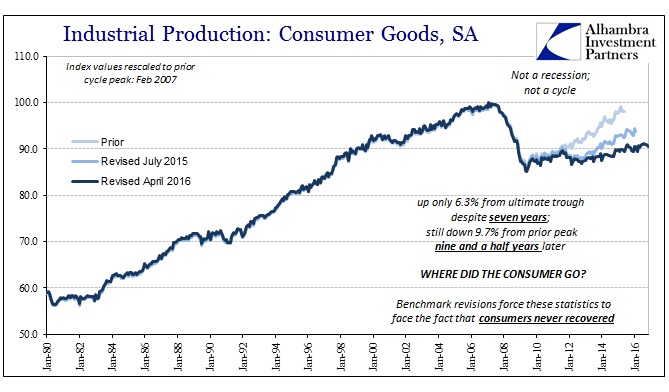

As I wrote earlier, in orthodox economics it is actually possible to declare a depression and a recovery at the same time. The Federal Reserve’s statistic for Industrial Production actually contracted for a fifteenth straight month in November, an occurrence observed only eight other times in just about a century of data. Thus, if IP, as one of the four statistics the NBER uses to date business cycles, is displaying rarified weakness, how is it that the FOMC can vote to raise rates for a second time supposedly on a path to normalization?

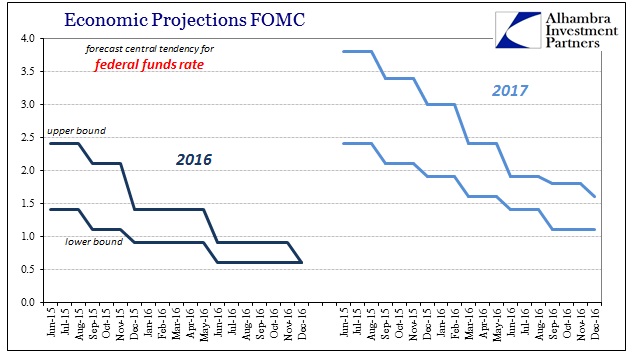

The answer actually lies in just two pieces of data provided also by the Fed, though these are the modeled projections that accompany Fed meetings that fall at the quarterly intervals. The first is similar to the now infamous dots, where the various statistical models the Federal Reserve uses to forecast all the various possibilities replicate what committee members consider when placing those dots. As Monte Carlo simulations, mostly, they produce a statistically significant range where the models expect conditions to be – including for the federal funds rate.

When policymakers in the US began in 2013 to seriously discuss the “exit” from the “emergency” monetary policies that had to that point been continuously applied since the depths of the Great “Recession”, they had in mind the literal interpretation of that word as well as “recovery.” The Fed’s models then were showing that despite years of “unexplained” weakness, there was still every reason to expect it was all just a temporary condition that time and enough “stimulus” would overcome.

As late as June 2015, ferbus and all the rest were expecting the federal funds rate to be between 2.4% and 3.8% by the end of 2017. That level of “normalization” no longer exists as a central tendency, however, since the Fed’s models now suggest that full “exit” would be itself a very low probability tail event. Instead, the central tendency for the federal funds rate has been marked down to a range of just 1.1% to 1.6% for next year. There is a vast difference in those two sets of estimates even though they were produced only a year and a half apart.

We have to understand monetary policy and economics as they see them, not in common sense terms (there is so very little here). The FOMC is guided by several core philosophies, but among them is monetary neutrality. I have seen several definitions for it out there in the internet, but in policy terms it can be quite simple. Money doesn’t define the long run trend, they believe, it can only aid in the short and intermediate terms “aggregate demand.” The long run trend is what the long run trend will be regardless of whatever it is the Fed does or does not do along the way.

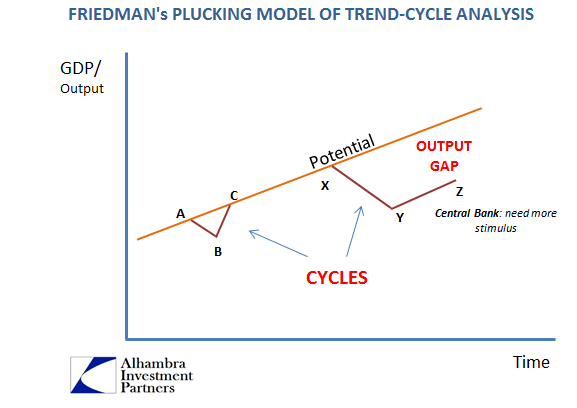

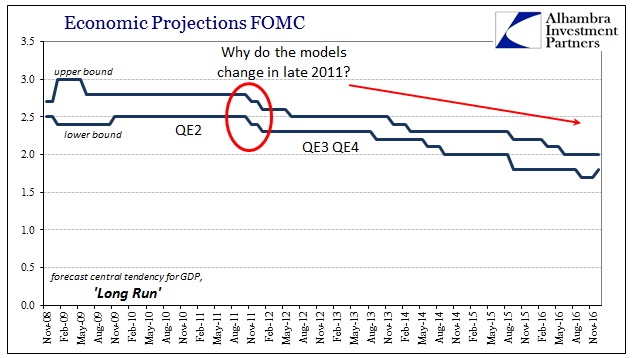

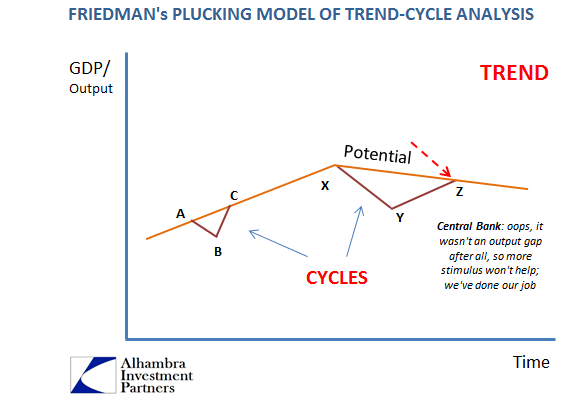

For the past several years, the Fed’s models have been reducing estimates for its version of “trend”, the long run tendency for real GDP growth. Seven years ago at the outset of what was supposed to be full recovery, it was calculated by these regressions that the long run potential was not disturbed by the Great “Recession”, believed to be between 2.5% and 2.8% growth. When Ben Bernanke’s Fed applied a second QE in 2010, it was a response as viewed by these models to an ongoing “output gap”; meaning that the economic trend was still as it was before 2008, only that the current level of “aggregate demand” was short of its cyclical place. Thus, to the Fed, more “stimulus” was required to boost “demand” back up to its precrisis potential.

In late 2011, however, the Fed’s models suddenly start to suggest that long run potential at least as expressed by real GDP was “somehow” declining. The coincidence is beyond curious given the monetary events of late 2011.

Since that time, long run potential has been almost regularly marked down by the Fed’s own mathematics. At an upper bound of just 2% that the math describes now in the latter half of 2016, it doesn’t sound like much difference than the 2.8% upper bound from December 2009, but it is drastic as well as very important in understanding monetary policy in December 2016. What that pattern suggested was increasingly that because immediate GDP growth was not immediately responding to applied “stimulus” the math had to increasingly consider the “supply” side rather than more exclusively “demand.”

The intersection of the modeled path of the long run economic trajectory with that of the dramatically reduced federal funds rate is the Fed essentially declaring that the economy we have today is the best then can do; this, under these orthodox terms, is it. Even if it means Industrial Production declining for fifteen straight months, that is not something the FOMC means any longer to fix. The committee just voted to tell you that it no longer believes that doing so is its job. If we are in a depression, as IP for consumer goods as well as the related denominator for the unemployment rate show, then there is nothing the FOMC can do about it.

After all that happened especially to start this year, monetary policy now views these serious shortfalls as a trend or “supply” problem exclusively that their adherence to monetary neutrality demands they respect. The FOMC threw four QE’s, six full years of ZIRP and a whole lot of promises and talk at the economy, and it just didn’t respond, therefore recovery has been redefined by that lack of response!

What’s even more shocking, to those just now being introduced to these redefinitions, is that these economists still have no idea why it might be a supply/trend deficiency. Because, to them, the reasons haven’t been readily identifiable, they continued to assume for years that it was still a positive output gap situation. Thus, the “global turmoil” recently has provoked something like a circular process of elimination, leaving behind only whispers of Baby Boomers retiring without explaining why they picked 2008 to do so all at once. In other words, if QE didn’t elevate demand, then it must be because demand couldn’t be elevated; therefore supply. The “rising dollar” was the final conclusive proof that demand wasn’t going to suddenly burst upward. Because of that, the projections now for the federal funds rate is converging sharply lower with the central tendency of long run real GDP.

That leaves the second rate hike after all that has happened, and more so what didn’t (2016 was supposed to have been a remarkable economic improvement over 2015), projecting recovery that is in no way faithful to the word – nor, I am sure, what the mainstream is still claiming about it. The FOMC just added its two cents (in the format of idle, useless bank reserves, of course) that it agrees 15 months of contraction in IP is by these orthodox definitions as good as the Fed can make it, the new baseline trend for the US economy. Despite all the wreckage that remains after almost a decade of clearly broken promises, including how malaise has infected so far as to break out in social and political unrest, they are done.

Stay In Touch