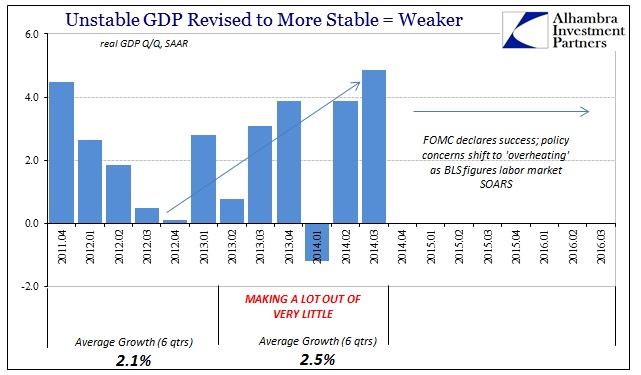

The ultimate lesson for learning not to rely on one quarter of GDP growth was actually two quarters. In the middle of 2014, GDP posted back-to-back gains that at the time seemed nothing less than fantastic. Even with residual seasonality revisions and new benchmarks, those two quarters remain prominent landmarks in an otherwise bleak landscape. And that is the whole point; despite the fact that the BLS currently figures Q3 2014 GDP at nearly 5%, such a strong estimate meant absolutely nothing as far as telling us anything meaningful about the actual state of the economy and how it might move forward. It was pure fool’s gold.

This should not have been a surprise, but it was because so many people were tired of gloom and economists so desperate for tangible “proof” they weren’t all frauds that they all saw what they wanted rather than what actually was. Underneath it all, there was, as I described yesterday, only great trouble and stubborn weakness. What looked good to a lot of people who should have known better was in reality just a momentary, isolated period of less bad.

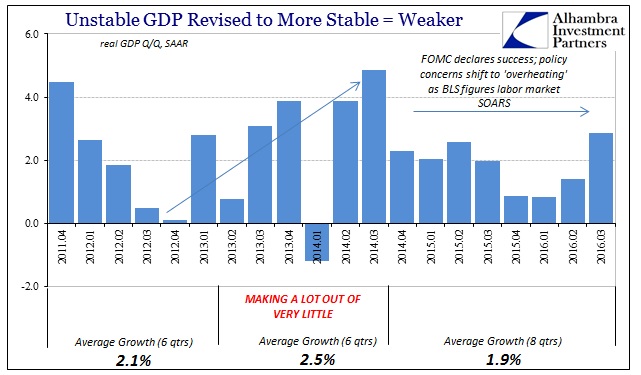

Those are the only two speeds of this economy in this depression – bad and less bad. If 5% was less bad, then what is 2.86%? As you can plainly see above, the estimate for Q3 2016 was the highest since that last less bad quarter in 2014; but at only just more than half the growth rate. Predictably, the current headline is being celebrated as significant for all the same reasons that one was.

A bigger than expected 2.9 percent annual growth rate in the third quarter was cheered by analysts and investors as a sign that a moribund economy is finally picking up speed. The report, the last read on the U.S. economy’s pace of growth before the election, was also seen as giving Democrats a solid talking point about the Obama administration’s economic policies.

It is the day’s message in what counts for economic news and analysis, as the idea will be pushed over and over that “a moribund economy is finally picking up speed” even though this same “interpretation” has been issued and disproved time after time over the years. The reason is quite simple: one quarter does not erase all those of lesser “speed” that came before it. In fact, it is those quarters that make all the difference. Even the same CNBC article is less unrestrained in its giddy acceptance of Q3’s headline:

But a closer look at the numbers show that the economy may not be as strong as the headlines indicate…

There were other signs that the economy remain weak. Consumer spending slowed, and investment in housing fell. And the growth of final sales — a measure of the overall strength in demand — rose by 1.4 percent in the third quarter after gaining 2.4 percent in the previous three months.

All of which points to an economy that is growing, but remains stuck in low gear.

Though there is unusual candor and reality in this assessment, it still downplays and hugely understates the significance of it. Even if we assume that the 2.86% estimate was perfectly solid and valid, it is still nothing to get excited about. In the context of the past seven years, it could be classified as “less bad” but only because these seven years have been, again, all bad. When 2.86% ranks among the best, you know there is something really, really wrong.

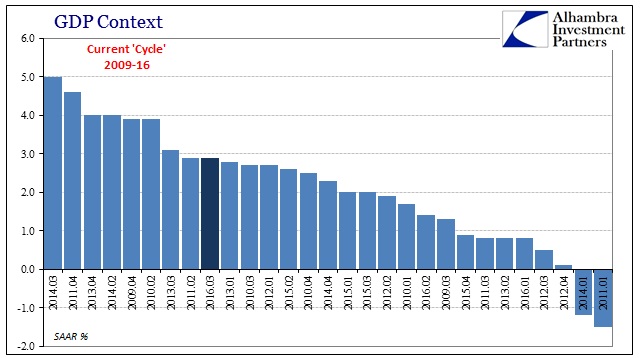

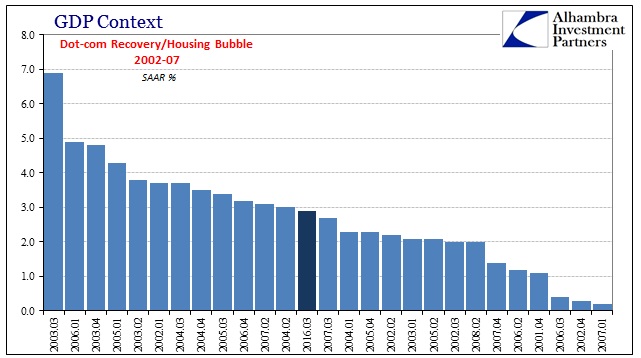

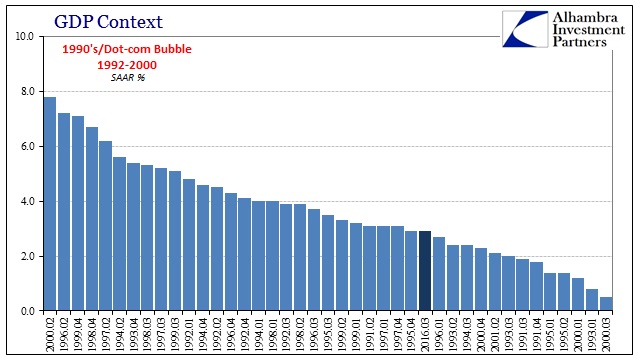

If we put this quarter in with the dot-com recovery/housing mania its standing falls to what would have been more like just average.

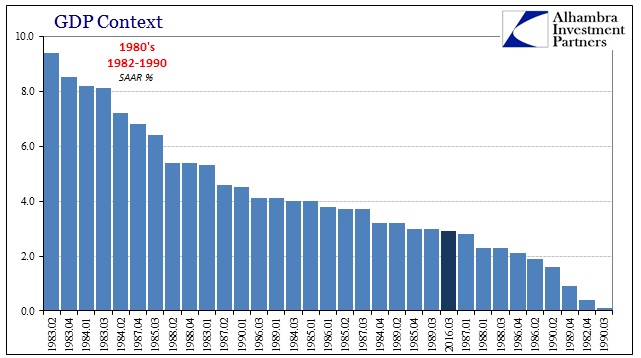

But putting into the context of periods where economic growth was less arguable has the effect of demonstrating conclusively how the current economy is so wrong. In either the 1980’s or 1990’s, 2.86% would rank among the worst results. In fact, in the 1980’s it would be barely more than several quarters of the near-recession around 1987 and those that felt the growing effects of the full S&L crisis that would develop into the 1990 recession.

This is not just a trivial distinction of subjectivity like ranking college football teams; it has significance in terms of what it says about the economy now and what it means for the future. When the “best” quarters can only manage what would have been classified in the past as indisputably weak, there is clearly “something” serious holding it all back. In those years past the natural variability inherent in the GDP statistic itself wasn’t noticeable even though it has always been there.

In other words, when GDP expanded by 5.2% in Q1 1983 there might have been a huge boost in soy bean exports, too, but it made little meaningful difference because 5.2% was typical and natural variations of these kinds were of far less proportions. But when GDP has a tendency to be persistently low, soy beans can seem to make a big difference but only for the statistic not the actual economy (this is the same in the positive as the negative variations that we saw in the cold winter quarters; in a truly healthy economy GDP wouldn’t seem much affected by either soy beans or snow).

The hallmark of this depression is that it is often measured with positive numbers, and that has the effect of being highly misleading. As I wrote yesterday:

Here’s the part that economists, policymakers, and the media (all three largely indistinguishable from each other) miss – lack of true growth is contraction, and the worst kind because it isn’t recession contraction it is depression contraction. In the former, all is forgotten after a time; in the latter where even occasional positive numbers can be and often are highly deceptive, time is the biggest problem.

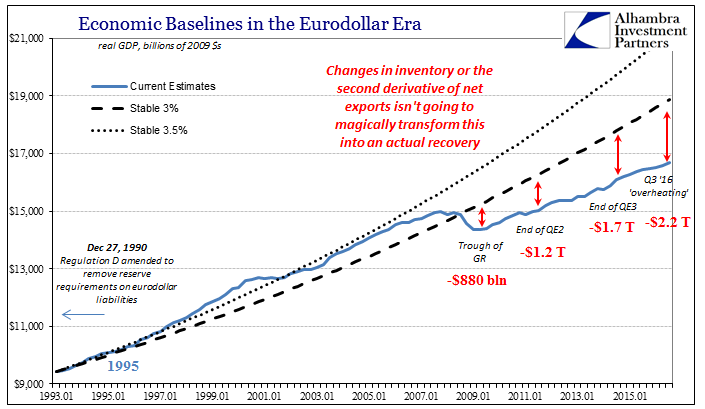

Actual and meaningful acceleration for the US economy would be marked by 6% or even 8% growth at this point. Alternating between bad quarters and less bad quarters is just more of the same depression contraction, where the cost in GDP (time) is now at least $2.2 trillion (to the low 3% long run baseline) and very likely double that (to the historical 3.5% long run baseline). By any reasonable standard, 2.86% isn’t good even if on the surface it is better.

Stay In Touch