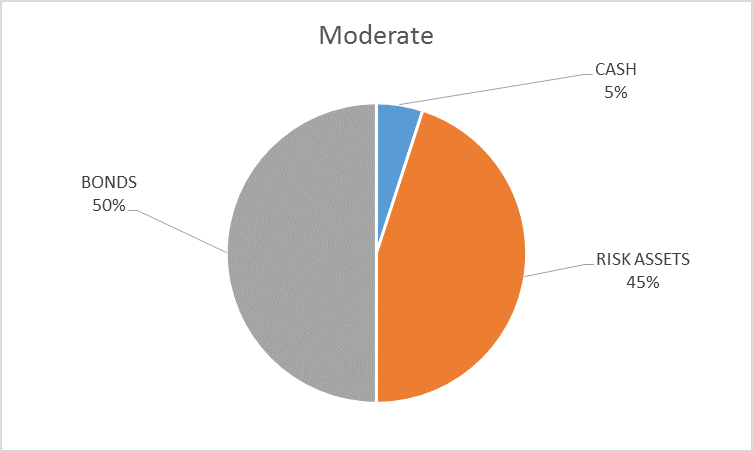

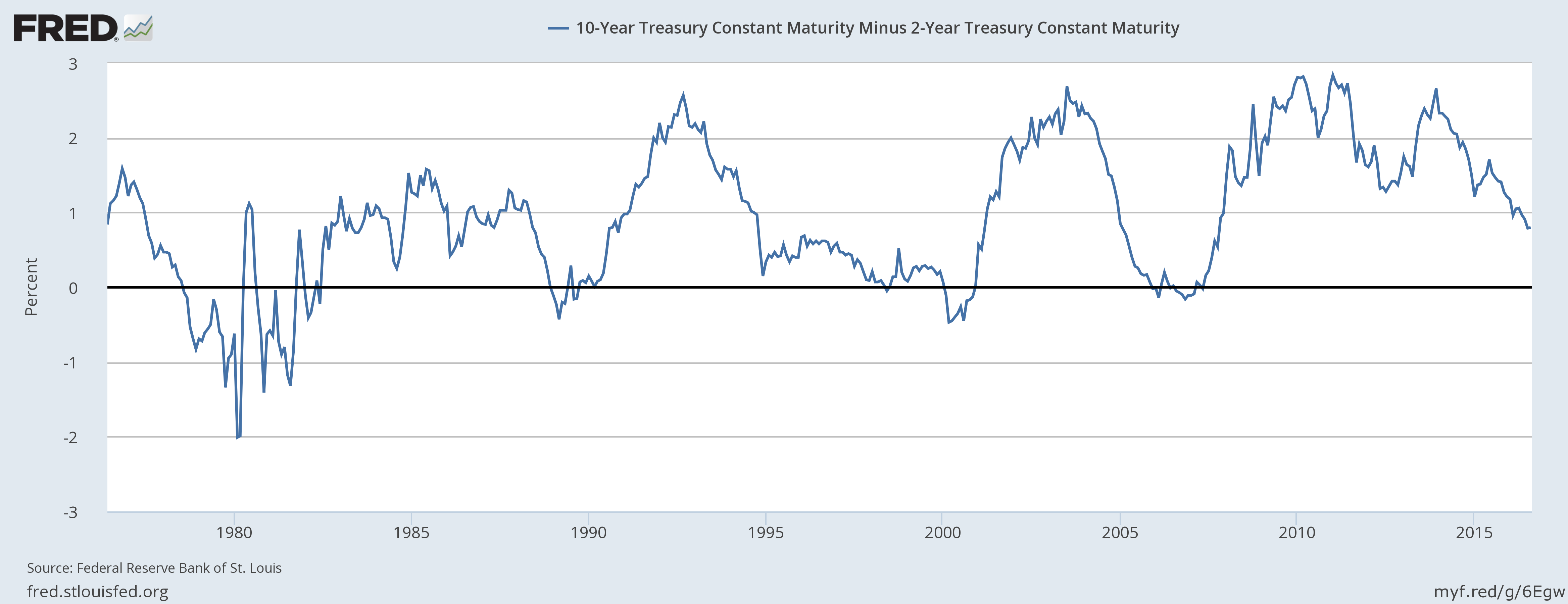

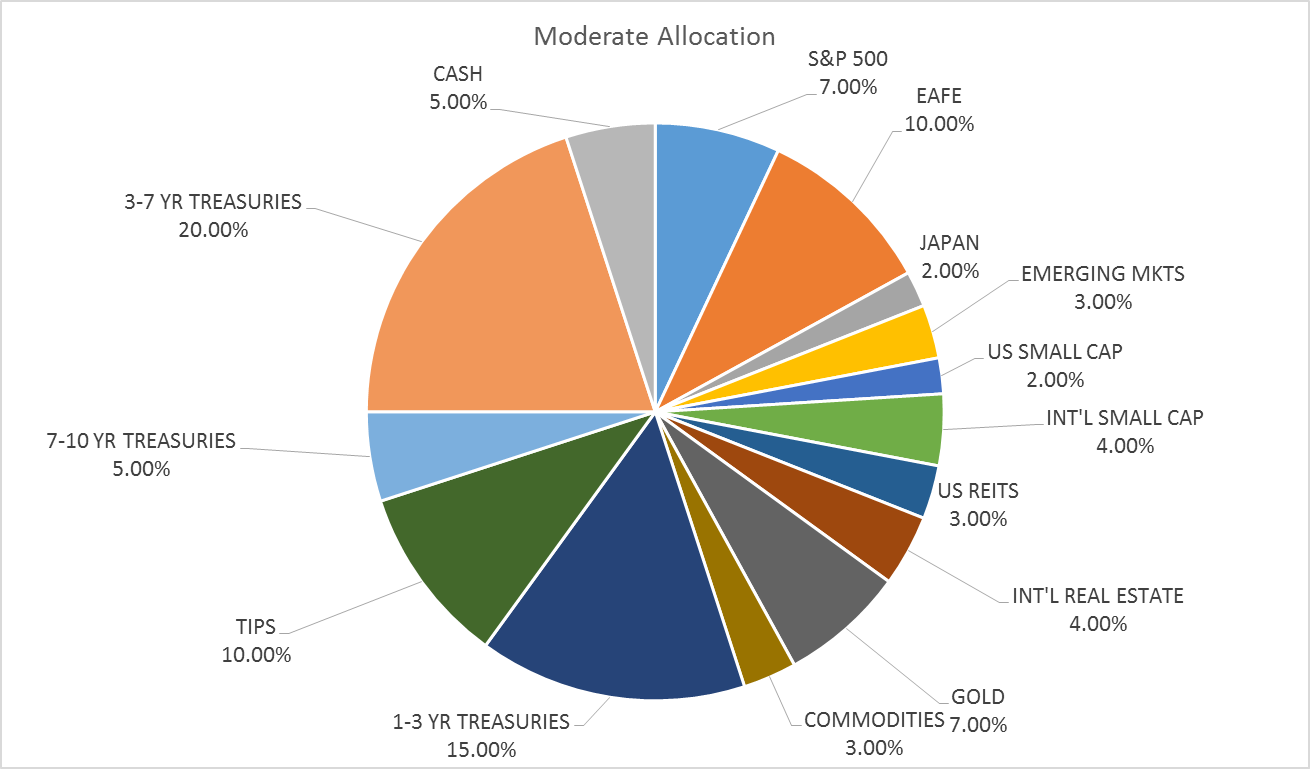

The risk budget is unchanged this month although the composition of the portfolio does change. For the moderate risk investor, the allocation between bonds, risk assets and cash remains at 50/45/5. There are changes to the allocation but the overall risk budget stays the same. Credit spreads did continue to narrow this month but other indicators did not confirm the move. The yield curve flattened and valuations rose as earnings fell. Momentum for major stock averages is waning short term and the US dollar has weakened since the last update.

The changes to the allocation this month are mostly predicated on shifting momentum. Stocks, despite making new highs, do not exhibit a high degree of conviction; there has been no followthrough since breaking out to new highs. While the incoming economic data has improved somewhat – better than expected is not necessarily better – our market based indicators have responded very tepidly. It does not appear the market is buying the renewed growth scenario. One has to wonder if the feeble Q2 rebound – compared to the previous two years experience – hasn’t takes some of the wind out of the sails of the second half rebound crowd.

Indicator Review

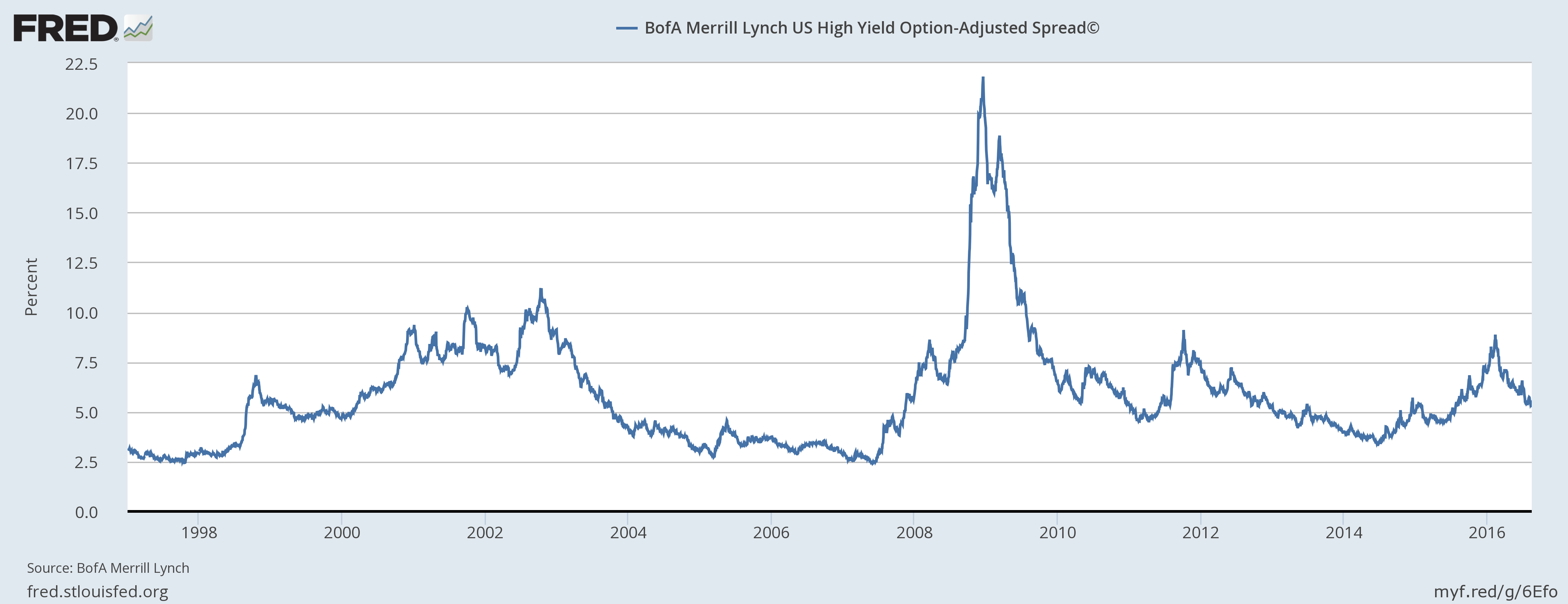

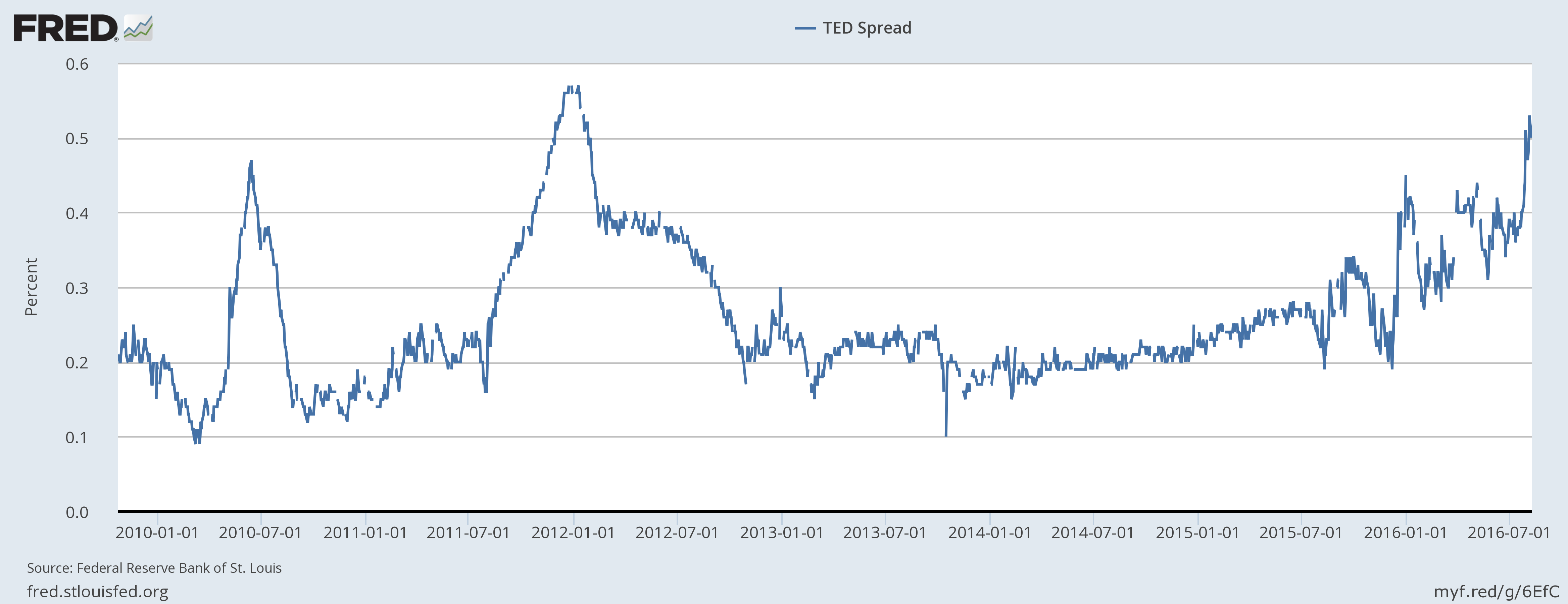

- Credit Spreads: HY credit spreads continued to narrow over the last month and are now narrower year over year. That is not generally a situation associated with stress. Spreads are, however, still higher than the lows for this cycle (6/23/14 @ 3.35%) and well above the lows seen in the last cycle (5/25/07 @ 2.45%). There is, however, the matter of the TED spread which has been moving wider recently as LIBOR has recently spiked. There is general agreement that the move is a function solely of regulatory changes in the money markets and uniform consensus of any kind makes me nervous. Rather than say, “It’s different this time” and hope to be proved right, I think it more prudent to say, “It’s not different this time” and hope to be proved wrong.

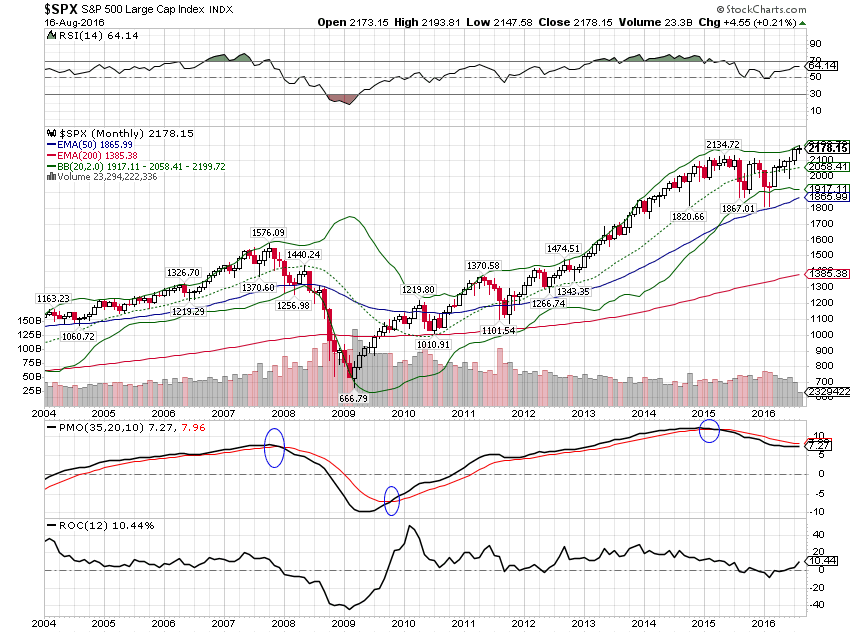

- Valuations: As Q2 earnings season winds down, the consensus is that this quarter marked the bottom of the earnings recession. Earnings did beat estimates – that should shock exactly no one anymore – but the revenue beat rate was below par. Overall earnings for the S&P 500 look to be down 2.5 to 3% when all is said and done for the quarter. That is less than last quarter’s contraction and so the downtrend has moderated. Estimates for next quarter are for flat and then an 8% surge in Q4. There doesn’t seem to be any fundamental explanation for that expectation other than an extrapolation of the current trend. The bottom line is that the bottom line is still contracting and multiples are still expanding. Where she stops nobody knows….

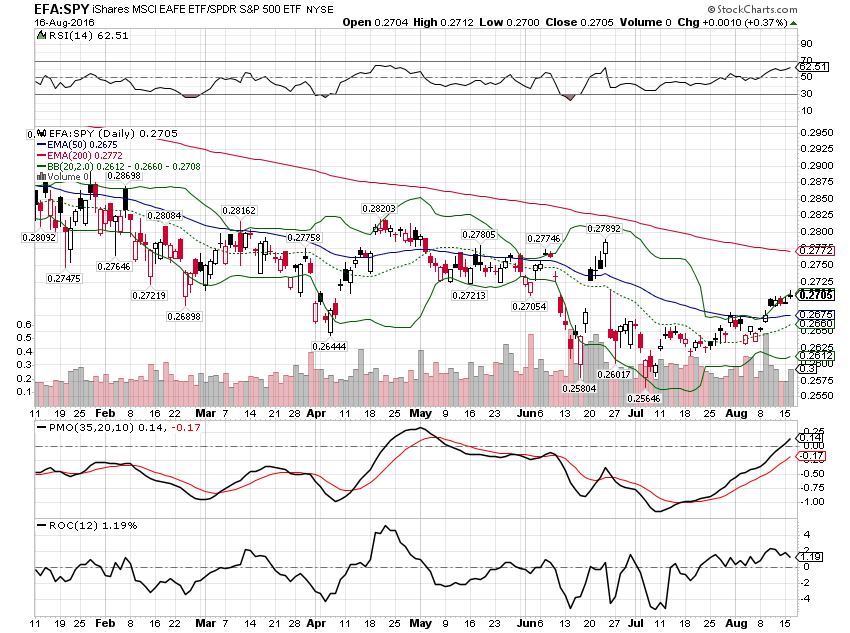

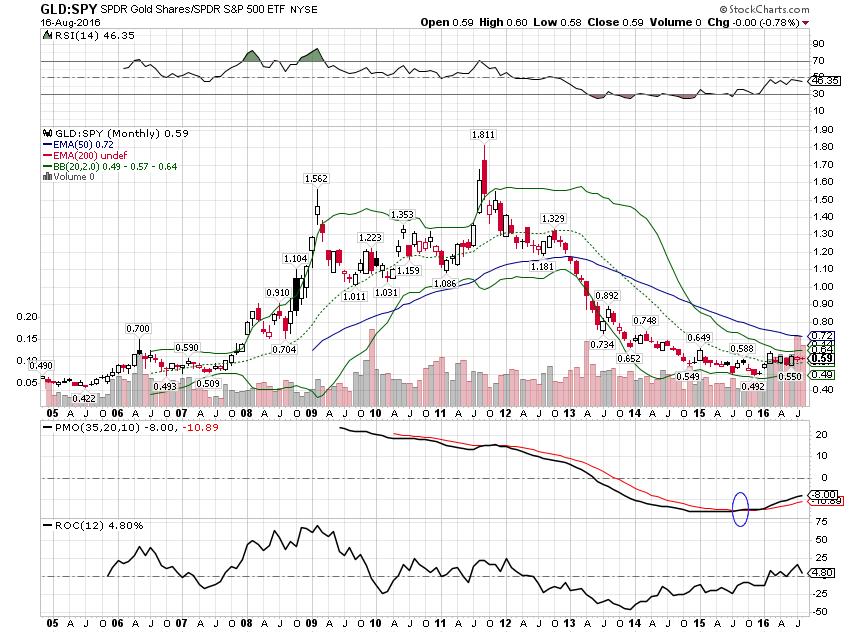

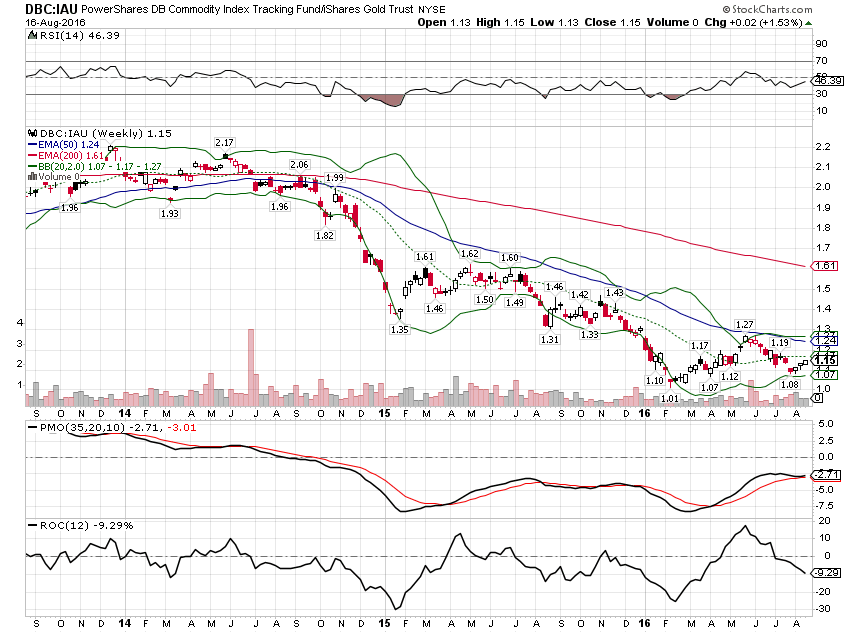

- Momentum: Momentum continues to drift away from US stocks. Relative performance trends continue to favor gold and bonds over US stocks. Foreign stocks, developed and EM, have also recently started to outperform the US again. For EFA, intermediate and short term momentum indicators are positive. For EM we also have a positive long term momentum buy signal versus the S&P 500. Momentum has also shifted in favor of the general commodity ETF (DBC) versus the S&P 500 on all time scales. DBC is also outperforming gold in the short and intermediate term. I suspect we are in for a period of catch up in general commodities versus gold. The outperformance of commodities is at least somewhat confirmed by the loss of upside momentum in long term bonds.

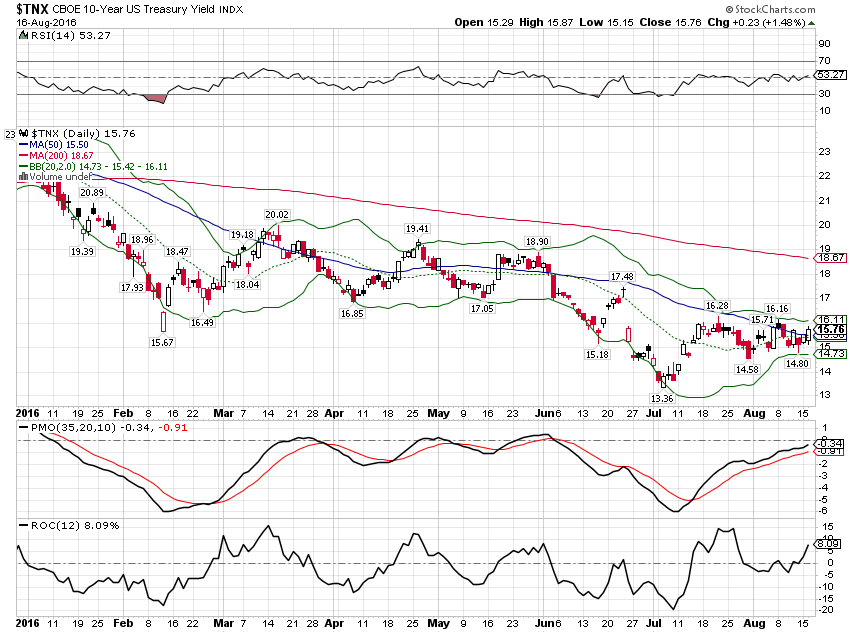

- Yield curve: The 10/2 spread flattened very slightly (4 basis points) over the last month but I think the real news here is that the flattening momentum seems to have waned. The rate at which the curve is flattening has stalled. Whether that is a good sign or bad is almost impossible to tell yet but based on the action in currency markets I would guess it is a sign that the market has no fear of a Fed rate hike – probably for good reason. As I’ve noted in the past, while everyone knows the yield curve flattens or inverts prior to recession, the more important observation is that the curve shows a rapid steepening right before the onset of recession. It may be that with short rates so low we never get to inverted but we may well see the steepening if the market starts to anticipate further Fed action.

Credit Spreads

HY spreads remain elevated but are now narrower year over year.

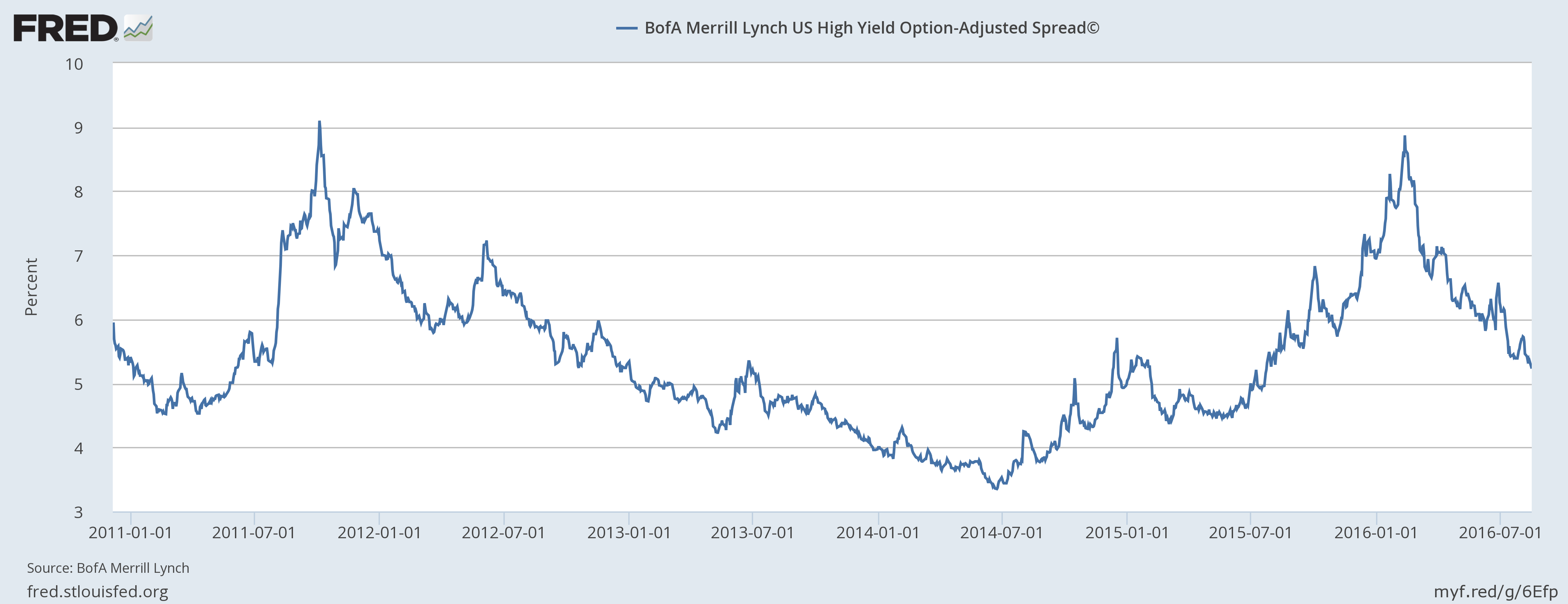

Shorter term view shows recent narrowing of spreads better.

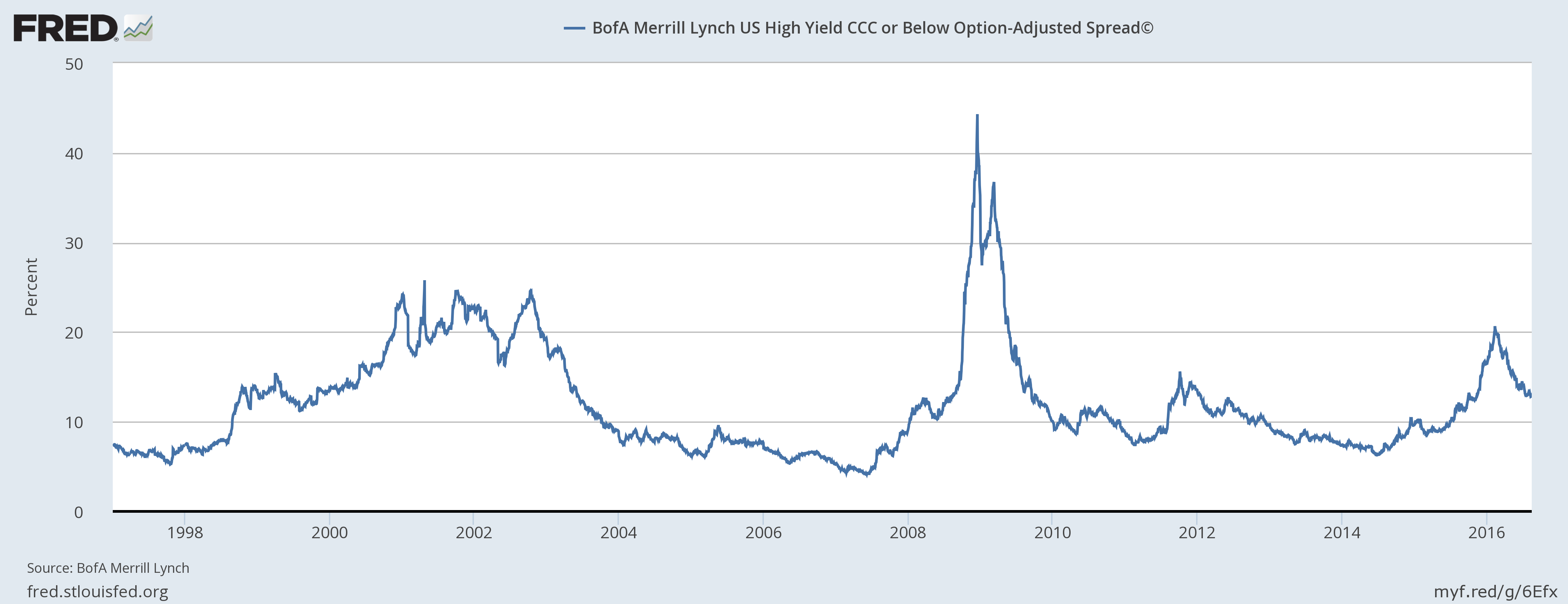

The narrowing has taken place across the credit curve. Even CCC bonds are no longer showing much stress. The appetite for yield is pretty amazing.

One area of concern is the TED spread which has recently widened as LIBOR has risen. It isn’t anywhere near levels associated with recession but it is moving in the wrong direction. Most everyone is dismissing this as a result of regulatory reform in money markets but if you have a loan geared to LIBOR what difference does it make why LIBOR went up? Your loan is still going to cost more. Call it regulatory tightening if it makes you feel better but it is a tightening. It isn’t much and the impact may be minor but it isn’t zero and it shouldn’t be ignored.

Yield Curve/Bonds

The yield curve continues to flatten but has stalled more recently. Prelude to a steepening based on more Fed action? Is the economy really that bad? Seems unlikely based on recent data but then the same could be said a few months before almost any recession.

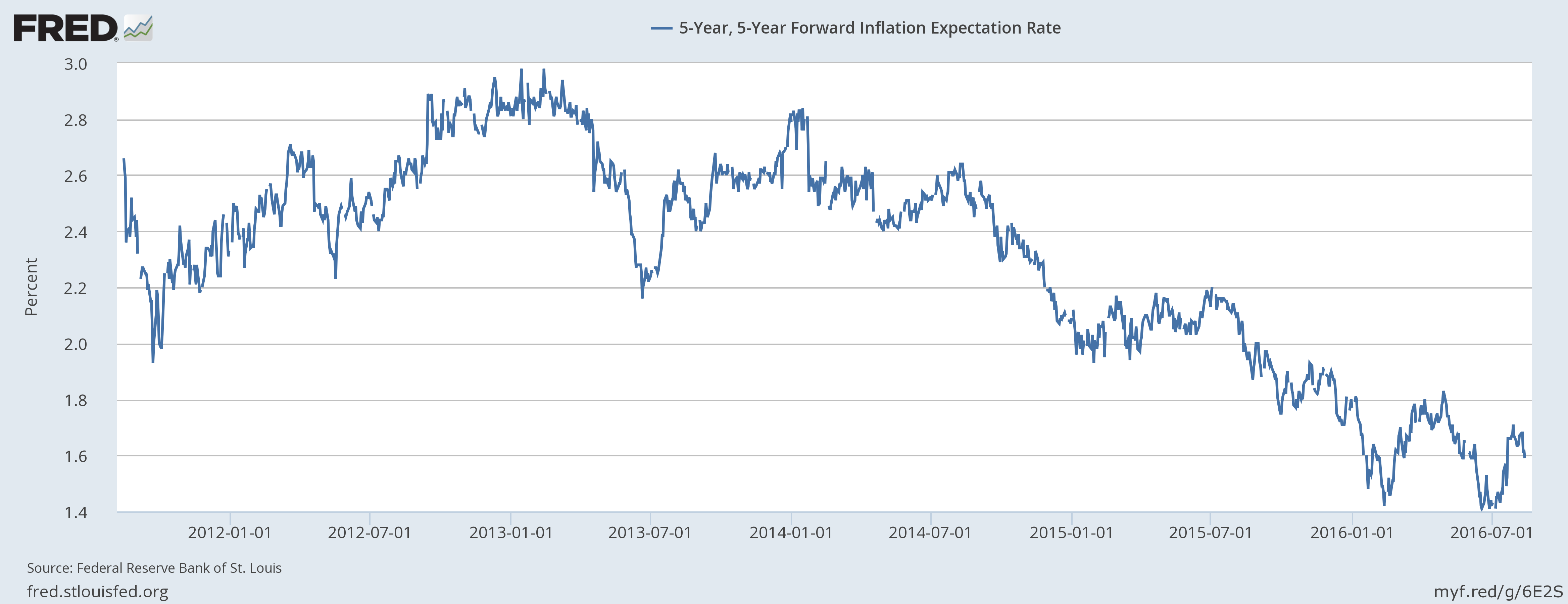

Inflation expectations barely budged.

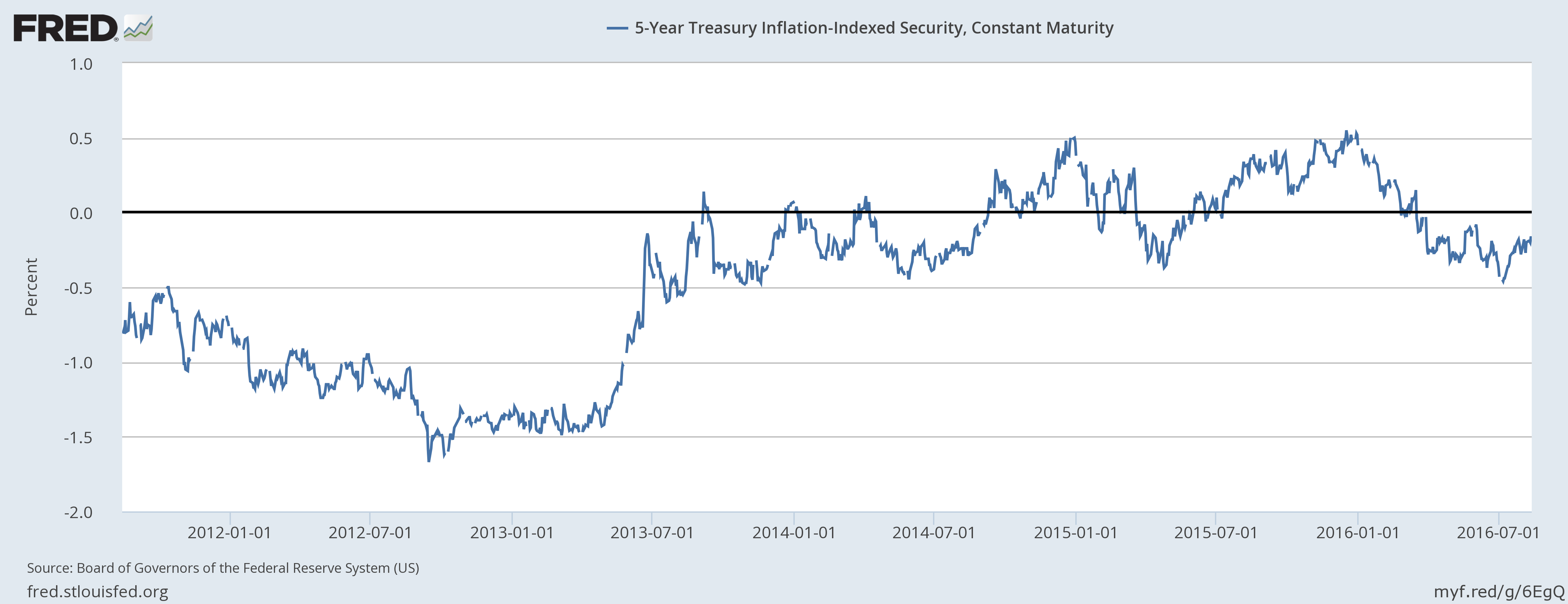

Real interest rates moved up 17 basis points over the last month, a slight – very slight – improvement in real growth expectations.

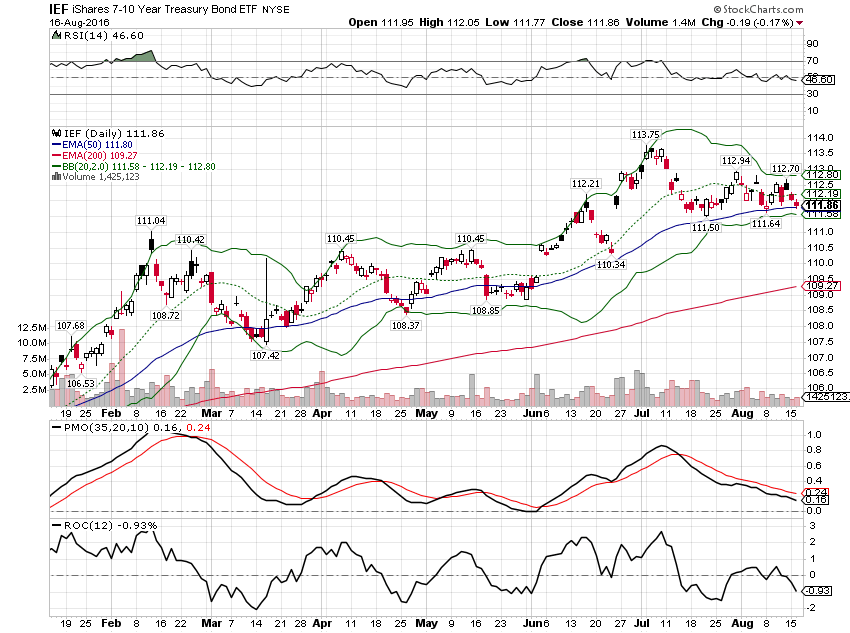

10 year Treasury yields are still near the lows of this cycle but downside momentum is waning and a corrective rally in rates is due.

Overall, there hasn’t been much change in growth and inflation expectations as expressed through the bond markets. There has been a very slight uptick in real growth expectations and nominal 10 year rates do seem poised for a corrective rally. Could it be the actual end of the multi-decade bond bull market? Have rates seen their lows? Well, of course anything is possible but I must admit I have my doubts. We will eventually have another recession and when we do I see no reason to expect anything but another bond market rally. For now though I think it wise to shift with the short term trend and shorten up duration again as we did last month. More on that below.

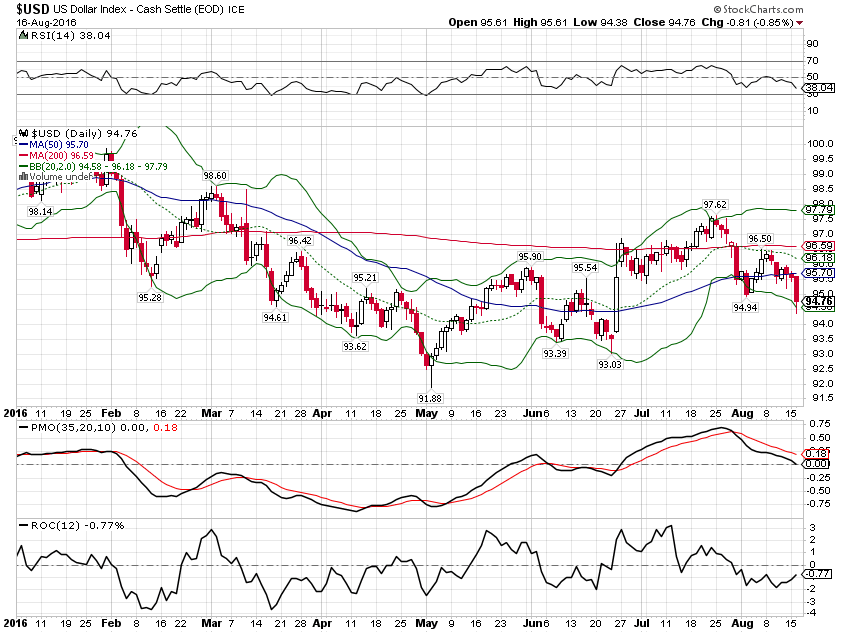

Those negative real rates continue to weigh on the dollar which is rapidly approaching pre-Brexit levels. With both short and long term momentum now negative on the dollar index, I expect further downside. That should continue to be supportive of commodity prices.

Valuations

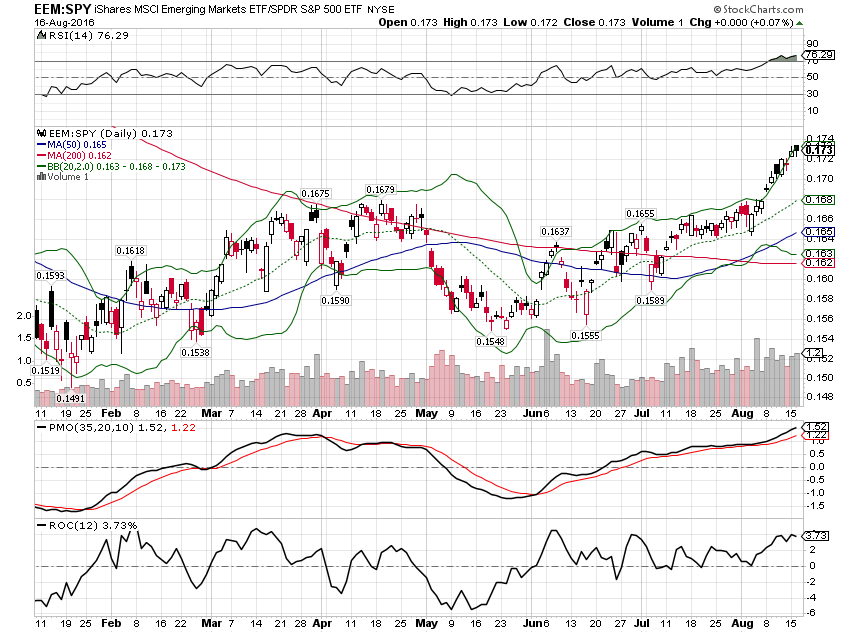

As I said above, the S&P 500 is just getting more expensive as earnings fall and stock prices continue to rise. It isn’t a big change though as the market as a whole just really hasn’t moved that much. Nevertheless, every valuation technique I know of that has any relation to future returns says stocks are fairly dear compared to history. How dear depends on your methodology but I don’t know of any valuation technique that sees US stocks as cheap right now. Emerging markets continue to be the cheap part of the equity world and they now have momentum relative to the US and the tailwind of a weakening dollar – as long as it doesn’t get too cheap, too fast.

Momentum

The S&P 500 has barely budged so far in August and long term momentum is still negative. Short term momentum has waned as well and is now offering a fresh sell signal. The complete lack of volatility so far this summer is actually quite eerie. It is said that one shouldn’t short a dull market but this might be the time that old adage doesn’t hold up.

EFA has been outperforming the S&P since early July but that was just correcting an oversold condition. Will it have legs? As I’ve said many times, it is very difficult for international stocks to outperform for any length of time unless the dollar is falling too. From a valuation standpoint EFA is much cheaper than SPY so one can justify an overweight but for this to really move, we’ll probably need to see the dollar fall out of the bottom if its recent range.

Long term momentum continues to favor gold over stocks. This trend has been struggling a bit lately but is still intact.

Short and intermediate term momentum now favors a general commodity ETF (DBC) over gold.

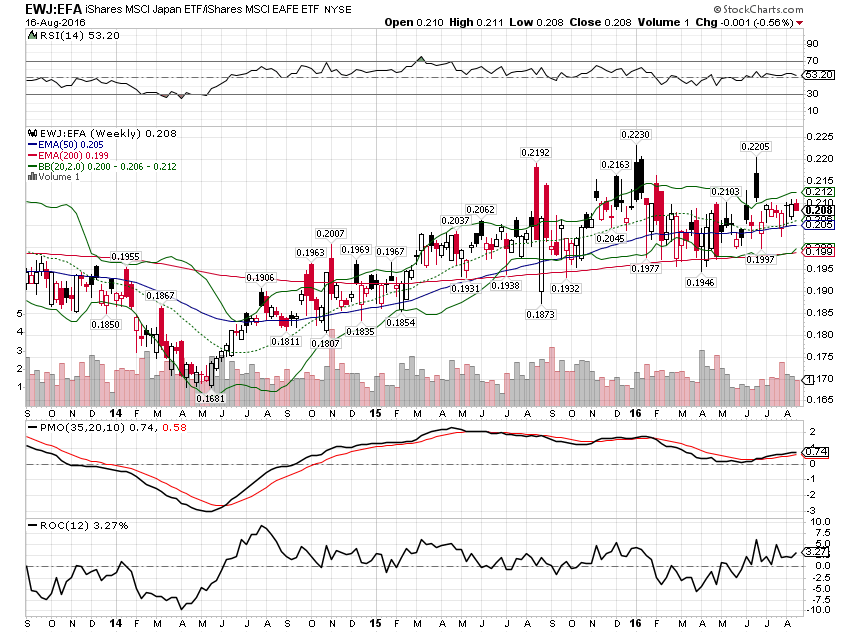

Japan continues to outperform EFA as a strong Yen aids returns.

Short and intermediate term momentum has turned down for the 7-10 year Treasury ETF. With a weak dollar also in place I think that makes sense and caution on duration is warranted.

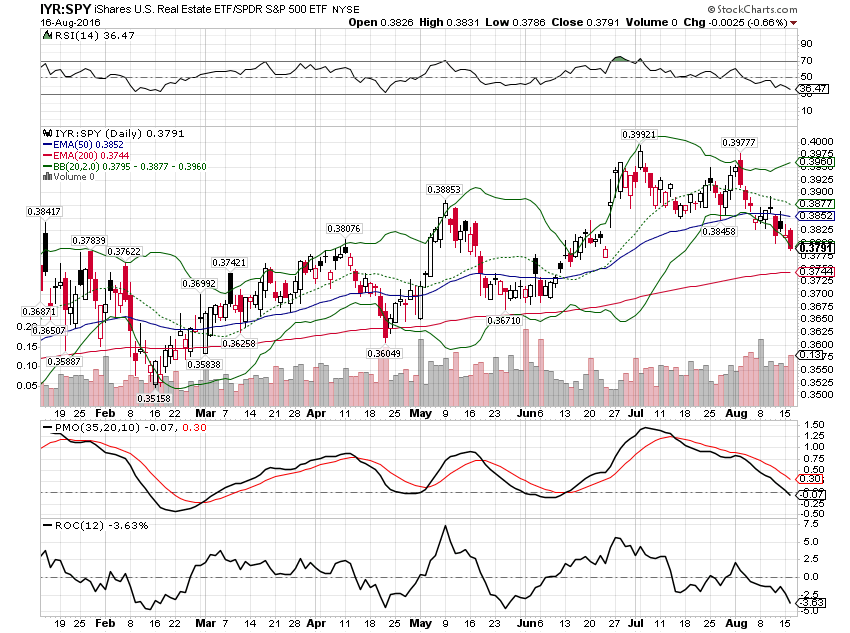

As bonds have lost momentum so have REITs, relative to the market.

Portfolio Changes

I am making some changes this month mostly based on the momentum shifts we’ve recently observed. Here are the changes:

- Reduce the SPY allocation by 2%

- Reduce IYR allocation by 1%

- Add a 3% allocation to DBC, raising overall commodity allocation to 10%.

This is not a big change but if these trends continue they could be important and early. Markets are pointing toward dollar weakness and all that entails. Assuming it doesn’t mean recession – at least not yet – the implications would be higher commodity prices, higher interest rates and outperformance by foreign stock markets. Currency trends have in the past been persistent but in the era of currency wars I’m not sure that holds.

Here’s the moderate allocation as it stands after the changes:

FOR INFORMATION ABOUT OTHER RISK BASED ASSET ALLOCATIONS OR ANY OF OUR OTHER TACTICAL MODELS, PLEASE CONTACT JOE CALHOUN AT JYC3@ALHAMBRAPARTNERS.COM OR 786-249-3773. YOU CAN ALSO BOOK AN APPOINTMENT USING OUR CONTACT FORM.

CLICK HERE TO SIGN UP FOR OUR FREE WEEKLY E-NEWSLETTER.

“Wealth preservation and accumulation through thoughtful investing.”

This material has been distributed for informational purposes only. It is the opinion of the author and should not be considered as investment advice or a recommendation of any particular security, strategy, or investment product. Investments involve risk and you can lose money. Past investing and economic performance is not indicative of future performance. Alhambra Investment Partners, LLC expressly disclaims all liability in respect to actions taken based on all of the information in this writing. If an investor does not understand the risks associated with certain securities, he/she should seek the advice of an independent adviser.

Stay In Touch