When we talk about or estimate long run growth rates, we intend to encompass entire cycles. In other words, whatever the long run average of real GDP growth, for instance, it takes into account both recession and recovery to harmonize into what would be a constant trend or potential. From that view, we would expect that while growth would be significantly less during recession it would be significantly more than average proportionately (in terms of the contraction) to revert back to potential.

In the case of the Great “Recession”, the unusually deep trough should have immediately been erased by a temporary period of unusually robust growth that would over time decelerate back to “normal.” That expectation should have been amplified by all the “stimulus” that was presented, but straight away there were signs that “something” was wrong (the “new normal”). The recovery never lived up to proportionality despite a QE1 then QE2. This stunted pattern was repeated all over the world.

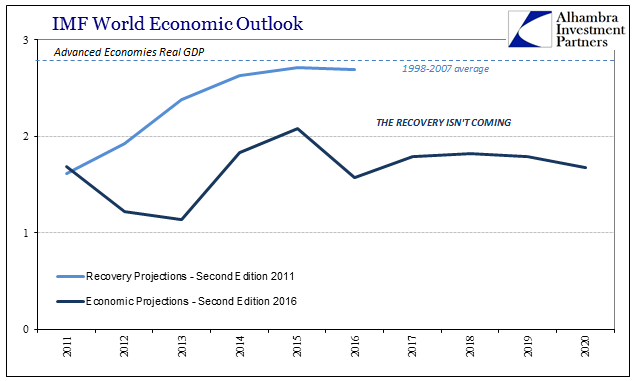

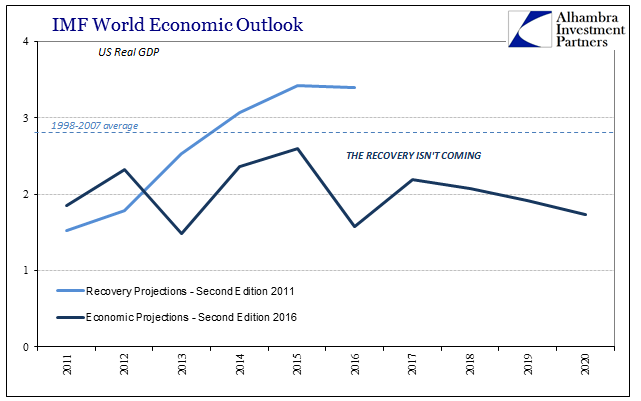

By 2011, the various econometric models had all but given up on full recovery, settling instead for just average growth without ever answering for the asymmetric hole left behind by the events of 2008 and 2009. The IMF, for example, in its second edition World Economic Outlook (WEO) for 2011 predicted that real GDP for the “advanced economies” would by 2014 resume something close to normal growth. In the US, it was expected that the economy would at least accelerate to above-average growth even if that wasn’t enough to completely offset the Great “Recession.”

The latest WEO estimates for the second edition 2016, however, have brought to a very rude end even those fantasies. Real GDP for this year, CY 2016, in the United States was written down enormously yet again. The current estimate is for just 1.58% growth, sharply lower than last year and even the first edition 2016 WEO estimate of 2.40%. Last October, the IMF had figured that real GDP would accelerated to 2.84% in 2016, meaning that more than 1.25% has been shaved off the outlook since then as “global turmoil” becomes increasingly real.

While that is concerning enough on its own, these reductions have finally been extended far into the future. Whereas in years past “temporary” weakness was met with reductions to immediate estimates, years forward would still estimate either average or better growth. No more; the IMF now see real GDP growth in the US picking up only modestly in 2017 before decelerating again to nearly the same atrocious growth as they now predict for this year.

The numbers for “advanced economies” as a whole aren’t as grim but are still much too similar. That means the US is instead of leading the world out of this mess (because of Bernanke’s self-proclaimed courage) is dragging everyone down into what is all but confirmed now as a depression.

To properly characterize these results and projections is to realize that “something” went horribly wrong in 2008 and 2009 such that what has come after is an economy completely unrecognizable to past trends and potential. That it would all date so easily to 2008 and 2009 (starting, of course, in 2007, specifically that August) only casts further doubt on the continuing convention assuming the Great “Recession” was a recession in the first place.

To this point, most officials have resisted the acknowledgement, preferring instead to see “transitory” factors merely delaying at least partial satisfaction of so much “stimulus.” The events of last year, as we are seeing in economies all over the world, destroyed for even many orthodox institutions that increasingly fanciful narrative.

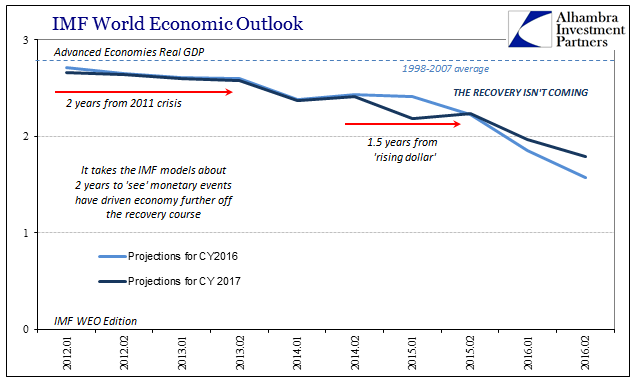

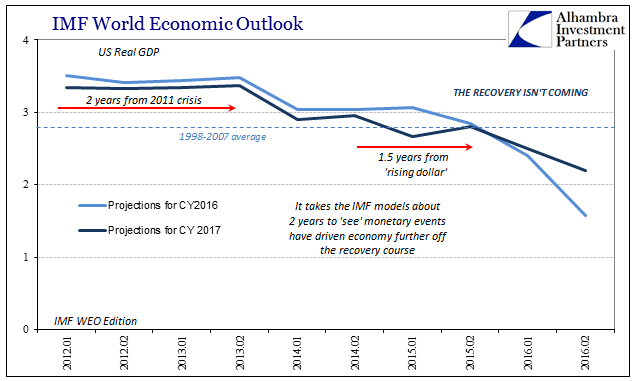

This is and can be only a monetary disaster, a fact further established by the delayed reactions of the IMF models. Economists did their best to ignore the events of 2011 and mid-2014 only to find out around two years after that the real economy was registering them as impactful against actual function. In other words, what were thought to be by “experts” and policymakers minor impediments easily set aside as they happened have been proved in time as actual reductions in long run (as well as immediate) growth and capacity. They ignored the weakness presented in the initial stages of the “rising dollar” as if “transitory” randomness only to find out that in these latest estimates for 2016 and beyond, conditions that by all orthodox assumptions should be free of those specific entanglements, that weakness has “somehow” become a permanent fixture.

The IMF for all practical purposes just declared the recovery dead, and by doing so effectively (certainly not explicitly) admitted that there was no recession in 2008 and 2009 after all, as “whatever” happened in the real economy then is clearly still ongoing. The fact that there are positive numbers even for GDP is a distinction without a difference; what matters is that the global economy fell far behind almost a decade ago and only falls further behind with each passing year.

Recessions are temporary matters to be overcome really with time and common sense; depressions are quite differently dangerous as damaging the very social fabric, but especially so when it takes years for those who should know better to even figure out it is happening. If it took the IMF models about seven years to finally move beyond the recovery fantasy, how much longer will it take them to figure out why? We just don’t have that much time.

Stay In Touch