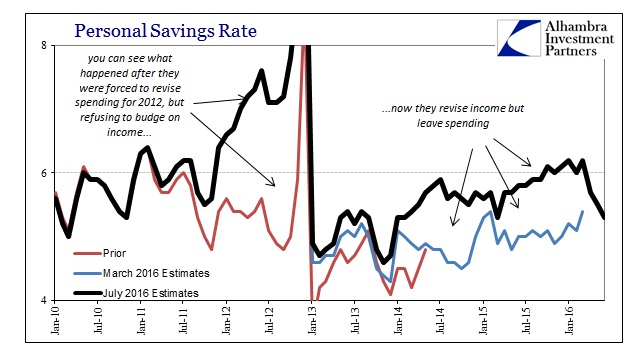

The Personal Savings Rate is a rather important economic indication. Because it is derived from the difference between income and spending, it can tell us a great deal about the state of the economy from the consumer perspective. Unfortunately, nobody can say with any degree of confidence what the savings rate is right now, or even what it has been over the past few years.

Back in March, it was thought that the savings rate for November 2015, a rather important month situated between (so far) both bouts of “global turmoil”, was 4.9% and down slightly from 5.1% in October. The rate was fairly steady throughout 2015, only achieving an upward bend in December last year on into 2016.

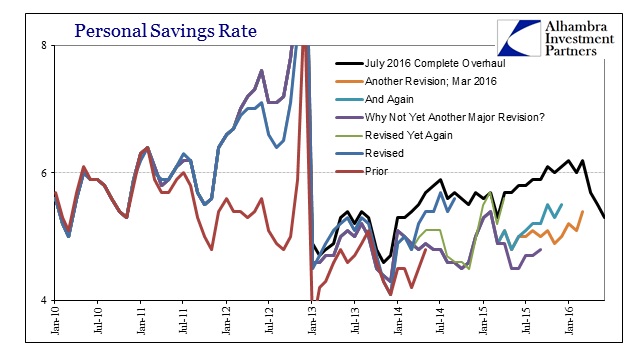

Income and spending figures have since been revised, with incomes, like GDP, especially at the start of 2013 pushed upward. Spending, overall, was revised slightly lower. The combination of those two revisions is to produce a savings rate history that is completely unlike what was believed just a month ago. The figures now suggest that personal savings were 6.0% of income in November 2015, not 4.9%. Further, not only was the savings rate higher it had started rising as far back as late 2014.

These are not small changes but they have become a constant feature. Because of that, there can be no confidence that whatever number is presented today will be left standing even a few months from now. Again, these are rather crucial figures for the Commerce Department to essentially demonstrate that it has very little idea of what they might really be. If this data is subject to so much change then it is at best unreliable.

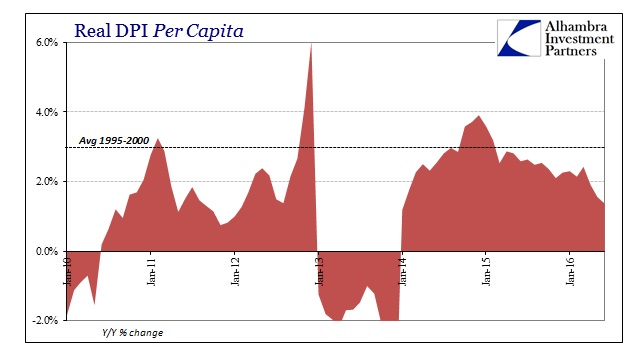

From that view, we have no idea if the dramatic slide in the savings rate is “real” or just further statistical imprecision. The reason for the drop is more so a decline in real income than an increase in real spending.

And those figures are derived from CPI rates that are now somewhat higher than they were a year ago.

In the end, maybe none of this actually matters much because the likely reason for the statistical scattering is what renders it all essentially splitting the hairs of statistics unsuited for this actual environment. The current economy is unlike any other economy, as once again we find more evidence that the Great Recession was not a recession. The revisions are thus shown as inconsequential to the more important big picture. We may not have any idea of what the savings rate is, but we can reasonably assume that in economic terms it is far less important than it once was because it applies to a much smaller proportion of economic participation.

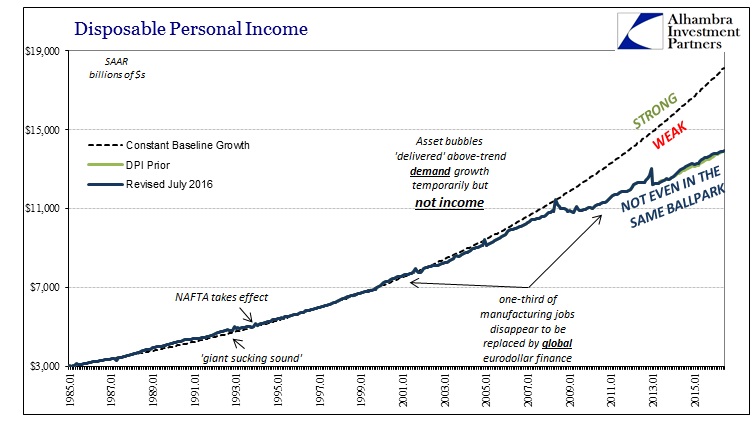

And unlike GDP, the trend in income falls below the historical baseline with the dot-com recession and the true start of Ross Perot’s “giant sucking sound.” This deeper review of income corroborates fully the participation problem which clearly existed before the Great Recession. Therefore, the Great Recession, again as something far different than recession, simply amplified the existing economic weakness into a massive and so far permanent rupture.

We don’t know what the savings rate is in 2016 because the economy of 2016 is and has been altogether different for practically all of the 21st century. Even though on the surface there seems a significant difference between 6% and less than 5%, in reality the only difference that truly matters is the one where Disposable Personal Income in 2016 is somewhere around $14 trillion rather than the $18 trillion it would have been had the Great Recession actually been a recession.

Stay In Touch