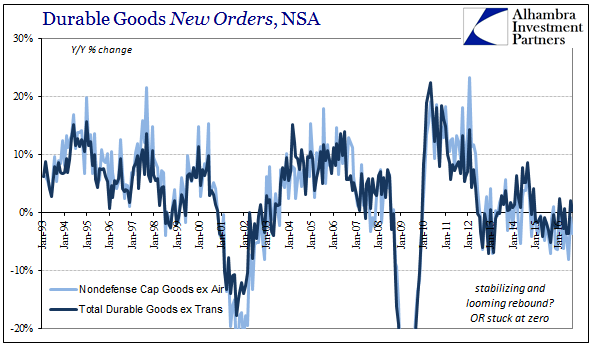

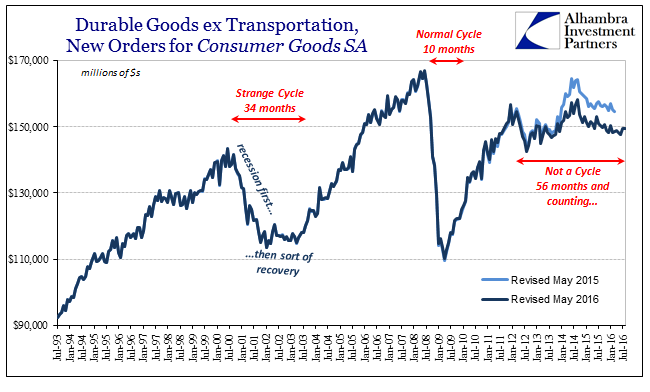

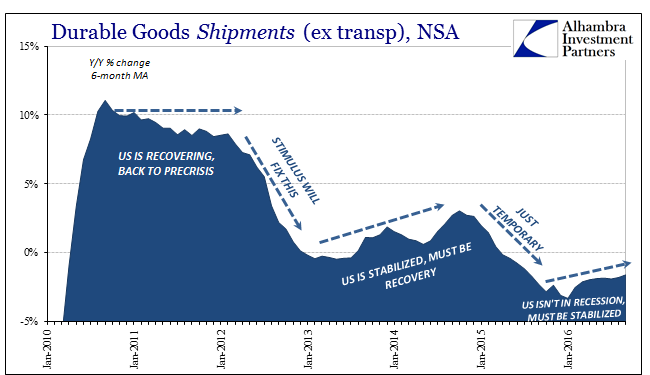

Durable goods continue to show that there is no difference between the economy of 2015 and the one being described by these numbers in 2016. To the “transitory” narrative, it is the death blow, which is why so many central banks and central bankers are busy exploring other options (while as quietly as they can writing down the future economy). To others, there is hope in that condition especially since for a time it looked like recession for this year. Where the glass is half full, at least 2016 hasn’t gotten a whole lot worse.

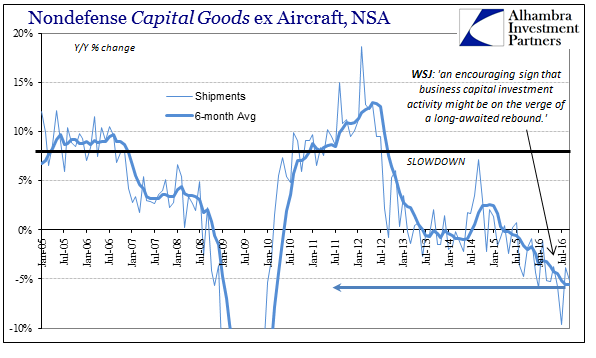

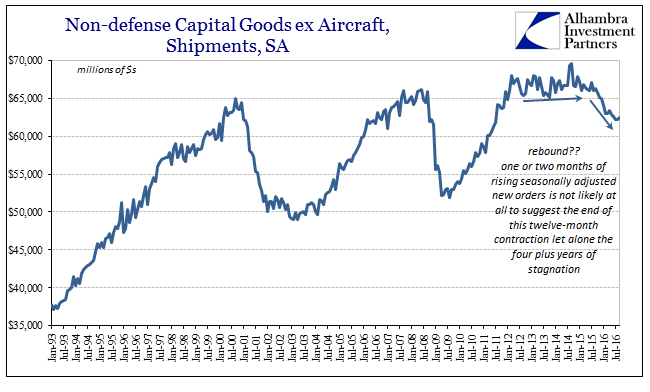

The statistics show that everything is stuck, at best. Durable goods shipments were down 0.5% year-over-year in September 2016 after being up almost 2% the month before; new orders were flat. Capital goods continue to see the worst of it, with new orders down almost 4% in the latest month while shipments fell by 5.2%. These circumstances are the continuation of two years of the wrong direction. To some, durable goods might show stabilizing, but in terms of capital goods businesses don’t appear to arrive at the same conclusion (and it’s not all energy-related).

The story of durable goods is the story of the economy itself. Why wouldn’t it be? It is a segment related to consumers in some of the most economically-sensitive ways possible. Big ticket items tend to sway with overall economic conditions, including consumer perceptions about the future. The less confident you are about what’s just over the horizon the less likely you are to buy expensive stuff.

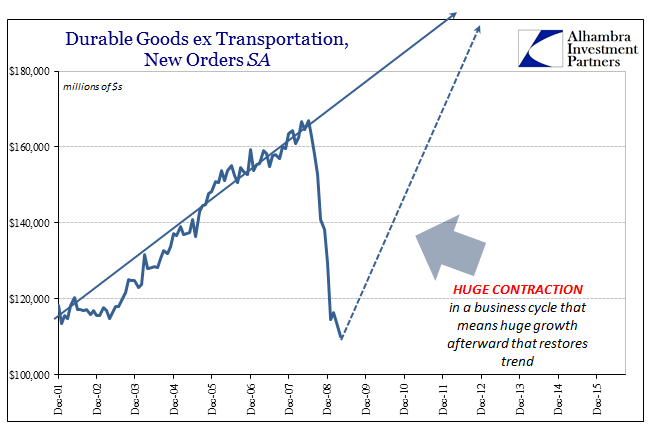

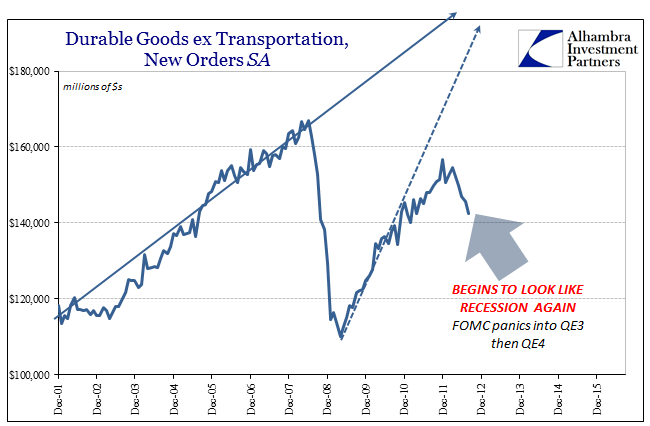

It all started with the shock of the Great “Recession”, but if it was to be a recession and normal business cycle that meant the prospects of huge growth despite the enormity of the hole that the economy would have to be overcome. Monetary officials around the world knew the scope of the challenge, which is why they quickly turned to “extraordinary” policies and in heavy (it was thought at the time) doses.

Almost immediately, however, there was a problem. The recovery started to shallow, which pushed some at the time to characterize it as just a “new normal” of asymmetric growth. It was a recovery, they thought, just not as strong as it perhaps should have been.

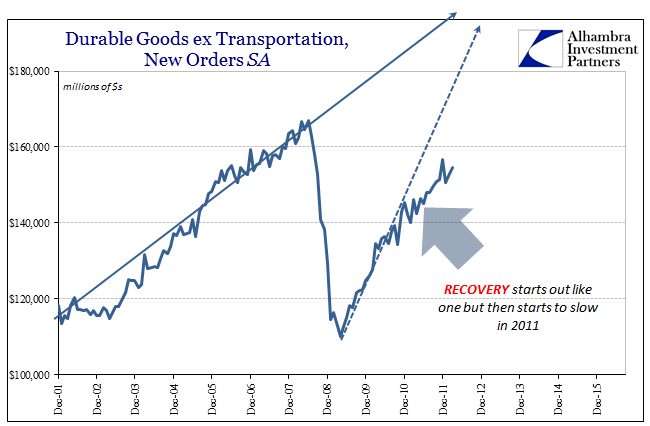

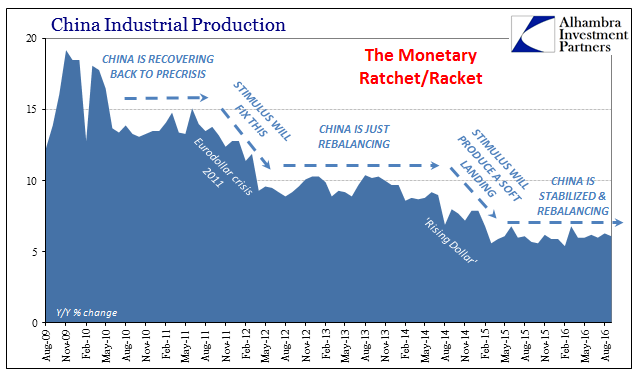

The first serious economic setback followed closely the monetary one in 2011. By early 2012, the economy here and globally started to weaken and do so in such serious fashion that it at the time threatened renewed recession (and in some places like Europe did occur). Central banks around the world responded with coordinated “stimulus” meant to overcome that drag and reignite latent recovery forces that economists still believed valid.

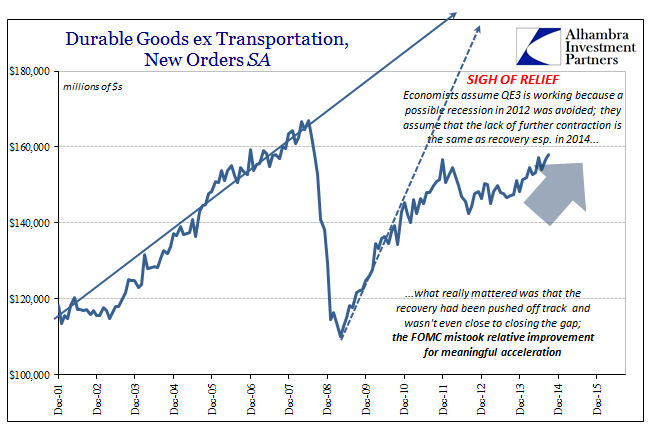

What followed that downturn in 2012 is the main source of how everything afterward has been misconstrued. QE3 ignited stocks in the promise that it would work, while in the economy there was no recession but also no recovery from the weakness. The mainstream opinion turned as if avoidance of recession by 2013 was the same as actual growth, or at least the precondition for it. That view was furthered in 2014 by also mistaking relative improvement for actual improvement. Far too much was made out of what was so very little (a condition further established by later benchmark revisions, but one that didn’t need them to still be clearly appreciated).

Even though by 2014 there were positive numbers and even more so in durable goods as well as other accounts, it wasn’t the same as recovery or the continuation of a normal business cycle. Stuck in that frame of reference, however, policymakers were essentially fooling themselves by failing to appreciate the overall context that was actually quite repressive as well as overriding. “Something” was still very wrong, even if in traditional terms “expansion” was still proceeding.

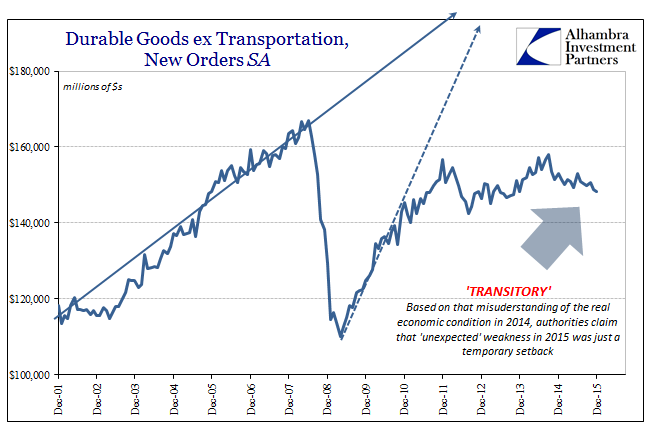

Because of that altered state, economists misread what came next – the effects of the “rising dollar.” Viewing 2014 as, again, meaningful acceleration, the mainstream interpretation of what was very serious weakness was to dismiss it. Believing the hastening in 2014 as real, the negatives of 2015 were downplayed as either a minor disturbance (manufacturing is only 12%) not worthy of consideration or a temporary condition that would soon enough dissipate of its own accord.

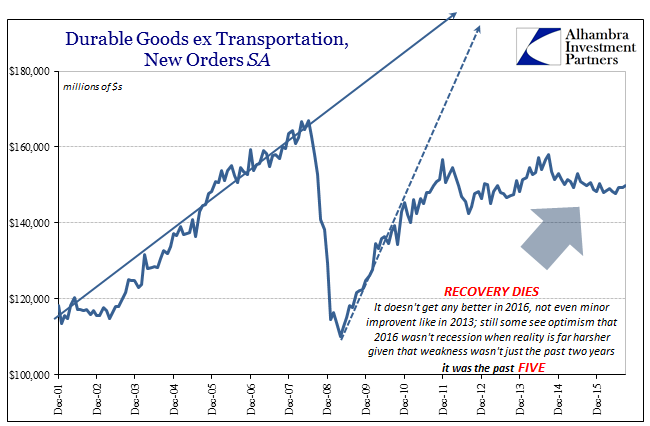

By that view and expectation, 2016 had to be a meaningfully improved environment even if still by relative comparison. It hasn’t been. As durable and capital goods show well, the economy remains as it was. From the perspective that viewed 2014 as actual acceleration, this is a surprise and a shock; from the wider context that sees the disparity of where the economy “would” be had this all been contained within a normal cycle, it was just more of the same.

Here’s the part that economists, policymakers, and the media (all three largely indistinguishable from each other) miss – lack of true growth is contraction, and the worst kind because it isn’t recession contraction it is depression contraction. In the former, all is forgotten after a time; in the latter where even occasional positive numbers can be and often are highly deceptive, time is the biggest problem. In 2016, that latter realization can no longer be avoided, which is why we have seen orthodox institutions like the IMF and World Bank give up completely on the recovery idea, and where central bankers are now after defending QE and ZIRP (and NIRP) forcefully for years suddenly admitting (some of) their faults and desperately searching for alternatives.

It is not a business cycle; there was no recession in 2008 and 2009. There was a contraction but it was instead a full dislocation which represented a huge shift in systemic factors starting with, of course, the eurodollar; what we see of US conditions is also what we find all over the world.

At each of these monetary intervals, the global economy absorbs the hit and weakens but doesn’t recover from it; what appears to be stabilization or even minor improvement is really just the interim between monetary events that transpire only in that one direction (negative pressure). Trying to understand what has been taking place from a cyclical perspective is like what it once was in trying to read ancient Egyptian hieroglyphs before the discovery of the Rosetta Stone.

Letting go of QE and accepting the (decaying) “dollar” as the actual monetary basis for the global economy is the key to translating what appears to be an impossible enigma into a coherent basis for understanding what is still, tragically, occurring.

Stay In Touch