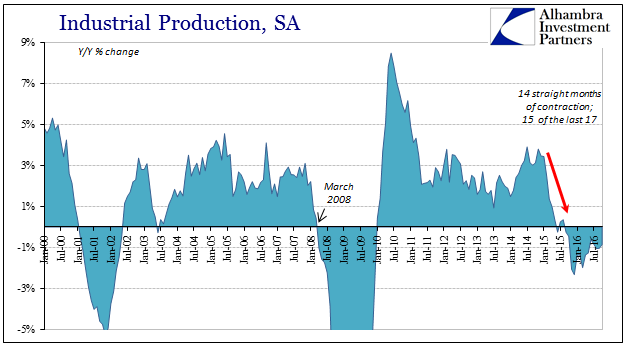

Industrial production continued its slow, shallow contraction, unusual in any economic climate but perhaps more compelling here in describing the different direction markets are taking. Clearly, as discussed several times before, certain parts of certain markets are betting that different is going to be effective where the same old was clearly not. The actual economy, however, has yet to show any of that same optimism because there is a very real chance that is all it is or ever will be (is different truly different, or just different types of the same kind?).

The statistics remain utterly grim; not in the manner that 2008-09 was grim, rather in the way the dot-com bubble collapse was pure torture, down a little bit at a time stretched across year after year. For the fourteenth consecutive month in October 2016, IP contracted in the US. There has been no appreciable difference between last year and this one, except that the contraction in US industry didn’t appear until halfway through 2015, whereas it has been falling for the whole of 2016 so far. In other words, IP is worse where the whole economy after last year was supposed to be meaningfully better.

In terms of month-to-month changes, IP was practically unchanged in October from September which was down from August, indicating that the seasonally-adjusted rise during spring seems to have faltered. For consumer goods, IP has declined again for each of the past three months since the seasonal upswing.

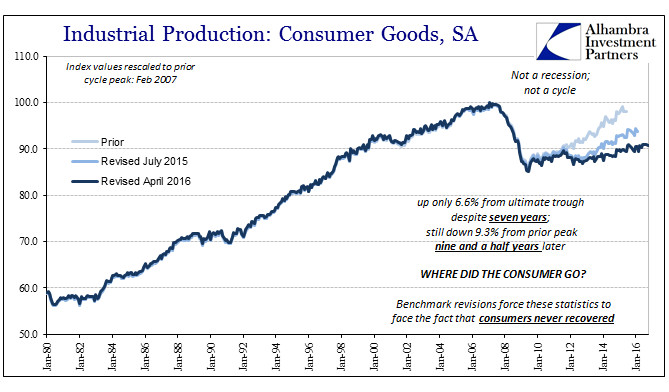

While that is an indication of the current weakness and its frustrating stubbornness, it also expresses the growing costs of being so far behind from where the economy “should” be, or at least what it would have been had the Great “Recession” actually been a recession. As a reflection of just how bad this depression has been for consumers above all other parts, the production of consumer goods is only 6.6% (total) above the trough registered in June 2009, more than seven years ago! That remains more than 9% less than the peak of February 2007, a comparison that is agonizingly approaching a full decade. It cannot be a recovery or even business cycle where production for consumers is not even halfway back after so many years.

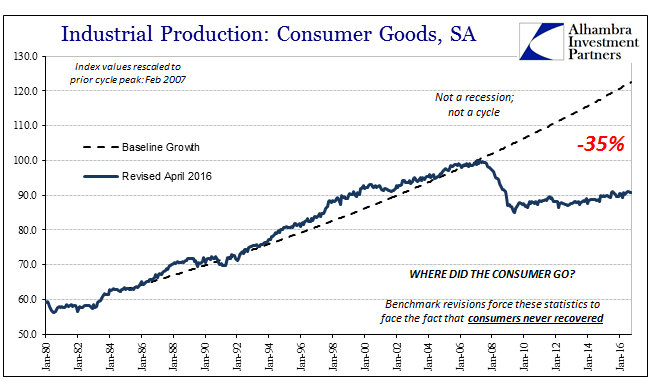

In reality, however, the true scale is not measured by what was, rather it is more aptly revealed by what an actual recovery would have looked like. In that view, the current level of US production of consumer goods is an enormous 35% less than the prior baseline trend that extended back a long, long time. That is by any rational basis a depression; a more than temporary and significant change in economic level and function. The longer it goes, the more permanent it appears to be.

Again, we see this pattern repeated in any number of economic accounts, including those in and of GDP, but in terms of IP consumer goods you get a good sense of how the very real struggles for consumers translates directly into lost potential on the production side; thus, how one feeds into the other and back again. At the very least, you can appreciate why Trump won all the states of the rust belt.

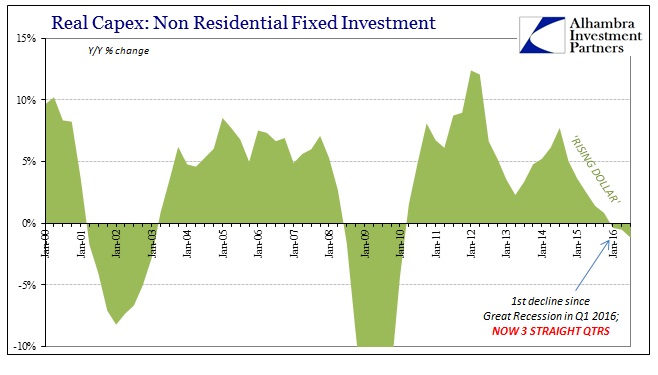

With that limited economic background, the reductions across business activities these past two years are why the whole economy seems to swing on those changes. Absent any actually “strong consumer” with which to take up additional slack that is always present in any other economic condition, as business investment goes so does the marginal economic direction. That means crude oil production, total capex, and especially automobiles.

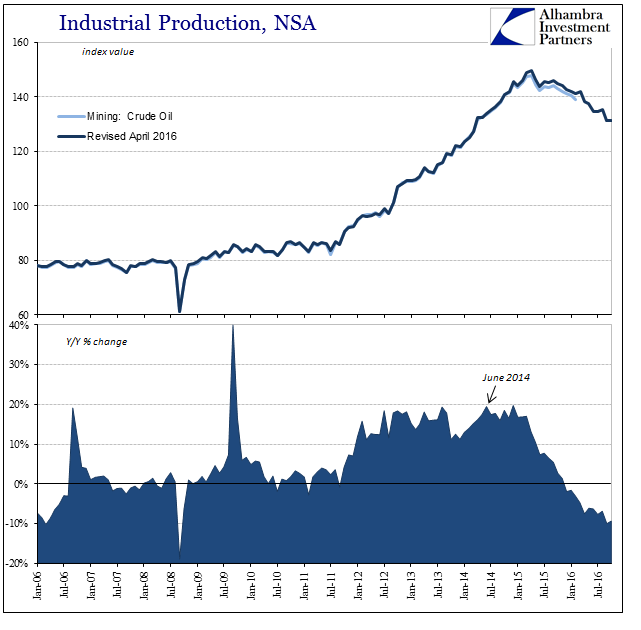

Crude production despite the rhetoric has not collapsed, perhaps as a reflection of the perceived prospects for oil price stabilization. In the IP statistics, mining for crude was off 9.3% in October, following a 10% decline in September. The 6-month average, which didn’t turn negative until March this year, is only -7.7% in October despite two and a quarter years of a commodity selloff and oil price crash. That would seem to suggest oil production is not going to crash and reset, rather it could be a drag for a very long time.

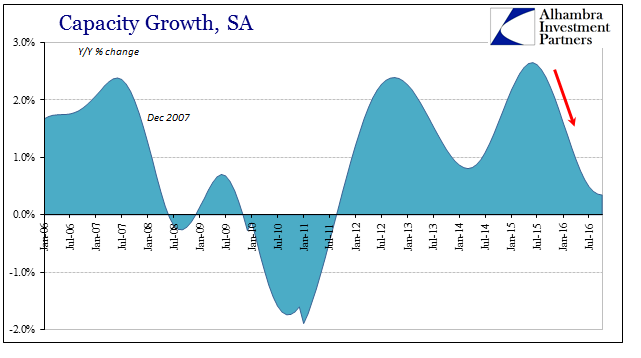

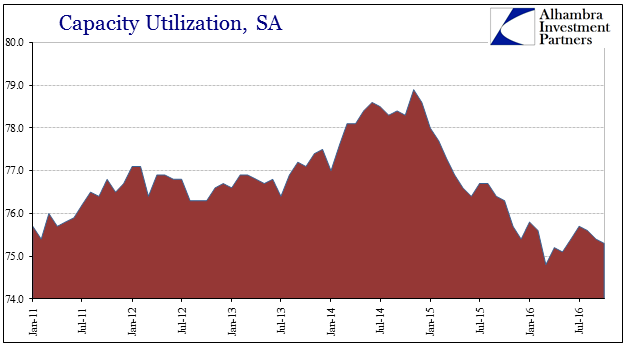

Capacity utilization declined again in the latest month, down also for the third time in a row since the spring upturn. At just 75.3%, it is just barely above the recent low in March. And as that slack in capacity lingers, businesses tend to scale back additional capacity growth. The Fed reports that total capacity for US industry was just barely positive again in October, having been increasingly below 1% each of the past seven months dating back to March.

The actual levels and estimates are slightly different, but the overall trend is the same as is measured in the GDP statistics, one of the reasons GDP has been much weaker since the middle of last year than the already weak years before. Without capex to provide even a small boost where consumers clearly cannot, what will add momentum? Highway spending?

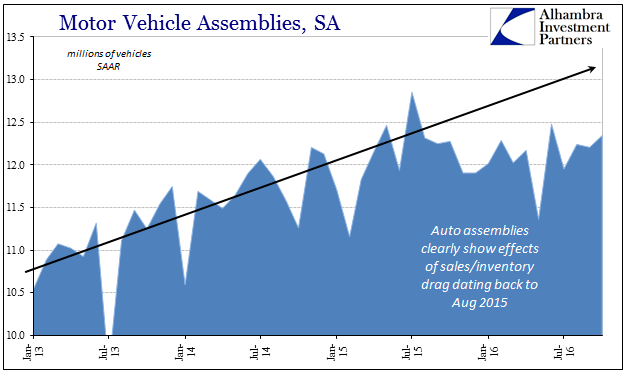

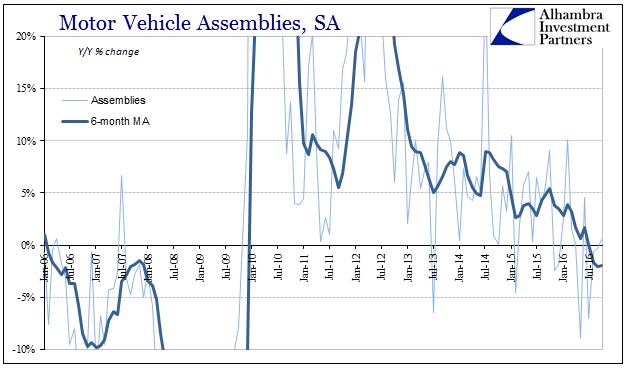

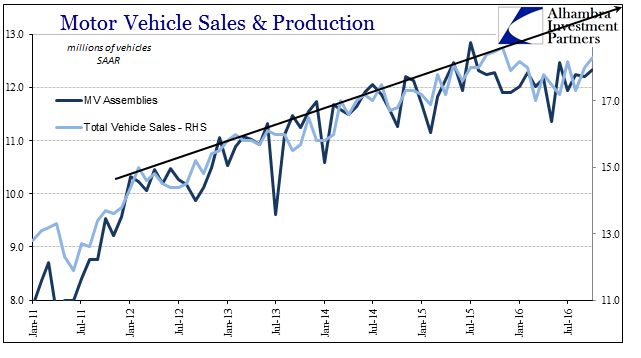

You have to hand it to Ford Motor’s CFO who so far looks to be spot on in terms of both auto sales and production; plateau’s in both to this point. Motor vehicle assemblies, which are part of the IP data release, continued to suggest subdued production, meaning lack of either growth or contraction. At 12.34 million (SAAR) in October, it is practically unchanged since March (which was a slight rebound from declines to end last year) and really a plateau that traces back to the middle of 2015.

That production scaling back has only matched sales leads to the current situation of the inventory overhang, especially in terms of fleet sales and inventory (wholesale). However you analyze the auto sector, it suggests consumers already having no recovery are being squeezed that much more such that even“free money” leasing is no longer a sufficient addition to buying power for an enlarging margin (rising defaults are probably a contributing factor, as well).

This is why “weak but not getting weaker” isn’t to be meant literally. After seven years of low growth, some slightly positive numbers, another year of no growth rather than recession is still functional contraction. Markets betting on a Trump “stimulus” and/or a chastened Fed repentant for its QE-sins should perhaps completely understand the starting point for those hopes (as well as how we have seen this all before). In other words, the economy in 2016 is in much worse shape both in relative terms as well as behind on potential than when QE3 was authored in 2012. QE3 (and 4) did nothing to prevent either the “rising dollar” or the further economic strain that has penetrated far further into the economic base (capex and even the previously invulnerable auto sector).

“Stimulus” didn’t fix it before, and now that it is worse, is there really a basis to believe that different but still “stimulus” will now be effective? It should be pointed out that this most recent infatuation with optimism is still relatively small, perhaps more popular imagination than reality; compared to markets in 2013 that wholeheartedly embraced QE3’s myth, it is practically tiny. That might suggest more realism this time as opposed to that last time, where markets today do appreciate the difference in economy as a base level. In 2013, stocks were up almost 30%; in 2016, stocks rise a few percent and it’s now taken as a great thing. Like continued contraction in IP, it is a relative measure of just how off-track everything has gotten. Then, there was great excitement about good prospects (Bernanke said so) for a full recovery after years of slow growth; now, it seems like a celebration just to hope for possibly something like those years of slow growth.

Stay In Touch