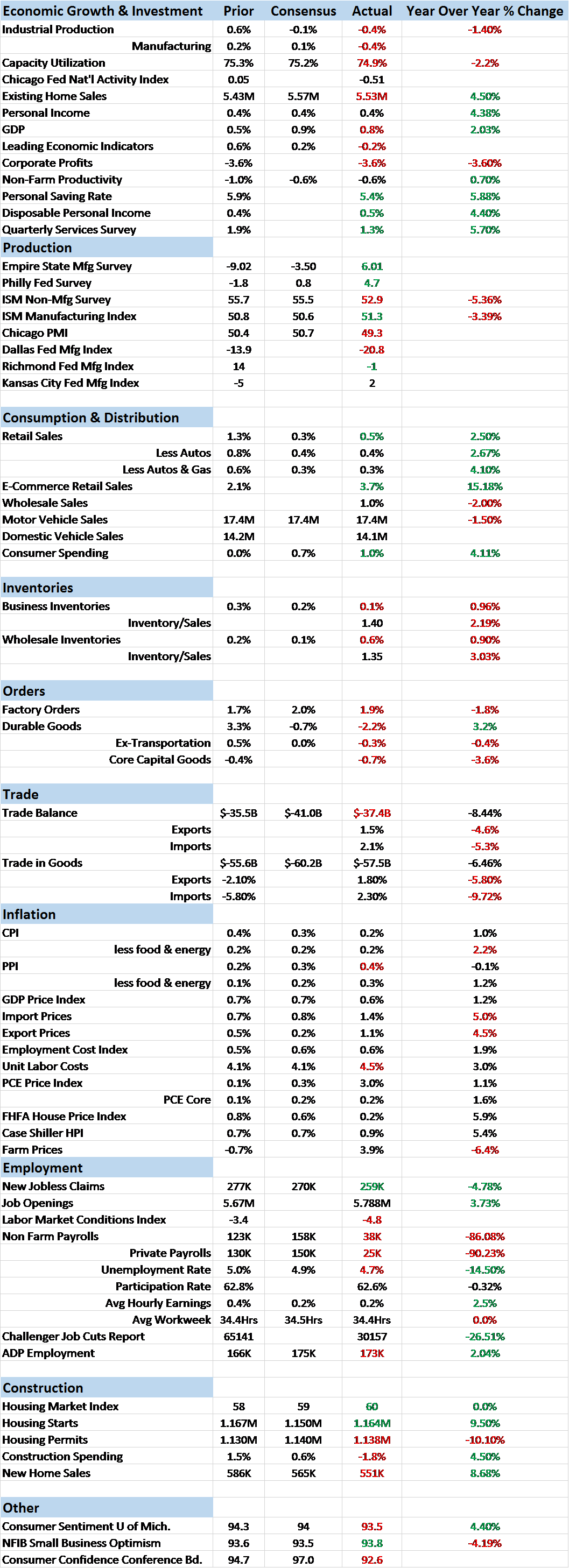

Economic Reports Scorecard

While everyone was focused on the potentially negative impact of Brexit, the Census Bureau was reporting evidence of actual economic weakness in the form of the durable goods report. The report was weak pretty much across the board but the weakness in autos is particularly concerning. The auto industry, along with construction, has been a leader in the recovery – such as it is. Perhaps the most negative part of the report though was core capital goods orders and shipments, down 0.7% and 0.5% respectively. Recessions and recoveries are generally and usually led by investment and the lack of it in this expansion is exhibit one in the secular stagnation story. And it isn’t getting any better apparently.

The durable goods report confirmed the industrial production report where manufacturing pulled down overall production by 1.4%. The regional Fed surveys provided some positive signs with Empire State, Philly Fed and the KC Fed all rebounding to positive territory. Even those were a mixed bag though. The details of the Philly report were widely negative despite a positive headline. New orders, unfilled orders and employment were all deeply negative.

The housing market reports were generally positive with the exception of permits which are significantly lagging starts, down 10.10% year over year. New home sales were strong but builders were offering large concessions on price to move the merchandise; median prices were down 9.3%.

The US economy is weak but not recessionary. Manufacturing is in recession now although there may be signs of stabilization. The business inventory/sales ratio actually fell 0.1 last month, not much but if you want to be optimistic, it could mean inventories have peaked. Retail sales have not been growing very rapidly but they do continue to expand at a 2.5% year over year rate. And e-commerce sales are rising rapidly. Some of the funk in retail sales may just be the industry adjusting to new buying habits. Inflation, meanwhile, is still conspicuous mostly by its absence but core CPI is running a bit hot at 2.2%, not that I expect the Fed to do anything about that.

The broad Chicago Fed National Activity Index is a good reflection of the overall economy. Last month’s reading of -0.51 means the economy is growing but at a below average rate. The weakness is not particularly deep but it is broad. The Atlanta Fed’s GDP Now shows Q2 GDP growth at 2.6%, a lot better than Q1 but not much of a rebound; the US economy doesn’t need any help from Brexit to look weak.

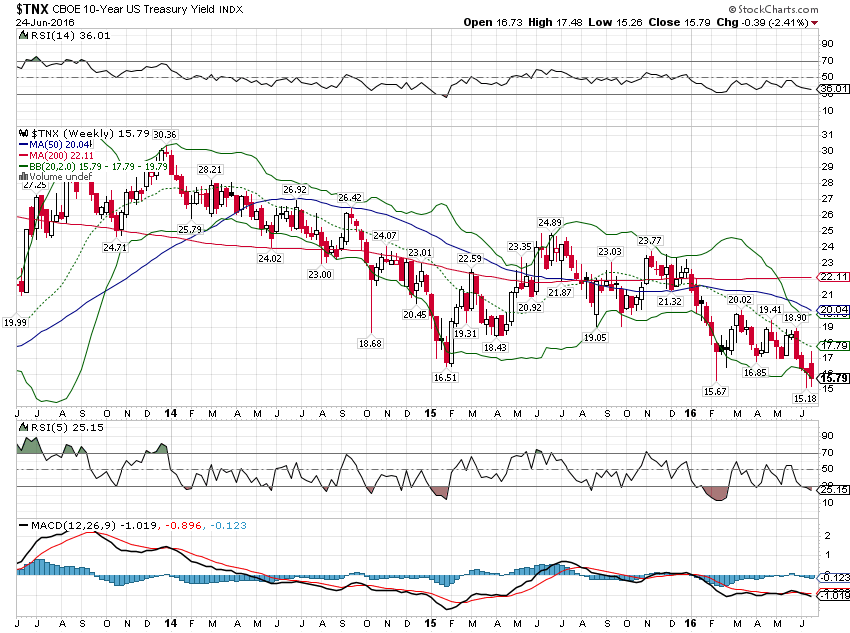

You don’t need to parse the incoming economic data too closely to verify the weakness of the global economy. A quick glance at the bond market will suffice. The 10 year Treasury note yield did not make new lows with the Brexit vote but that is merely a matter of time unless we see a sudden growth spurt from out of the blue. With a yield of 1.58%, the 10 year is saying nothing good about the US economy.

Note: The St. Louis Fed has recently revamped their FRED website and it is all I’ve come to expect from government. They have made it harder to search and more disorganized. And apparently they were so busy screwing up their website they didn’t find the time to actually, you know, update the data from Friday. I see no point in posting charts with data missing so I’ll use alternative charts to try and show what I need to show. Hopefully, the St. Louis Fed will get its act together for the next update in two weeks.

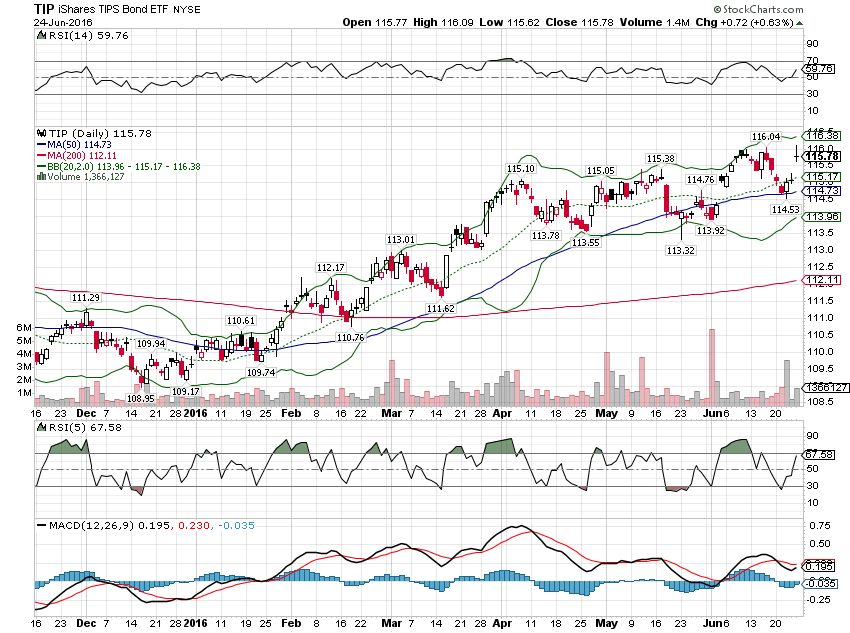

Real yields dropped Friday as well, Brexit reducing expectations for real growth. Like nominal bonds, TIP is near its highs:

The yield curve continues to flatten, long term bonds outperforming short term:

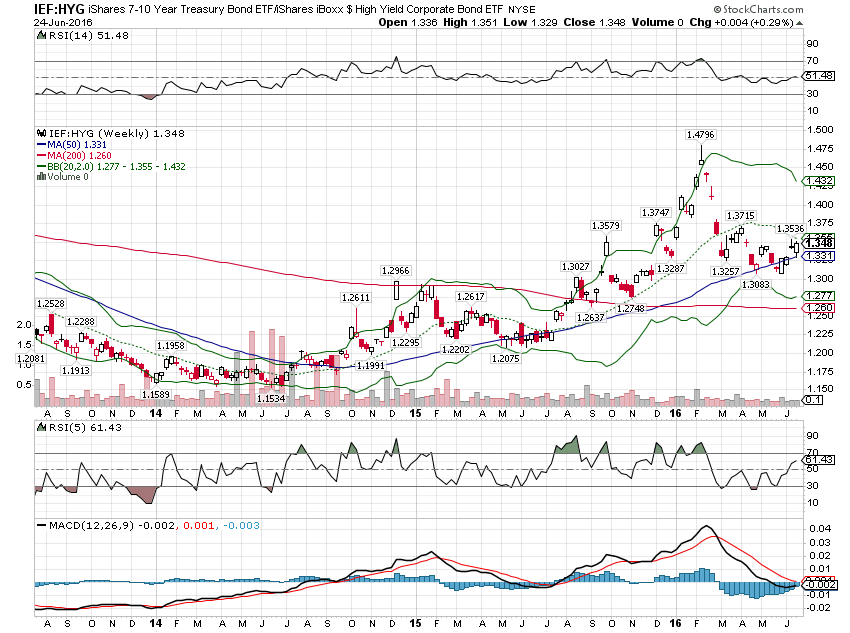

Credit spreads had been narrowing but widened Friday. Treasuries are continuing to outperform junk:

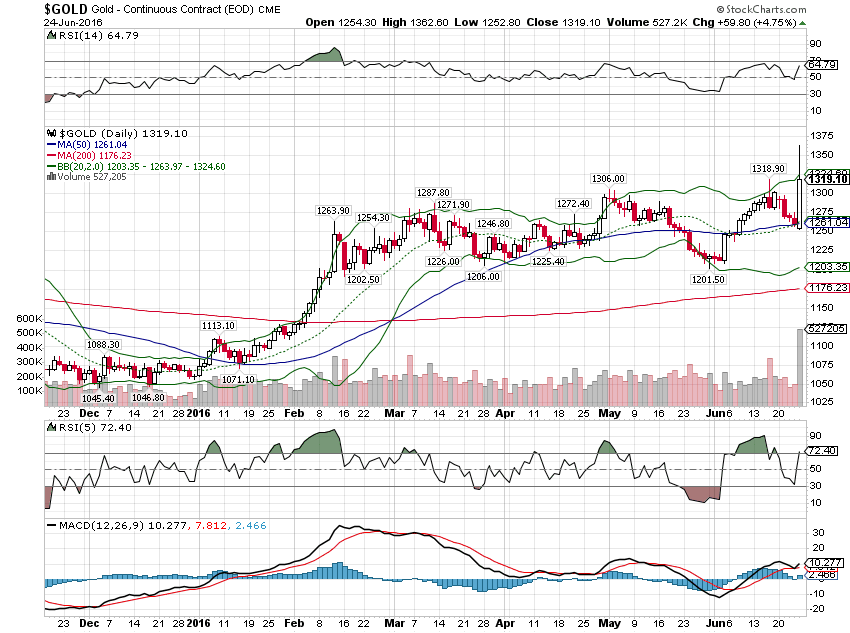

Gold did make new highs for this move but only marginally. Further gains may be limited if the dollar keeps rising (although that isn’t my base case):

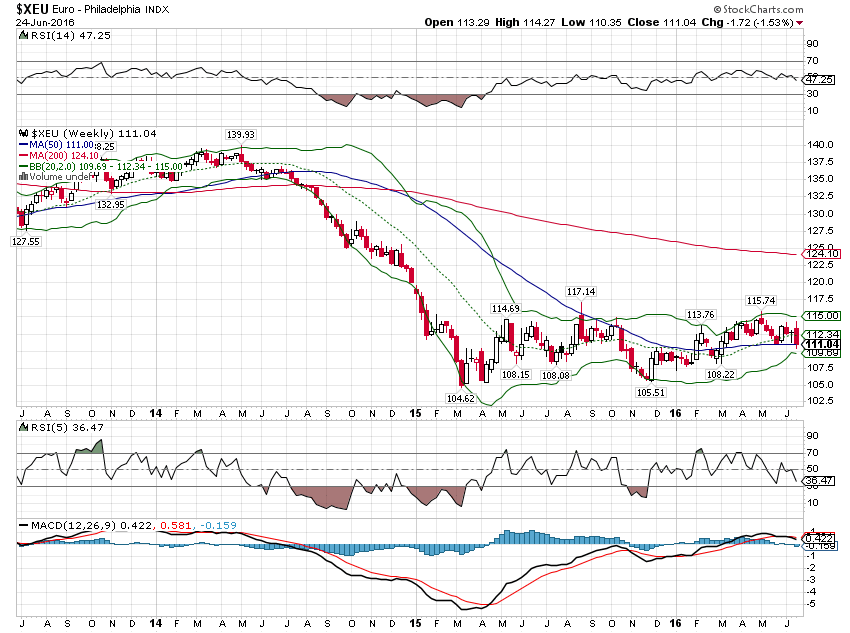

The dollar did rally Friday but frankly, I was surprised it wasn’t stronger based on the rhetoric about the implications of Brexit. Maybe the dollar will keep rising but the resilience of the Euro Friday was pretty impressive.

If Brexit is really so bad, such a harbinger of doom for the EU, why didn’t the Euro fall further?

The Brexit vote moved markets Friday but, at least for now, it didn’t really change anything with regard to economic growth, globally or in the US. Global growth was weak before the vote and Brexit doesn’t improve the outlook. Whether it makes it a lot worse is a matter of debate for now and something we won’t know for a long time.

In today’s interconnected world, it is currencies that are the canaries in the coal mine, the first to react to changes in growth and inflation expectations. The next couple of weeks will probably provide some important clues about the ultimate impact of Brexit. It is often the case that the knee jerk move in markets is wrong and this may be no different. For now, I see no need for changes to our portfolios based on Brexit but my focus will be on the Dollar, Yen and Euro for hints about the future.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, Joe Calhoun can be reached at: jyc3@4kb.d43.myftpupload.com or 786-249-3773. You can also book an appointment using our contact form.

This material has been distributed for informational purposes only. It is the opinion of the author and should not be considered as investment advice or a recommendation of any particular security, strategy, or investment product. Investments involve risk and you can lose money. Past investing and economic performance is not indicative of future performance. Alhambra Investment Partners, LLC expressly disclaims all liability in respect to actions taken based on all of the information in this writing. If an investor does not understand the risks associated with certain securities, he/she should seek the advice of an independent adviser.

Stay In Touch