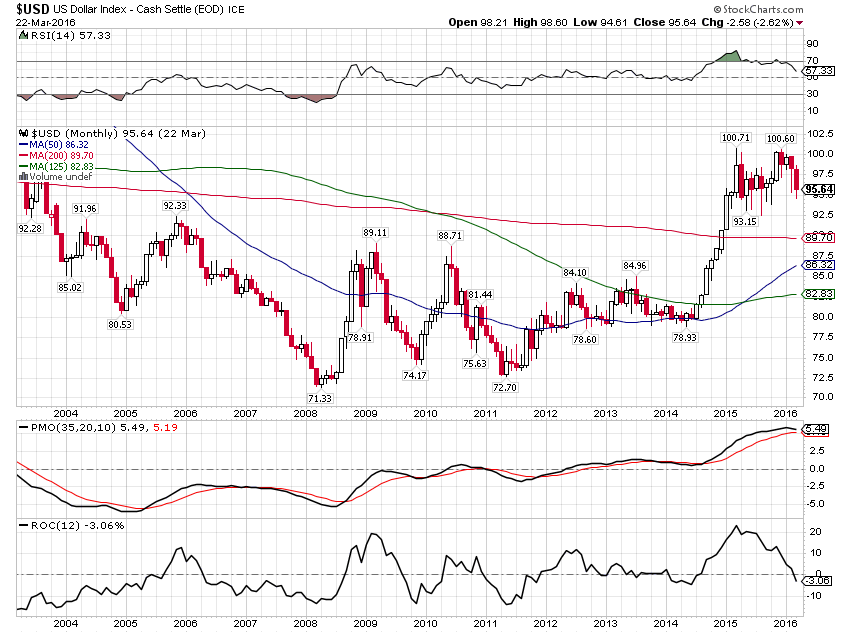

The last month has seen a shift in the fortunes of energy stocks with the sector leading the pack with a return over 11%. Will it last? That probably depends more on the direction of the US dollar than it does any of the alleged production agreements that get so much press and rarely produce anything other than a press release. The price of oil, which is the primary driver of energy sector performance, is very sensitive to changes in the value of the dollar.

If we are to invest in a single sector it seems axiomatic that we would only do so if the sector is expected to outperform the market as a whole. One might consider that in the context of risk too, in that a sector with a lower volatility might still be preferable to the market index. But with energy the volatility is actually higher than the S&P 500 so the return needs to beat the index by some margin to produce the same risk adjusted return. A ratio chart shows that hasn’t been the case basically since the crisis except for a brief period in 2010/11.

On the other hand, look at the left hand side of the graph when XLE did outperform the S&P by a significant margin. That coincides with a period of a very weak dollar when crude prices were on their way to $140/barrel.

For now, despite some near term outperformance, there has not been a sufficient change in long term momentum to justify a purchase. If the dollar breaks down and goes lower – something that wouldn’t surprise me – then energy will likely be an outperformer again. If not, then it is probably best to look elsewhere.

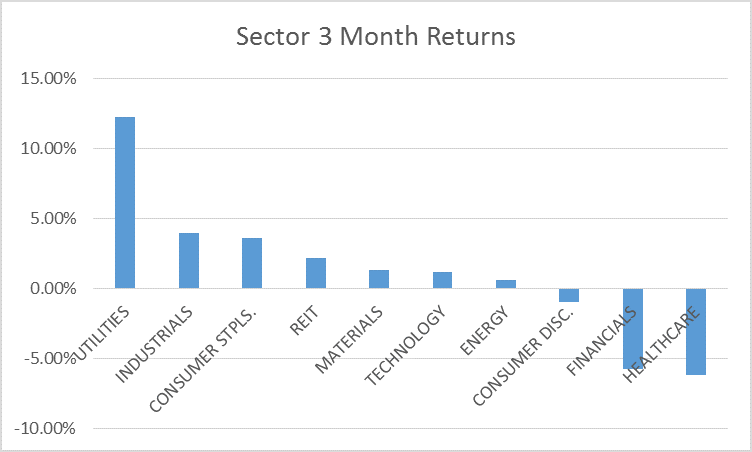

If we take a step back and look at 3 month returns instead, the picture changes. The top performers over the last 3 months include Utilities and Staples, two defensive sectors. Industrials come in second, a bit of a surprise considering the state of manufacturing right now. It appears though that this is more a market phenomenon than anything specific to the sector as Industrials tend to perform in line with the market over time.

Weak dollar sectors – XLE and XLB – are outperforming short term but if that is to continue we’ll need to see the dollar continue its recent weakening. And that will depend to a large degree on the performance of the global economy. Anything that narrows the monetary policy divergence seems likely to weaken the dollar. Technically, we are close to a momentum sell signal on the dollar index but we aren’t there yet.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, Joe Calhoun can be reached at: jyc3@4kb.d43.myftpupload.com or 786-249-3773. You can also book an appointment using our contact form.

This material has been distributed for informational purposes only. It is the opinion of the author and should not be considered as investment advice or a recommendation of any particular security, strategy, or investment product. Investments involve risk and you can lose money. Past investing and economic performance is not indicative of future performance. Alhambra Investment Partners, LLC expressly disclaims all liability in respect to actions taken based on all of the information in this writing. If an investor does not understand the risks associated with certain securities, he/she should seek the advice of an independent adviser.

Stay In Touch