On June 6, Janet Yellen spoke to the World Affairs Council of Philadelphia in what were highly scrutinized comments. The occasion was just a weekend in between the May payroll report that clearly unnerved her and the rest of the FOMC. Prior to that BLS publication, it was believed that a rate hike in June was all but set. Afterward, as Yellen’s speech appeared to confirm, it was a complete turnaround.

The Fed Chairman emphasized four important uncertainties facing the US economy in 2016, both immediate and long-term. The first was domestic demand, primarily consumer spending which she and other economists continue to suggest is and has been strong despite all evidence to the contrary. Second, Yellen contended more about “global turmoil”, the easy excuse that it is all the fault of overseas idiosyncrasies, especially China being China. Her fourth point was inflation where she essentially punted; she still expects it to move up to the 2% target but she also acknowledged that inherent imprecision might make the actual track of consumer prices “significantly different” (translation: we don’t really know).

Over the long run, it was her third point that is perhaps most crucial: productivity. Unsurprisingly, Yellen expressed optimism on the subject (when does she ever not?), particularly as she believes the depth of the Great Recession itself was partially responsible for yielding almost no productivity growth these past seven years (though no thoughts on why seven years weren’t yet long enough). As the economy gets stronger, in her view, investment (she didn’t specify, but I highly doubt she means even greater financial investment), R&D, and entrepreneurialism should all return more toward historical trends. This will allow wages to rise and foster higher sustained economic advance.

Over time, productivity growth is the key determinant of improvements in living standards, supporting higher pay for workers without increased costs for employers. Recent weak productivity growth likely helps account for the disappointing pace of wage gains during this economic expansion. Therefore, understanding whether, and by how much, productivity growth will pick up is a crucial part of the economic outlook.

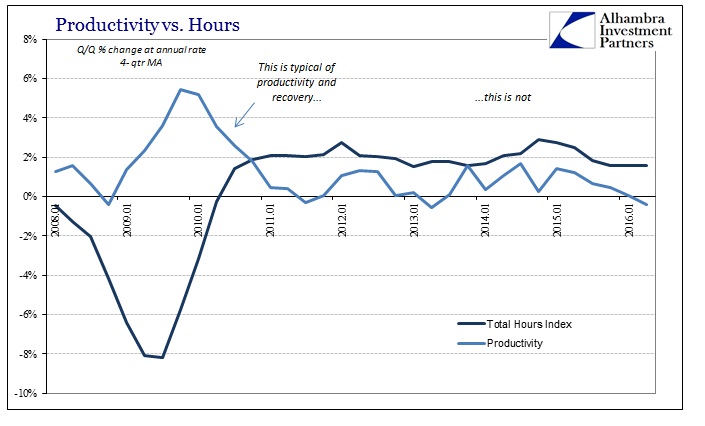

We aren’t talking about one or two or even three years, here, productivity has been weak throughout the whole “recovery” and indeed began to decelerate at the tail end of the housing bubble. In other words, is productivity weak because of the economy, or is the economy persistently weak because of productivity? The last two Fed Chairmen have been talking about the economy picking up for years on end, perhaps businesses active in America just don’t buy it?

It’s an odd occurrence either way it can be spun, certainly in light of the “best jobs market in decades.” From the point of view of the labor statistics, the economy is robust and has been for two years. Why wouldn’t these businesses that have purportedly been hiring at such a fast pace not likewise and concurrently invest in themselves beside raw labor? If the economy is so strong that they would need such a sustained pickup in labor utilization, then that alone should have fulfilled Yellen’s requirement. That means either business itself is fundamentally different in the 2010’s or the economy as viewed by the labor market isn’t nearly so strong.

Mainstream association of “strong” consumers aside, there is very little evidence that the labor market is indicative of the economy as a whole. Manufacturing here and around the world has started into its third year of sustained contraction, hardly arguing for the same economy as measured in BLS statistics. Despite even more robust payroll gains at the end of 2015, there was widespread and growing fear that recession was perhaps imminent to start this year. In short, the labor market economy is of its own world uncorroborated by anything else.

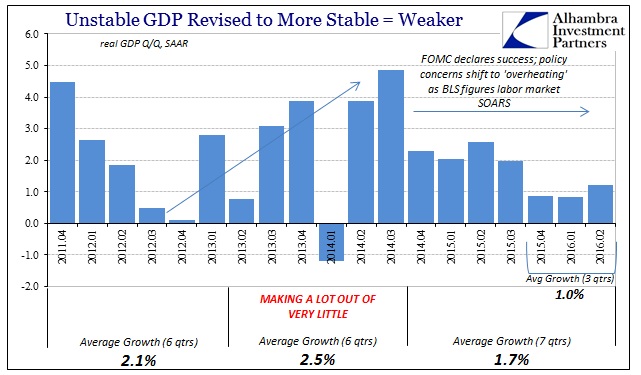

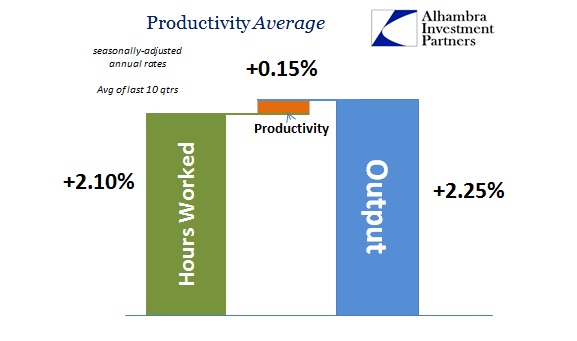

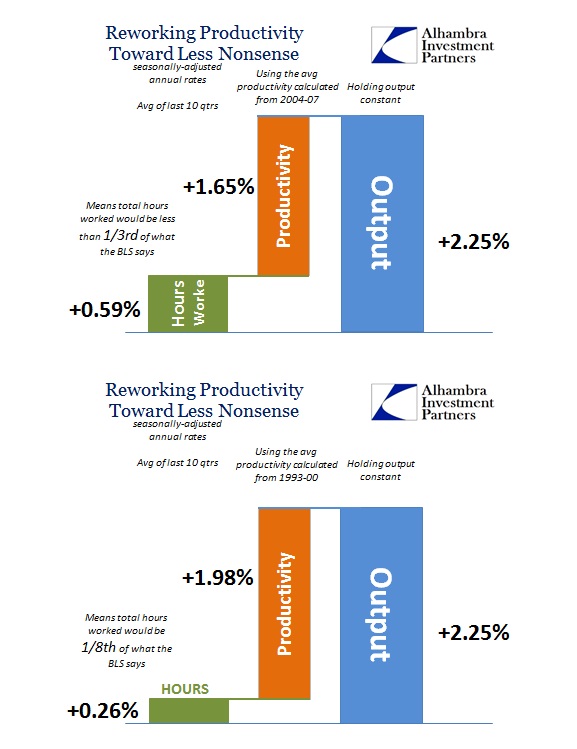

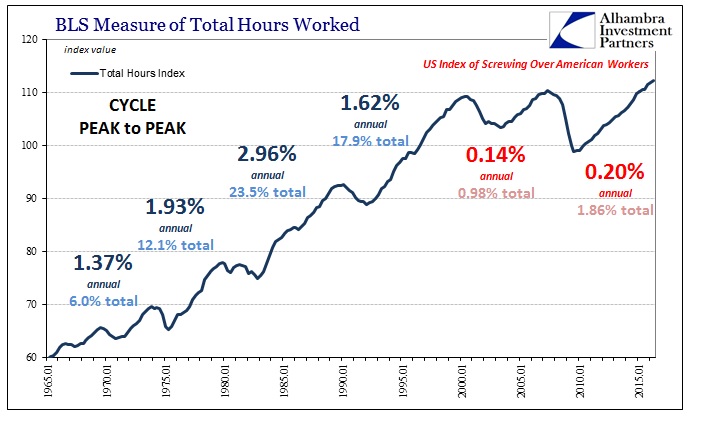

That includes GDP, which despite grand policymaker assurances in late 2014 has instead slowed and then slowed again. Over the last three quarters through Q2 2016, GDP has gained a little less than 1%. Despite such paltry economy that spans nearly a year, the BLS continues to suggest large gains in labor. Total hours worked grew by 2.13% on average in those three quarters. That rate of expansion was more than a quarter better than what was averaged in the recovery from the dot-com recession (2004 to 2007) and only 10% less than what was estimated for the 1990’s (1993 to 2000).

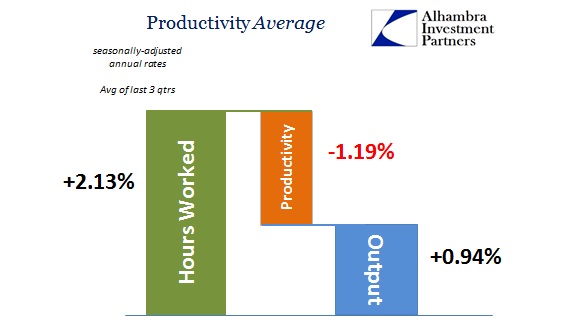

As a result of this large discrepancy, productivity is forced to be highly negative. If hours worked gain 2.13% per quarter but private output was just 0.94%, then productivity as the plug in between them must have been -1.19%. The last time productivity was so bad was 1979 at the worst of the Great Inflation, indicating the start of what would be nearly three years of on and off recession, the second of which was the worst of the postwar period until 2008.

The longest stretch of productivity declines since the end of the 1970s is threatening to restrain U.S. worker pay and broader economic growth in the years ahead…

It was the third consecutive quarter of falling productivity, the longest streak since 1979. Productivity in the second quarter was down 0.4% from a year earlier, the first annual decline in three years and just the sixth year-over-year drop recorded since 1982.

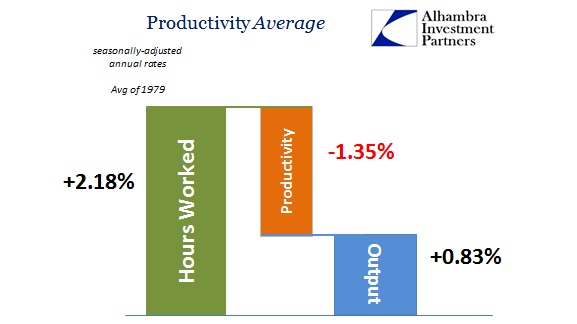

There is simply no way this adds up to a “stronger” economy just over the calendar horizon. The statistics from 1979 are alarmingly familiar: average total hours increased an average of +2.18% while total private output was just +0.83%, meaning productivity was sharply negative at -1.35%.

The similarity of outward appearance is extraordinary, and by that count alone it suggests the opposite of what Yellen was thinking in terms of the strong economy to come. The reason for that is exceedingly simple – businesses don’t hire where they don’t get a lot of additional output from their employees. That is capitalism; the synergistic combination of labor and capital such that together they produce more than either alone. So if businesses have hired a lot and received less in output, roughly speaking, than they hired, there is grave danger that the large increase in headcount will reverse and trigger a decrease.

And it is the inverse condition that actually leads to the recovery economy that Yellen keeps alluding to. In other words, where low productivity yields recession, high productivity ends it; once businesses have laid off enough workers such that output per worker (a lot) more than equalizes, the end of the downturn in employment and really economy is at hand.

So Yellen’s narrative is in trouble on both ends; either productivity figures are somewhat accurate, meaning that nearly a year of negative productivity suggests, in general outline, like 1979 and meaningful downturn, or that productivity has been artificially suppressed by the BLS overstating labor gains, and thus the economy of the past few years really has been as bad as the “manufacturing recession” indicates. Neither of those scenarios leads to the storybook ending economists always describe, which itself is indicative of same (if they have to keep telling the same story year after year, it’s not a very good or dependable story). Either the economy is like 1979, or it was never a recovery to begin with.

Productivity has been near-zero for years, which is a reflection of this depression (meaning different from recession, a more-than-temporary deviation in economy). No matter how you normalize the figures in either direction, it all adds up to only that. If productivity is correct as it has been estimated at such low levels, then, as Yellen said back in June, that was certainly a “key determinant” of the lack of “improvements in living standards” and stagnated worker pay. If, on the other hand, the BLS has been instead overstating labor, then there still isn’t enough gain in output to work out something close to normal. In other words, productivity would still be significantly lower just not zero, but that would also mean a lot less jobs especially since the middle of 2014.

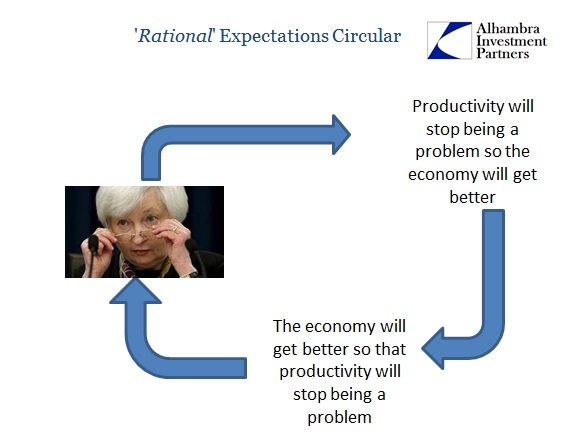

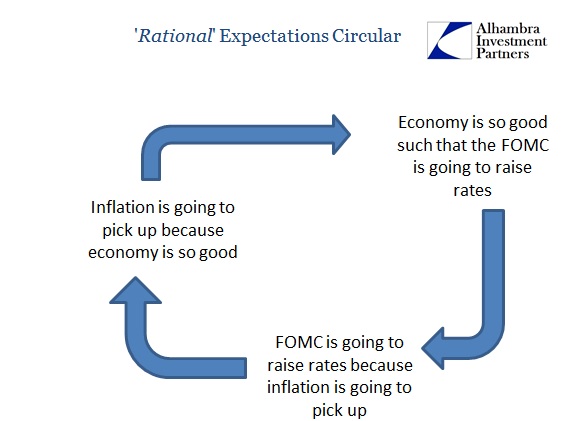

Yellen’s economic formulation, then, the one that dominates the mainstream, is the circular logic of the economy that “should be.” We don’t need to worry about all this messiness and ahistorical weakness since the economy will get better because, as she says, it will get better. That is entirely backward and accounts for her and her colleagues’ continued state of befuddlement. This discrepancy and disaster in the statistics tells us instead that there is something very wrong with the economy and even if we don’t know which way that means specifically it isn’t likely at all to get better; and a great deal that suggests it will only continue in this state.

The shorter version is simply her claim that though she’s been wrong year after year after year she isn’t now so we can just ignore the mess in all the numbers as if mindless mean reversion were itself an economic force. The reality is far simpler; the mess in the numbers shows why she, like Bernanke before her, has been wrong year after year after year and will continue to be.

Stay In Touch