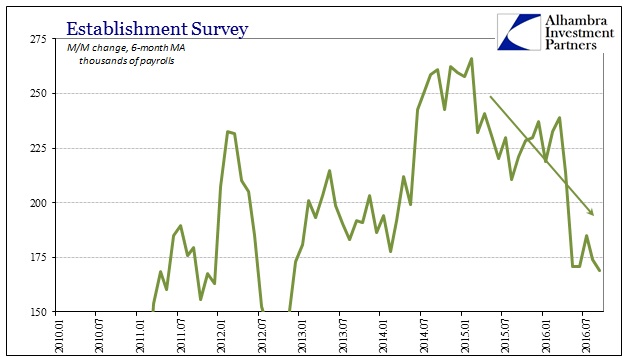

The September payroll report continues a string of repetitious unevenness that is the hallmark of these types of economic periods. The economy seems to appear strong then weak and then strong again so that just when “everyone” is ready to put the weakness behind, it disappoints all over again. It is a seemingly confusing condition made more so by especially statistics like the Establishment Survey. Though the headline “jobs” number is reprinted as gospel, on a monthly basis it is essentially meaningless. What I wrote in May with regard to the “weak” April report still applies:

There is very little value to begin with in trying to parse monthly variation, reflected in a wide confidence interval at just 90% confidence. For all we know the jobs market in April 2016 was exactly the same growth as March 2016 when everyone was far more pleased. What we really don’t know is whether both March and April should have everyone elated or seriously worried (obviously, the rest of the economic data points uniformly point to the latter).

At just +156k for September, the published confidence interval of +/- 115k means that there could have been as few jobs in September as was thought of the May report that so unsettled everyone, or nearer the June report headline which accomplished if only briefly the opposite. And since the published confidence interval itself hasn’t been updated though the data and calculations of errors certainly have, there isn’t any confidence (pun intended) in what we don’t know about the statistics. In other words, we really don’t know how many new jobs were added in September and further that we don’t really know by what range that uncertainty may actually apply.

A second straight month of disappointment to the gospel, however, has raised all over again the same questions that were brought up at the release of the April and particularly May reports – that were promptly forgotten with the huge “robustness” of June and July.

Payroll growth was disappointing for a second straight month in September as employers added 156,000 jobs, raising questions about the health of an economy that was expected to perk up from a prolonged slump in the second half of the year.

And another:

U.S. employment growth unexpectedly slowed for the third straight month in September and the jobless rate rose, which could make the Federal Reserve more cautious about raising interest rates…

The data suggested the economy was on firm ground, but not growing so swiftly as to knock the Fed off its game plan of raising borrowing costs only gradually.

“It’s an economy that is doing okay. It’s not necessarily accelerating, but it’s certainly doing okay,” said Jonathan Lewis, chief investment officer at Fiera Capital in New York.

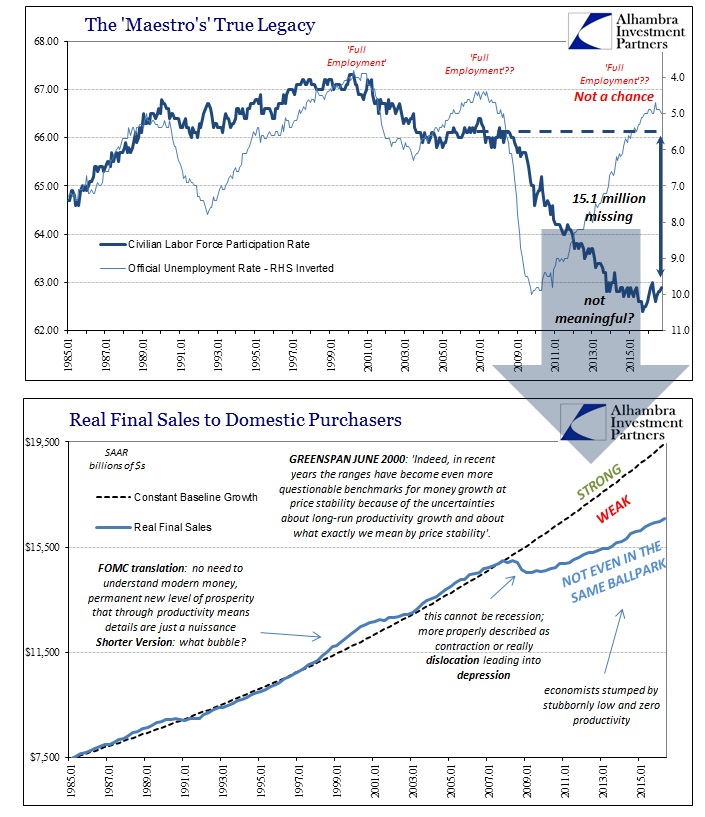

This is just not true, a testament to what improper focus on the short run has done to commentary. “An economy that is doing okay” violates every condition about economic sanctity with regard to the business cycle and overarching philosophy. A back and forth economy lurching between possible (and debatable) periods of strength and unnerving slowing is one in serious trouble – no more so than when it is supposed to be experiencing “full employment.” There is always some variation in the short run, of course, but taking steps toward “liftoff” it should be between robust growth and knock-your-socks-off robust growth.

What we find instead is not an economy just doing “okay”, it is one that is truly languishing in depression – year after year of only uneven and questionable expansion at best. Recession would be preferable, even a deep one, because in a normal business cycle reversion to the uninterrupted mean (undisturbed potential) means actually robust growth after some time. In this economy, there are “somehow” still only questions even seven years later.

We have seen this behavior before, and even under these same uncertain circumstances that weren’t then supposed to have been debatable. The Japanese went through this – twice. In 2000 as well as 2006 and 2007, the Bank of Japan was faced with the contradictions of its faith in QE/ZIRP “stimulus” and an economy only showing at most sporadic response to it.

How can ZIRP and money printing be so feeble? There is a reductionism that is extremely important in all of this, starting with the premise of QE. A significant dose particularly those in the trillions should not leave policymakers straining to find evidence of its effects. That should be true in the intermediate term but undeniably so over the long run. The fact that none of these central banks are able to escape with clear achievement can only mean that either “something” greater than QE is holding it all back, or QE isn’t “stimulus” in the first place. Both of those options lead to only one conclusion; central banks, the supposed masters of currency and money, don’t know near enough about currency but especially money…

The end result is an economy that goes nowhere, languishing in prolonged malaise seemingly caught in monetary limbo between perpetual recession and a recovery that intermittently appears to be just around the corner. It feels just good enough not be the worst case but also never completely breaking free of what feels like an unknown anchor. In the end, it is actually the worst of the worst cases, where the economy has been removed completely from the normal business cycle and left in indescribable, frustrating agony. This condition even has a name if but colloquial by design – Japanification.

BoJ officials raised rates at their August 2000 meeting based on a highly contentious interpretation of an uneven recovery/economy only to cut back to zero and add QE just seven months later. They did it again in July 2006 under similarly questionable circumstances, managing to get a second rate hike done in February 2007 by totally dismissing the US housing bubble collapse as “abating” “uncertainties” “overseas.” Unreformed faith in monetary “stimulus” makes policymakers and all those who follow them blindly see what just isn’t there.

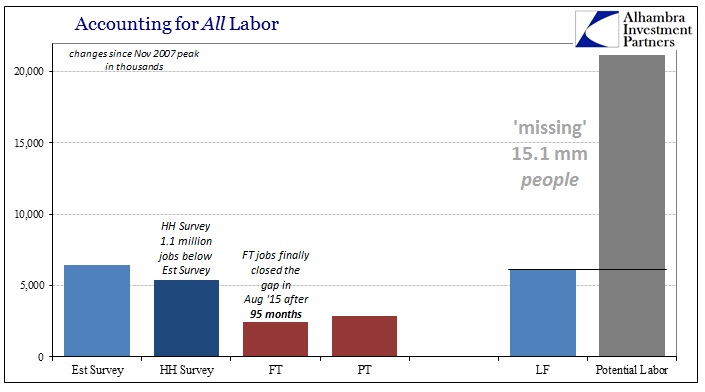

Thus, what is important about the Establishment Survey in 2016 is still just two major points. First, that overall it points to slowing across the broader economy over time, if not always month to month, when the opposite should be happening. Second, that condition must be factored under terms of the huge hole left by the Great “Recession” that importantly still remains.

This is not an “okay” economy; far from it. It is a disaster that continues to be prolonged by those who claim it is, aided by the increasingly established fact that traditional business cycle rules and interpretations just don’t apply.

Stay In Touch