As perhaps another in a very long line of indications as to what is unholy and wrong about today in banking and finance, over the weekend it was reported in the Financial Times that Deutsche Bank had received an improper accommodation on its “stress test.” In what can only be described as a clear example of cheating, DB’s capital position was boosted by the inclusion of $4 billion in proceeds from the sale of HuaXia, its Chinese lender subsidiary. The sale had been agreed upon in December 2015 but had not closed by year end (and is still to this day being held up, meaning that the ECB included capital that almost a year later still hasn’t actually been received).

The rules of the “stress test” clearly state that only completed transactions were to be counted. As the Financial Times discovered, the results from DB’s test indicated this accommodation as a conspicuous footnote that none of the 50 other banks were given even though several had also announced similarly uncompleted transactions that would have boosted their ratios. As amazing in its deception as that was, the truly appalling nature of it was revealed by the jump in DB’s stock upon opening this week after publication of the affair. In other words, “speculators” (of the non-evil persuasion, apparently) were bidding up the bank because they saw it as an indication that the ECB would surely go to any lengths to rescue it if they were already willing to dilute (fake, in part) the test results meant to calm everyone down.

It’s another sign not just suggesting the twisted nature of central banking but that for Deutsche Bank there really might be something to all this if the European Central Bank would go this far in perhaps just the early stages. The stock had jumped as high as $14.00 yesterday, falling back a bit today on perhaps a more seasoned perspective including just such a prospect.

Indeed, there is great deal to be concerned about far beyond just the DOJ fine and whatever its potential impact on DB’s “capital” position. In my view, the biggest risk to DB is the same risk that is being partially uncovered across the global (wholesale) banking landscape – it is the revolt of the math, specifically but not limited to volatility. In seeing this occur at BMO just recently, the anecdote only further raises our suspicions especially where Deutsche is concerned.

As I have been writing over the past year and a half or so, those concerns have already been raised – nobody noticed because they were too invested in trying to ignore how QE wasn’t what they all thought it was. When math starts to go bad, banks often face only stark and confusing (to the outside) decisions: let RWA’s rise and be forced to raise more capital at a time when questions about banks “having” to raise capital may make it more difficult and perhaps dangerous (Deutsche), or try to “earn” your way out by drastically shrinking operations and cutting back marginal resources before the auditors and regulators start questioning why your math doesn’t conform.

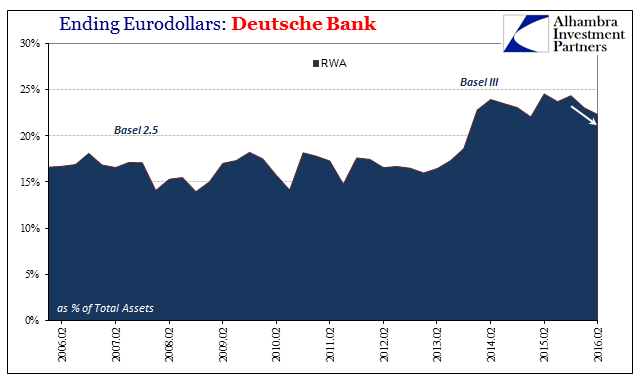

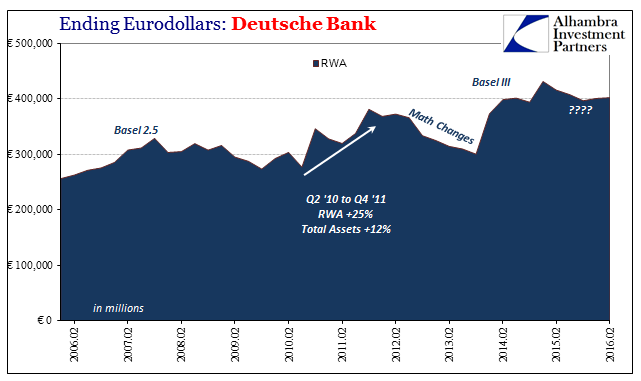

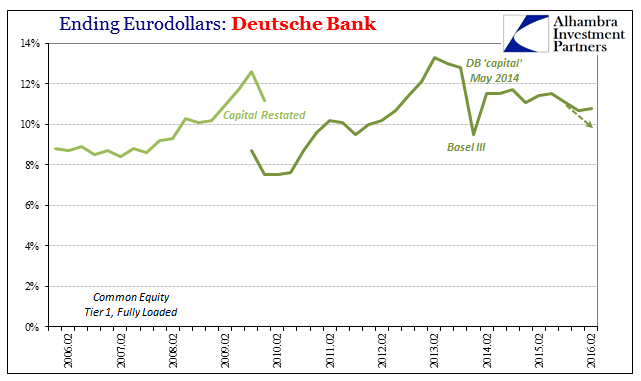

The issue is primarily how risk-weighted assets (RWA) are calculated with the understanding that a great deal is determined by internal often black-box models. Deutsche Bank more than perhaps any other global bank has been aggressive in this process. Until the advent of Basel III, DB’s RWA as a proportion of total assets were way out of line, something like 15-17% up until 2014, which shows just how much math has gone into an overall balance sheet calculation heavy with derivatives.

What is questionable, in my view, in 2016 is how that ratio actually fell as assets rose. To put it into actual figures, since the end of last year DB’s total assets have increased by €174 billion, including €100 billion due to positively marked derivatives contracts alone. Yet, for that increase in balance sheet and derivatives, total RWA only grew by just €5.5 billion. How is that possible?

Cursory examination via the Basel framework suggests that DB must have added a whole lot of safe assets, meaning those of such purportedly low risk as to be placed in Basel’s low risk buckets. Some of that is true and easily established (a large increase in “cash”, for example). However, the €100 billion in derivatives argues for a more comprehensive review, especially given DB’s history in this area as well as what we see of banks elsewhere.

First, we have to note that European accounting with regard to derivatives is different than what we find in the US and in other systems. Here, derivative books are whittled down by various means, often using netted contract values rather than notional exposures. For DB, as European banks, the asset side includes derivative contracts with positive values and those with negative values on the liability side. As a result, derivatives make up a much more significant portion of the presented balance sheet. As you can see above, currently derivatives are about a third of the whole on the asset side.

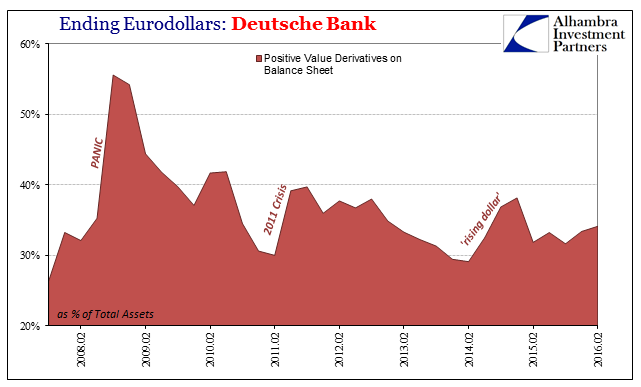

But what is also clear is that DB’s derivatives exposure tends to rise sharply during periods of stress. The reason for that pattern isn’t immediately clear except in the way in which traditional balance sheet accounting of these kinds of wholesale transactions is often backward. A derivative contract with a positive value is one that is cash flow positive, regardless of the position of the contract, whereas one that is of a negative market value (placed as a liability) is the opposite. From the perspective of funding, what is here accounted as an asset is really in many cases derivative funding hedged by what is on the liability side an offsetting negative market value contract.

From that perspective, we can better appreciate why the positive value derivatives rise both in absolute as well as relative (to total assets) terms. In the second half of 2011, during the worst months of that crisis, for example, total derivatives on the asset side increased by an enormous €304 billion, accounting for nearly all the increase of DB’s total balance sheet (+€314 billion). Given the asset expansion as well as the times, the bank’s RWA total jumped €62 billion, or 12%, as you would expect. The Common Equity Tier 1Capital ratio that had been rebuilt to 10.2% at the end of Q2 2011 fell back to just 9.5% by the end of the year.

Bank management responded to that “RWA shock” as I described several weeks ago:

Deutsche Bank, for one, began immediately to correct the problem. Just a few months later in January 2013, Jain and his management team were pleased to announce that the bank had successfully cut €55 billion in RWA in the fourth quarter of 2012 alone. The effect was an immediate increase in the bank’s core capital ratio to 8% from less than 6% (and insufficient) at the end of 2011. Of that €55 billion “improvement”, €18 billion was derived from the “roll out of advanced models”, an additional €8 billion was due to “data improvement exercises”, and a further €15 billion from “portfolio optimization.” Deutsche never provided much detail about that last one apart from language indicating “optimizing risk mitigation” from which we can infer at least more hedging.

During this “rising dollar” period, however, RWA performance has been completely different. In the first part of it, from the end of Q2 2014 through Q1 2015, DB’s total assets again expanded dramatically, by about €290 billion, largely the result of a similarly oversized increase (+€261 billion) in derivatives marked at a positive value. This time, though, the total of RWA grew by only €33 billion, about half of what had occurred in 2011. More curious still is what I described above, where assets and derivatives swelled again throughout the first half of this year but RWA somehow barely budged.

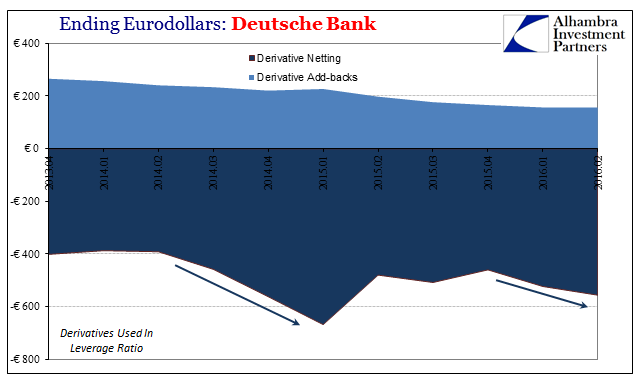

From that we are supposed to infer DB has become a much more effective hedger (or modeler). Some of their balance sheet presentations indicate as much, including the derivative netting the bank used for arriving separately at its leverage ratio. Banks via Basel rules are allowed to net out any derivative contract that has offsetting provisions, collateral, or positions so long as they conform to the applicable regulatory and accounting rules for netting.

Because of these figures showing significantly more netting (as well as significantly less added back) during the “dollar” episodes, DB’s leverage ratio during the first (Q3 2014 thru Q1 2015) was basically unchanged while in the second (Q1 and Q2 2016) it only fell from 3.5% to 3.4% (a lower leverage ratio indicates more leverage on the balance sheet). In short, the bank twice added huge amounts of derivatives that didn’t in any way make the bank appear riskier (in Basel terms) because of how they were “mathed.” In the case of the two quarters of 2016, it is about perfect; total derivatives in assets grew again by €100 billion while the amount netted out increased also by just less than €100 billion.

The effect on capital ratios is thus similarly muted, as described above. Via effective hedging, purportedly, the bank has managed what looks like an almost perfectly even keel of capital and leverage during the most tumultuous conditions since 2011. And good thing, too, because the operational loss last year and the subsequent hit to “capital” via lower retained earnings dropped the Common Equity Tier 1 ratio down to 10.7%. If RWA math had led to a similar outcome as 2011, DB’s capital ratio would have been well under 10% by the end of Q2. All it would have taken was a €30 billion increase in RWA to push the capital ratio that far down, a place that this weekend’s news about the problematic “stress test” shows authorities aren’t willing to visit.

It gives us motive to further suspect DB’s math. We are supposed to believe that contrary to other banks Deutsche has been more effective at managing its risks even as its balance sheet swells on derivatives exactly like it has in the past, all during “global turmoil” that has been marked more so by hedging and balance sheet constraints (globally) than anything else. It is, I believe, an increasingly dubious proposition, one that is reflected more and more in DB’s stock and other market receptions including funding and CDS.

To be perfectly clear, there is nothing outwardly which suggests serious problems – but that is the problem. The bank’s balance sheet presentations rely largely upon internal calculations that we can neither view nor verify, leaving often less helpful inference and suppositions. Ironically, these capital and even leverage ratios are meant as a means of reassurance. If there was transparency this wouldn’t be an issue. The lack of it plus the serious and quite relevant matter of how banks and their numbers often presented misleading views of certain institutions not all that long ago only further fosters this kind of mistrust. Faking the ECB “stress test” even if by a relatively small amount doesn’t help; especially now.

This all says a great deal about banking in general as commentary on the state of the eurodollar as well as regulations that are often described as fixing the problem. This is all backward to begin with, as the Basel philosophy going back to the beginning was always flawed; it was designed such that risky behavior can be made to appear far less so with the choice being often left up to the banks themselves and then monetarily by the assumed reliability of offered math (balance sheet capacity in the form of derivatives, hedging, risk offsetting, etc.). It is a system that practically guarantees suspicion, especially post-2007.

This was once very well understood, especially where the liability side mattered more if not at least as much as maneuvering on the asset side. As the FDIC’s 1978 Manual of Examination Policies declared:

“…capital ratios…are but a first approximation of a bank’s ability to withstand adversity. A low capital ratio by itself is no more conclusive of a bank’s weakness than a high ratio is of its invulnerability.”

Four decades later, all that is supposed to matter is the math. And it does, just not in the reassuring way Basel designers and reformers had thought.

Stay In Touch