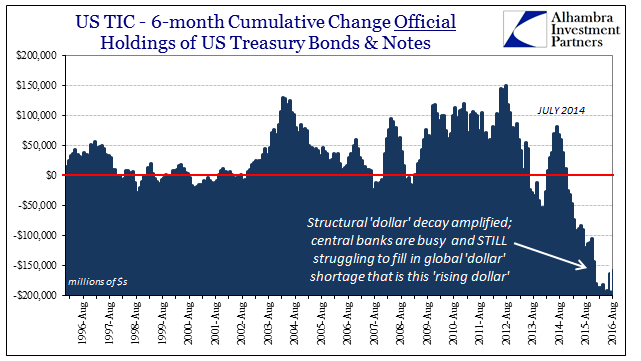

According to the TIC estimates, more than half a trillion in UST’s have been perhaps liquidated from foreign official holdings since October 2014. More than half of that total has taken place just in 2016 alone in the eight months through August. And, of course, in that time UST nominal rates have only fallen and sharply so, contradicting the nightmare scenario, at least as economists tell it, where foreigners dump treasuries so much that the 30-year bond bubble violently comes to its rueful end. Clearly, “something” else is going on here.

Rather than answer the discrepancy, more and more there is instead narrowed discourse. If foreign central banks are forced to “liquidate” (the quotation marks are as usual deserved because as in other cases where I use them the word in question in the wholesale “dollar” context isn’t to be taken as literal) not because they are worried QE worked so well the US economy is recovering so fast rates must rise, then we have to consider the other possibilities – of which there is only one. As noted yesterday, those not just in China are “supplying dollars” from out of their so-called stockpiles. How and when are topics for separate discussions.

If central banks are left to undertake such a drastically different approach to global money, from that other liquidity indications make much if not perfect sense. I have argued in the past that you can tell how bad it was in “dollars” by the level of these reported central bank “sales” of US$ assets; the more they do, the less the private market has done. That would seem quite consistent with other related warnings like LIBOR, repo, or swap spreads.

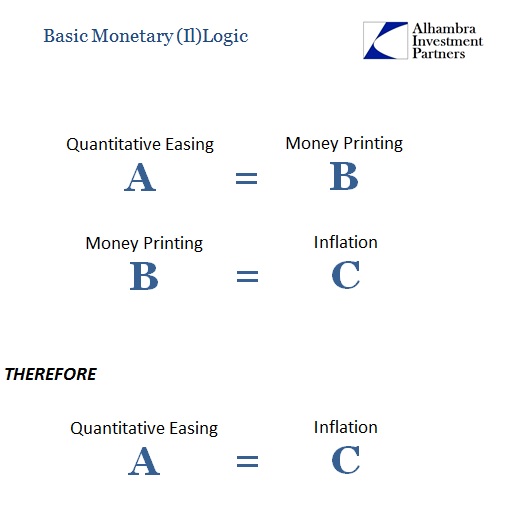

Global “dollar” illiquidity or even a shortage is a slap in the face of central bankers and economists, a complete contradiction to what is still believed by many of what QE was. Thus, they more and more refuse believe their lyin’ eyes.

That’s because the once-dependable indicators traders relied on for decades to send out warnings are no longer up to the task. The so-called yield curve isn’t the recession predictor it once was. Swap spreads are so distorted they can’t be trusted. Even the vaunted VIX — sometimes referred to as the “fear gauge,” is leading its followers astray, strategists say.

This Bloomberg article even manages to quote one analyst who says, “There aren’t a whole lot of reasons to believe there are funding strains in these big financial institutions.” As I write for my RCM column tomorrow:

It would be easy to respond with Deutsche Bank, too easy really, but it’s not as if DB is an outlier. At worst, the big German bank has been the leading edge of an industry-wide downward lurch. What’s even more ridiculous is that you can establish this with just a few minutes work by plotting the price of Deutsche’s stock or those of European banking as a whole or even US banks (of the wholesale variety) as a group against the 10-year swap spread now persistently negative. They all move almost perfectly together, with their unmistakable inflection last summer just before CNY broke and “global turmoil” rather predictably followed.

It’s an entirely emotional response because it challenges some very core beliefs. Primary among them is that the technocracy cannot ever be so incompetent to have claimed to have printed money that nobody can find. It shows up on the Fed’s weekly H.4.1 alright, and so that is enough for these people.

As central banks around the world pump billions of dollars into the global economy every month and policy makers pass regulations to safeguard against a relapse of the 2008 financial crisis, the market’s best and brightest say some warning signals are flashing at precisely the wrong time.

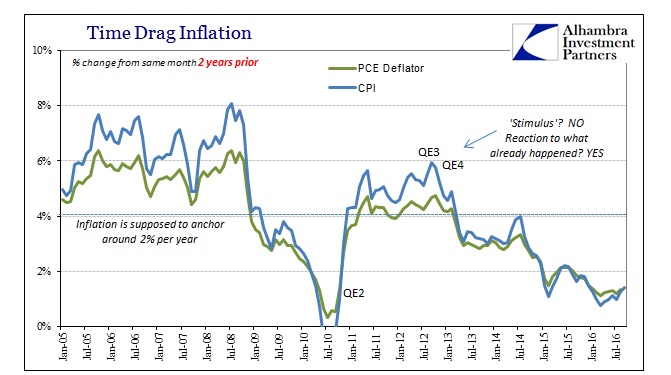

Billions of newly printed dollars pumped “into the global economy every month” would show up first in consumer prices as sure as the sun rises in the east.

This plus the unemployment rate are the two pillars of denial, and, obviously, they run very strong and deep. How could the “best and brightest” be so wrong about something so basic? It would take years to put it all down on paper (or in cyberspace) but a good place to start is Janet Yellen’s speech last Friday. Even with that it will be hard to accept from among the faithful devotees to the technocracy, even when delivered directly from the horse’s mouth.

A good part of this refusal to accede to “dollars” rather than bank reserves is as I have been arguing for years. In the case of the yield curve, for example, its flattening and shriveling is now being dismissed because in the past such price action in UST’s meant recession. That didn’t happen, therefore in this limited, linear worldview of recession/not recession the yield curve has been supposedly, as TED and swap spreads, sending false warnings.

“Perceptions that a flatter curve was presaging a recession were obviously wrong,” said Ward McCarthy, chief financial economist at Jefferies LLC. “We’re in one of the longest-running expansions on record. You have to look at the behavior of financial markets through the prism of central-bank policies, or central-bank balance sheets.”

Again, words have meanings and in this case the quotation marks are demanded for “expansion.” The fact that it has been long-running is precisely the problem, and the very one that the yield curve has both predicted correctly and continues to indicate, even factoring this latest minor selloff. To the hardened devotees of orthodox economics, low nominal rates are the work of central bank stimulus; in the real world, low nominal interest rates occur only where money has been tight and thus economy unusually but consistently bad. The yield curve in this situation doesn’t suggest imminent recession, rather it proves the last one never truly ended and thus was never actually one to begin with.

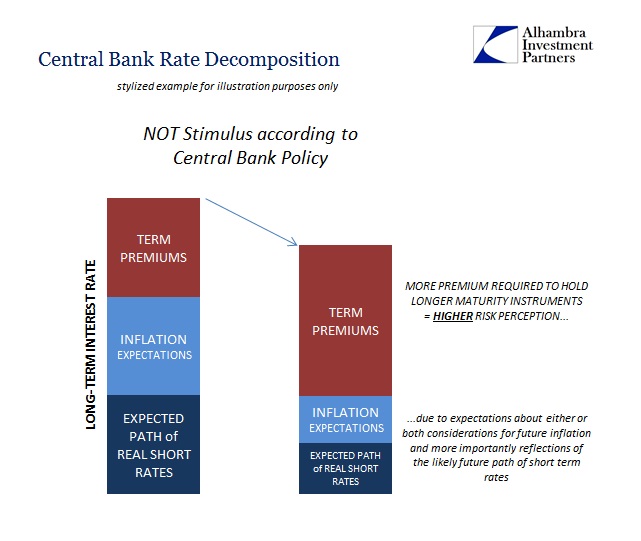

Even Ben Bernanke would be forced to admit the logic of it, if ever he could be separated from his attachment to the aid of unknowns. In other words, there is no actual evidence that the decline in nominal rates throughout this “selling of UST’s” was the “good” kind due to “term premiums.” On the other hand, there is a great deal of evidence that falling rates and collapsing curves were due to the two other components that we can quite easily find direct evidence for: shockingly low future short-term rates, and an equally shocking and low path of expected inflation.

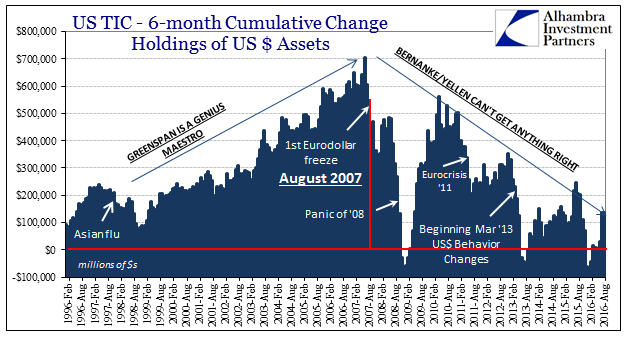

There is obvious internal consistency in the “dollar” story, from foreign central bank actions to money market conditions to the growing economic consequences of it all. That is why it must be denied, called meaningless the more widespread and uniform it becomes. QE is money printing, end of story. Economics is not a science; it is so clearly a cult. Anything that contradicts that mainstream dogma is to be declared heresy. There are no warnings, there is only what economists tell you.

Stay In Touch