In conventional thinking, China’s problems are China’s problems. As those related to its currency, it is believed a mere matter of either intentional policy (devaluation = export stimulus) or the outflow of “hot money” because of China’s unique circumstances. From this position, one populated by policymakers, what has transpired over the past year plus was all very confusing. It is exceedingly difficult to reconcile “hot money” outflows with global liquidation(s).

There were many clues that this was the wrong approach. The Treasury International Capital (TIC) data though delayed a few months actually provides a great deal of what is necessary to clear up the matter. What was evident even last year during the summer was that this was not just China’s problem. I wrote last September:

While China has received note for its now-open UST sales, it has not been alone or unique in that regard. Indeed, there have been several surprise “partners” in central banks (or national governments, which is not always one and the same) contributing “reserves” in the face of financial retreat in global “dollar” supply. Straight away, the UST holdings by Japan show the grim reality in far closer proximity, in this respect, to China than seems otherwise appreciated.

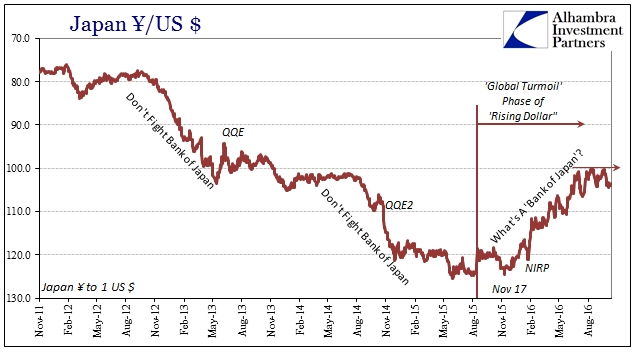

Central banks as a class were “selling UST’s”, and though China contributed perhaps a majority it was others across Asia but especially Japan that suggested widespread funding problems tied to the eurodollar that were being directed toward the Far East. From that realization, it was easy deduction to put together Japanese banks with Chinese “dollars.” That meant, of course, spillover for Japan. I wrote in early November 2015, less than two weeks before the yen began its middle finger (or whatever the Japanese equivalent affront might be) to the Bank of Japan:

What is more visible is, again, that China is not alone in its official sector struggles. From Brazil to even Japan, “dollar” wholesaling is in some high degree of irregularity. For Brazil and the oil export countries, for example, that isn’t surprising but the addition of others like Taiwan (dating back all the way to 2012) and Japan suggests both that hidden asymmetry as well as its more Asian aroma.

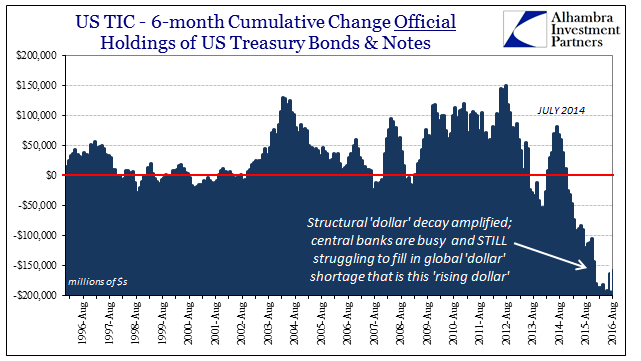

The eleven months since then have proven that the correct interpretation, especially with regard to Japan. Asia remains even now the center of “dollar” problems. Though there was less bite to them after February, they remained nonetheless below the surface and began boiling up again in mid-year with Japan (the basis swap problem combined with JGB’s) right at the forefront. The latest TIC updates for August 2016 continue to show that central banks, largely Asian but also the UK (for obvious reasons), were confronted with renewed highly negative amplitude and have taken a more active approach to dealing with it.

Total official sector net selling of US$ assets reached -$38.5 billion in August, -$44.2 billion in UST’s alone, both the biggest negatives since February. That would largely square with what I had described of “dollar” conditions at the time, this “something” that appeared to have provoked a change in behavior Japan as well as China. In the latter Asian domain, the PBOC swapped steady internal RMB liquidity for a more steady CNY exchange. As I explained here, it is a direct tradeoff where holding the exchange rate means “supplying dollars” to the private Chinese markets by “selling UST’s” which has the effect of depriving RMB of its “backing.”

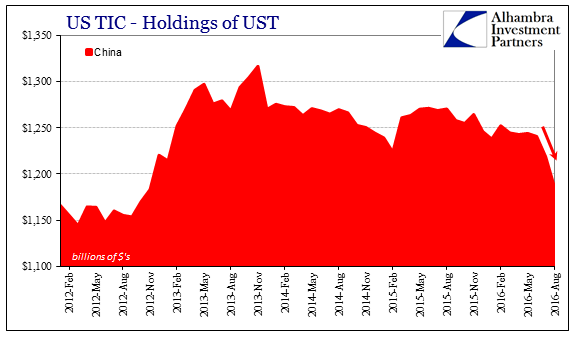

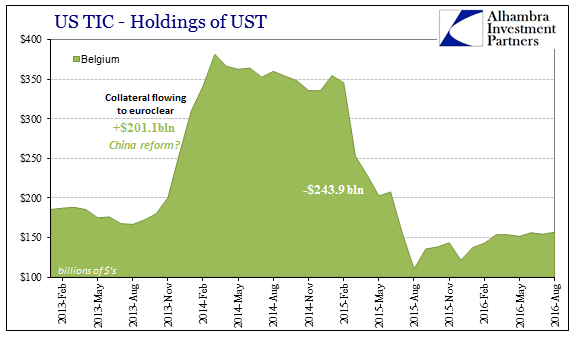

The TIC data for China, factoring both Belgium and Hong Kong (not shown here), confirms the middle part of that formulation, unusually heavy “selling UST’s”, and therefore the whole thing.

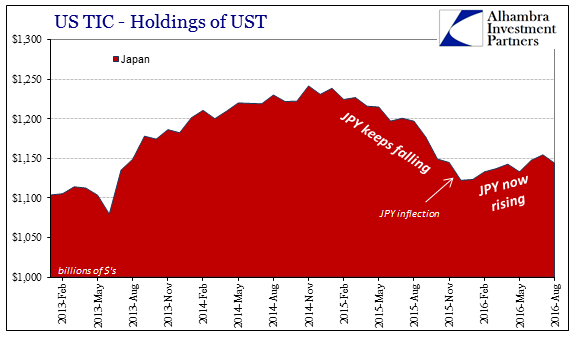

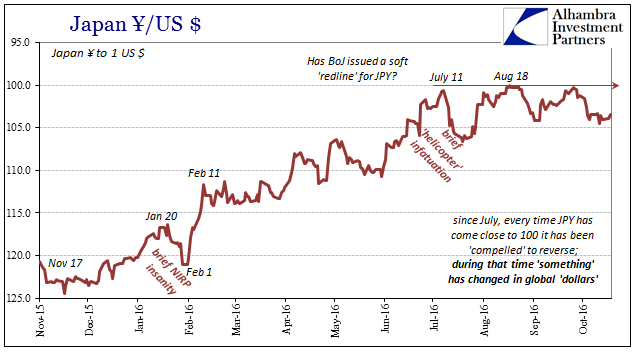

TIC recorded Japanese holdings also declined in August, further suggesting some kind of artificial influence (through BoJ’s UST swap?) on JPY. From November 2014 into December 2015, Japanese holdings steadily declined while JPY exchange at first continued its prior downward trend and then flattened out. From December forward, however, UST holdings in Japan started to rise again while JPY went on its own way contrary to BoJ intentions.

With Japan’s UST holdings falling in August coincident to JPY’s “soft ceiling” around 100, a potential redline that has held for months now, it raises the possibility that the Japanese are indeed acting in “dollars” perhaps in close similarity to what might have been happening in the months leading up to the “dollar” runs last August and January. It is just one month so there isn’t substantial enough to draw a hard conclusion, and this isn’t the first month during the yen’s rise where reported UST holdings have dropped, but the (to this point) coincident decline in TIC combined with the suddenly steady JPY does demand scrutiny with that in mind.

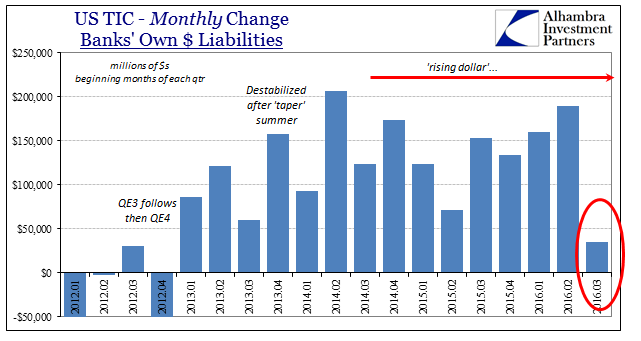

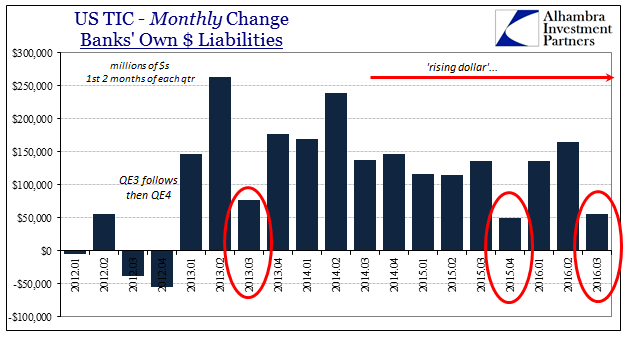

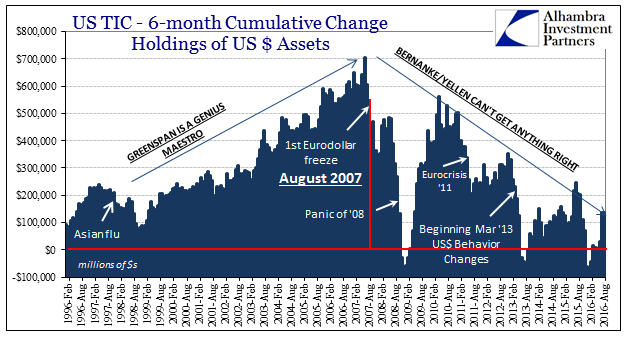

The backdrop for all of this remains the eurodollar’s unseen balance sheet capacity. The estimates provided by the TIC series are limited, but still very helpful as a partial proxy. As noted with the release of July’s figures, the estimate for bank liabilities in dollars was suspiciously low for a beginning month of any quarter. Global bank balance sheets have fallen into a distinct quarterly pattern where they end one quarter with hugely negative changes only to undo the declines in part to start the next one. For the prior month that meant:

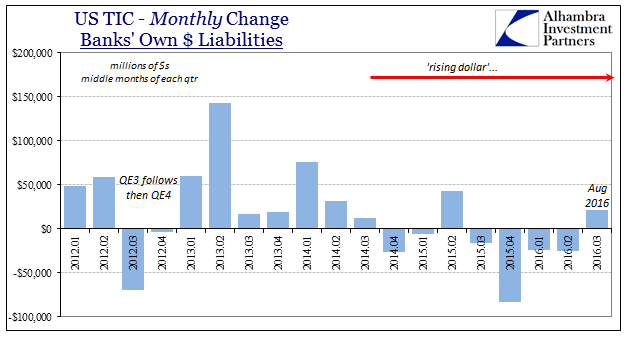

The bank data for July 2016, however, is concerning in terms of the lack of positive flow after quarter end. Banks finished Q2 2016 already at a slightly more negative pace, -$171 billion compared to -$163 billion in March 2016, and -$161 billion September 2015 at the end of that Q3. To start Q2 this year, as has been normal, banks’ dollar liabilities in April rose by +$188 billion more than offsetting the end of Q1 (March), which was also far better than the +$134 billion in October 2015 and thus a good reflection upon global “dollar” conditions at that time. To start Q3, however, only +$47.6 billion was reported for July – a huge discrepancy.

The total has since been revised lower, now just +$35.1 billion. Only some of that was taken back in August, meaning that though the figure was positive for a middle month for the first time since May 2015 it wasn’t nearly enough to offset the huge “dollar” hole to start Q3 (leftover from the end of Q2).

Combined July plus August, it does appear as if global banks pulled back some serious “dollar” capacity such that it would compare to October plus November 2015 as well as July plus August 2013 – neither of those periods were particularly stable for global liquidity. It certainly fits with the overall impression of the months as well as how and why these various largely Asian central banks dealt with it.

I think that all this is a primary factor in what are clearly more sideways, indecisive markets, including vital “dollar” parts like eurodollar futures that are seemingly caught between Asia and DC (FOMC votes). I wrote yesterday (subscription required):

I think what all this adds up to in very broad and general terms is where markets “know” that “something” is out there and they remain very wary of it, but aren’t yet willing to throw in the towel because since February it hasn’t led to the open, global disruptions and even liquidations that it did then. The possibility of that scenario remains a significant concern, especially if CNY gets going again, but perhaps there is optimism (from this indecisive perspective) that “somebody” can do something about it now that central banks have shown a more active posture as compared to 2015. Nobody is quite ready to buy (risk), but also not quite ready to sell (risk), either.

The TIC figures usefully supply more weight to that last part; the risk is there alright. And like last year, it is so far beyond just China being China.

Stay In Touch