There is absolutely no need whatsoever to pay any attention to what Janet Yellen says. There is even less call for parsing the increasingly ridiculous FOMC statement, particularly with regard to inflation where it will continue to suggest “professional forecasters” are the only way (left) to measure monetary policy effectiveness. Instead, four times a year the FOMC meeting coincides with the release of the Federal Reserve’s modeled forecasts. These are, of course, useless as projections and thus serve an entirely different purpose.

Because Janet Yellen will never, ever say the words “monetary policy doesn’t work” or “QE has unthinkably failed even in the most basic sense” we are left to examine her math which has done it for her. Though at some point it should be required (in the sense of reckoning and accountability ahead of reform), for now there really is no need for her to explicitly state what pretty much anyone outside the media and economics profession already knows. The quarterly staff figures just further confirm all suspicion.

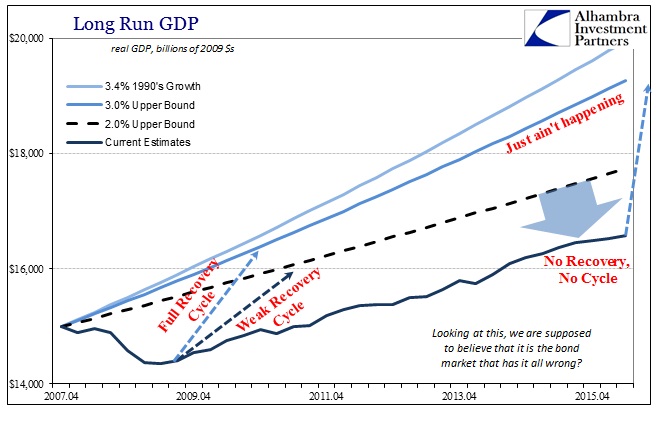

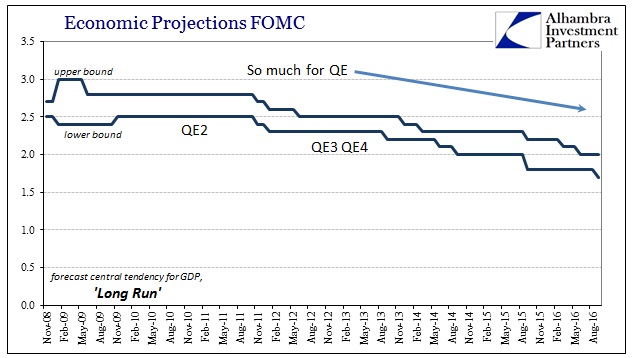

It really starts with the modeled projections about long run growth which stands in for economic “potential.” As noted on several occasions, the last at the end of August, the CBO has along with the Fed agreed in its modeled projections showing a drastic reduction in “potential.” While economists take these numbers to suggest there is something wrong with the economy, in reality what they prove is that again monetary policy just doesn’t work. I wrote then:

That is why the Fed has to mark down long run potential because not doing so would mean that at some point in the near future the economy is going to have to explode higher to bring up the average of this “cycle.” And the longer the economy persists in this mysterious “low growth trap” the greater that eventual “liftoff” will have to be to get back to the normal long run tendency. Instead, economists have reduced economic potential because nobody believes any such thing will occur, not even them. Thus, they now have to come up with reasons that preserve their worldview while also accounting for the world – an increasingly impossible task. Even now the much-reduced long run tendency remains quite far out of reach, dampening enthusiasm all over again academically for both the timing and intensity of that anticipated “liftoff.”

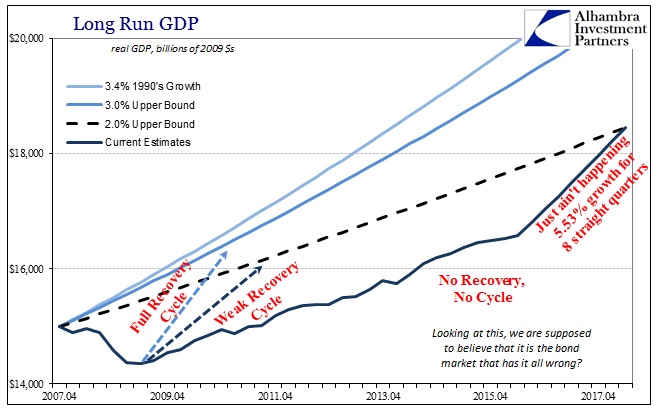

The long run “tendency” is exactly that, meaning that it measures growth across a full economic cycle including its recessionary part. Thus, the current “cycle”, which economists still outwardly believe is the operative condition, has to include both the Great Recession’s decline and also the unusually slow recovery thereafter (and thereafter and still thereafter). Just to get back to a greater than 2% long run average or central tendency will require at this point sustained 5% growth or better for several years. To, for example, normalize GDP at the 2% upper bound for the long run tendency by Q2 2018, two years forward, would require 5.53% growth in all eight quarters between now and then – it’s just not going to happen.

When the figures were updated for June, the FOMC reduced the upper bound for long run growth to 2%; in the new estimates for September, the lower bound was cut to just 1.7%.

Again, economists see this as some mystery of demographics or non-specific productivity problems in the economy itself; it is instead more proof in the language of economists that the Great Recession wasn’t ever a recession and policymakers have no idea what they are doing. And that starts with money itself.

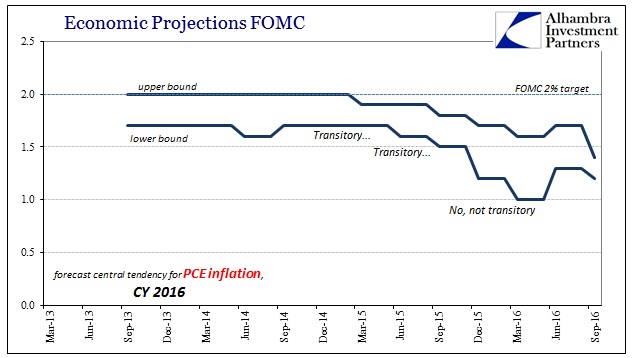

In more specific formulations, that means inflation. You would think after so much trillions in “money printing” there would be an obvious correlation, or at worst a detectible real economic response to what was advertised as enormous and quantitatively determined balance sheet expansion. That is where the word “transitory” originates; it is the orthodox response to this demonstrable failure. To Yellen and the FOMC, balance sheet expansion surely works, it’s just that its success is being delayed by other “unrelated” factors. While that remains the public determination of the FOMC (the continued use of the word “transitory” right in their official statements) the models are increasingly adapting to a different reality.

There are several key developments related by the trend in this year’s expected inflation. The first is what recounts that forecast for “transitory”, meaning that the math did actually model out to a temporary effect from the oil price crash and growing (global) economic insufficiency. Even though expectations for 2015 were eventually and sharply curtailed in December 2014 (the central tendency range for the deflator in 2015 was reduced from 1.5% – 1.7% to 1.0% – 1.6%) it wasn’t until November last year that 2016 forecasts finally recognized that the meaning of the word “transitory” would have to be stretched into nonsense.

The second important piece in that history is that the Fed actually raised its forecast in June, only to cut it back again in this current update. In other words, the math was encouraged by what was suspected to be a durable rebound from the atrocious conditions at the start of the year only to find that now maybe such optimism was, as always, premature. While the lower bound is back to where it was before the March update, the upper bound “central tendency” for the PCE Deflator is at a new low – right near where the deflator itself remains for going on a third year.

As for near-term economic growth, GDP estimates for this year were again trimmed with a new forecast for more of the same economic stagnation. Despite all the proclamations especially related to the labor market and unemployment rate, the economy at least as measured by GDP (which is the most charitable method available) is forecast to be considerably slower than even last year. Even the projections for next year, which were already (dangerously) low to begin with, are for now “anchored” around the (dangerously) pathetic 1.8% – 2.0% long run “tendency.”

This was not supposed to happen, as the economy was thought to be long before now heading toward at least some appreciable acceleration. That it won’t for yet another year can only mean the increased likelihood that it never will (i.e., the Great Recession wasn’t a recession). The lack of inflation coincident to “never will” completes the monetary picture, including everything relating why “stimulus” isn’t.

Going all the way back to late 2014, this was the central point of contention – a contest between economists with the stock market on their side against the bond market and an appreciation for actual money as opposed to 1950’s monetary theory. Despite the fact that policymakers and economists (redundant) were adamant that the economy was about to take off, the possibility was undercut by their own math even at that time. I wrote in late November 2014:

As I mentioned yesterday, this is another area which likely explains the position of credit and funding (yield curve, tight “dollar”) in direct opposition to stocks. The former has engaged in “secular stagnation” without need to define the exact cause, while the latter only “hears” recovery from the FOMC without the hidden downgrades because it provides convenient if plainly incomplete rationalization for price behavior. The problem of such insufficiency is that there will come a time when only a real recovery will be enough to withstand so much sustained attrition; which is what this all really gets at even if misguided by the adherence to rigid orthodox tendencies and the math it takes for them to see it.

The economic math has been forced by actual conditions over the past two years to “see it.” Economists are themselves talking about it if only internally at the moment, but they, too, are finally recognizing at least the results of what all this means. They will resist calling it a depression to the last possible moment, but increasingly there is no room left especially by way of their own regressions for any other word. It’s why even now many central bankers are advocating a new approach using more aggressive and forceful promises (forward guidance) because this depression is finally speaking their language. What Janet Yellen says is entirely irrelevant; it’s all in the numbers.

Stay In Touch