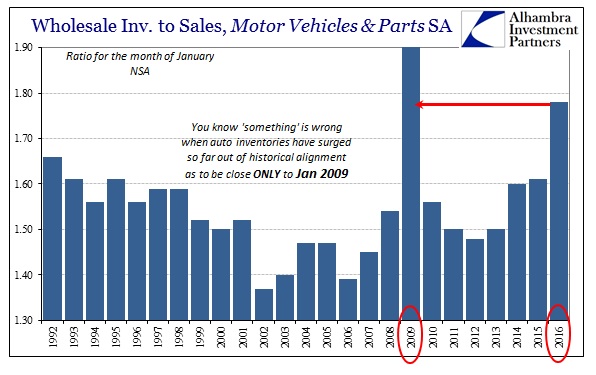

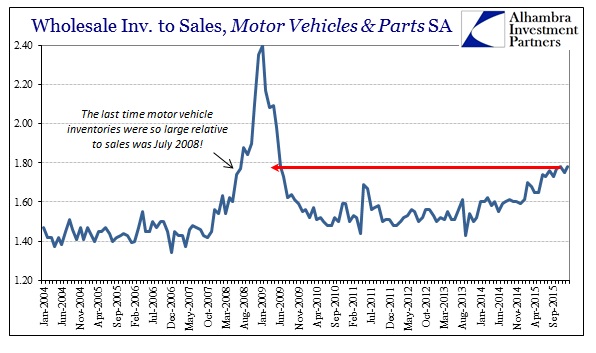

Even motor vehicles are stocked at recessionary levels. The inventory-to-sales ratio for autos remained so high in January 2016 that they are totally unlike any other January in the entire series except for January 2009!

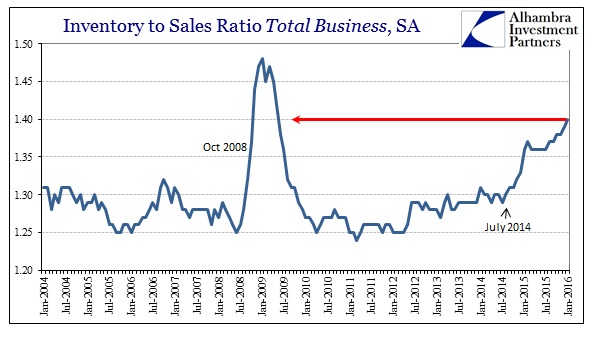

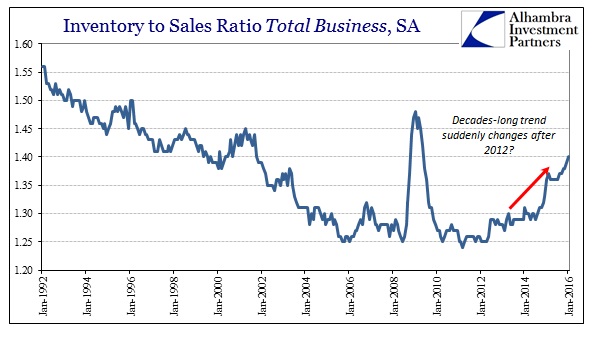

Again, the extreme inventory imbalance is everywhere, leaving the aggregate measure of Total Business Inventory-to-Sales at another new high of 1.40. The last time inventory was this far out of balance was May 2009; that ratio of 1.40 for January 2016 is higher than all but seven months of the Great Recession. What’s worse, as is clear on the chart immediately below, the shift in inventory balance aligns with the “rising dollar” period which is, again, far more than just oil prices.

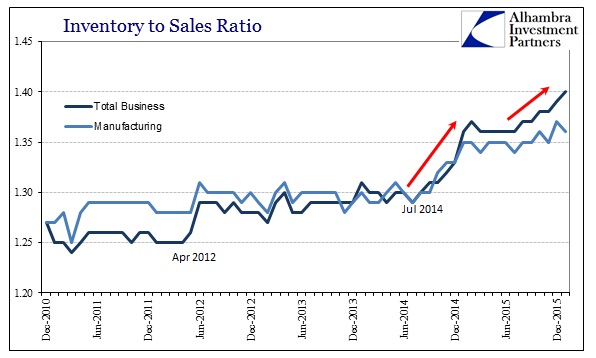

The inventory-sales-ratio for Total Business in July 2014 was 1.29, meaning a +0.11 gain over the past eighteen months. That was similar to the sharp rise from June to October 2008 (from 1.25 to 1.37) which indicates the differences in context despite the similarities in the extremes. In other words, heading into fall 2008 was the sharp and quick recession format that conformed to historical experience versus what we see now as just a slowdown that for whatever reason grinds on no matter what.

The slope of the negative imbalance might be different, but across the whole supply chain inventory is accumulating in the extreme. That is how long this process has been dragging on, almost like the proverbial boiling frog. Manufacturing has already been pared back (here and especially China) to no avail so far, not even the slightest hint of convergence to sales. That would suggest still more adjustments to come without suggesting anything about when or if the slope of these declines might change. Maybe, like 2008, businesses are waiting for a financial trigger to force sharp and much deeper realignment. Or it could be that we are witnessing something entirely different and new; the same frustrating, lingering process that is plaguing Brazil and China.

The latter option would at least be consistent since US consumers are at the center of all of this, here and overseas. I would not yet, however, discount the former possibility as more extreme inventory levels hold only greater potential for the sharper reversion trend.

Stay In Touch