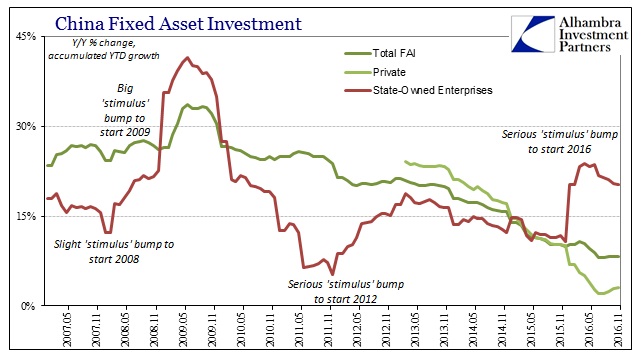

China’s big problem can be succinctly described as where Economics met economics. Capital “E” Economics pushed authorities to over-financialize China in response to the Great “Recession”, which China’s government was only too enthusiastic to do even though its monetary regime at the PBOC better understood what was at the time happening than any of the central bankers in the West still do not today. Following textbook Economics led the Chinese by 2012 to begin to contemplate confrontations with the economics of global malaise.

In 2013, this conflict was a bit simpler, or at least the balance of risks appeared in China’s favor. If we think about the Chinese economy as straddling this duality, relevant government agencies and the officials within them had come to believe that though there would be no global recovery with which to return China to its pre-crisis (eurodollar) “miracle”, the economy of 2013 around the world had at least stabilized after the great uncertainties in 2012. Such a condition would allow for greater emphasis on managing bubbles rather than economy.

The result of this rebalancing was Chinese reform, unveiled in late 2013 and immediately met with financial rejection. I have little doubt that the response in the “dollar” markets was not what they had envisioned, modeled, or perhaps even figured as anything other than a “tail risk.” The reason they were so caught off guard was, in my analysis, that the Chinese misread the conditions of 2013, falling too much in love with the narrative of “reflation” then running wild that was never corroborated by actual monetary revival.

Throughout the balance of 2014 and almost all of 2015, despite all that happened the Chinese were clearly reluctant to shift priorities back to the economy. They applied minimal assistance even though economists (really Economists) all over the world pled with them to go back into the textbook. It wasn’t until January 2016 when conditions became really dicey that authorities finally judged economic risks as more than bubble risks.

The Chinese and global economy seemingly stabilized all over again in later 2016, so we are supposed to believe that China is back to bubbles again as if they had learned nothing from 2013.

President Xi Jinping and his top economic policy lieutenants adjourned their annual planning conference Friday with a vow to safeguard the financial system and deflate asset bubbles. Maintaining stability and making progress on supply-side reform will be key 2017 themes, they said in a statement issued after the three-day Central Economic Work Conference.

“Policy makers are making clear that they’re determined to clamp down on speculation and will keep doing so next year,” said Wen Bin, chief research analyst at China Minsheng Banking Corp. in Beijing. “It’s very important to deflate the property bubble.”

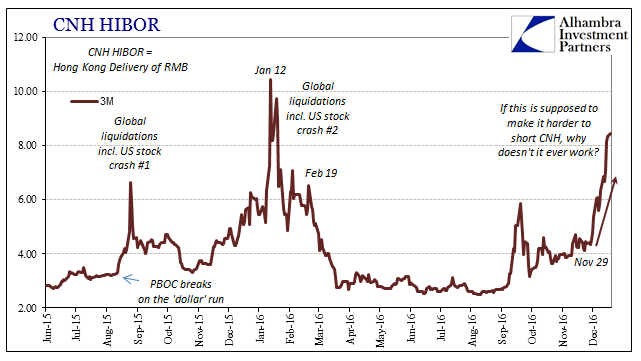

Ever since money market reform (2a7) passed into benign history with money markets more a mess today than during it, I have been wondering what excuse would take its place. The FOMC’s “rate hike” is certainly a candidate, though some care will be necessary because “necessary tightening” in the mainstream does not result in illiquid turmoil. The Chinese central bank going back to bubble popping just might be a more pliable pretext.

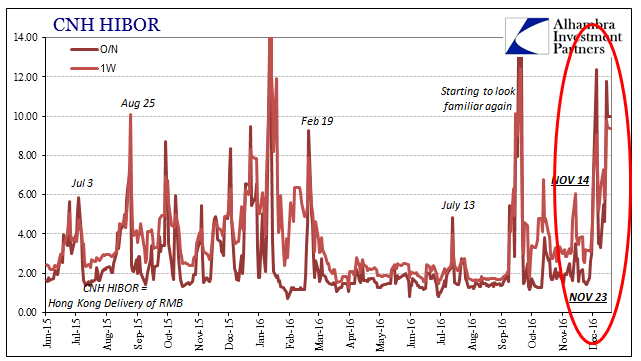

The overnight HIBOR rate (CNH) was 10% for the second straight day today, with the benchmark 3-month HIBOR (CNH) rate rising to 8.454%, the highest since the worst in January. This spike in money rates is almost always attributed to fighting “speculators” still, even though it doesn’t seem to ever work.

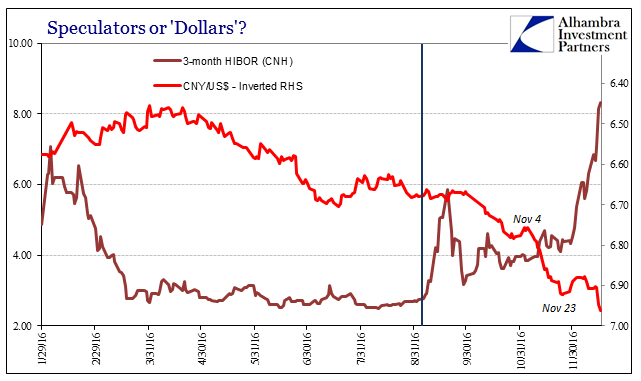

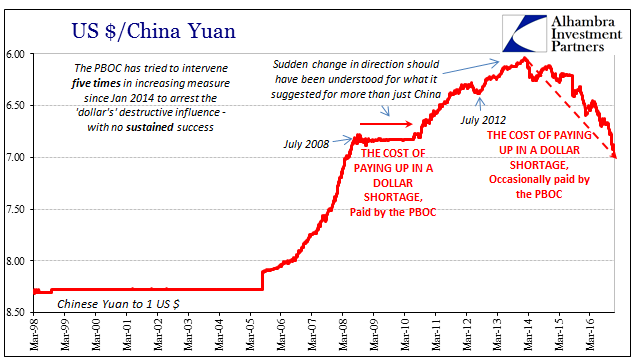

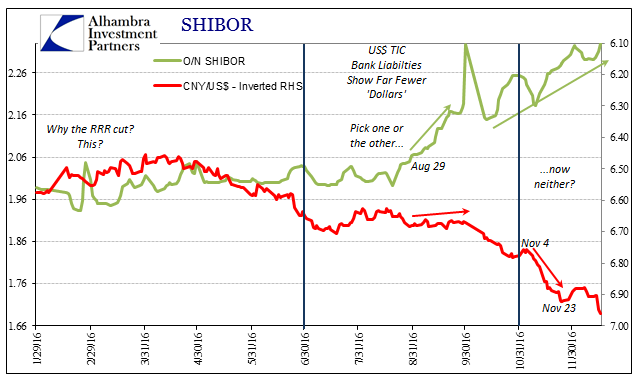

When Chinese money rates started to rise in early September, the CNY (onshore) exchange rate was steady around 6.67 or 6.68. As both HIBOR and SHIBOR rates kept rising, spiking the former case, CNY remained flat if not almost fixed or pegged again. That would seem to be in keeping with the “speculator” narrative, especially as those weeks were in close proximity to the yuan being upgraded in the IMF catalog to a “reserve currency.”

Though the mid-September surge in HIBOR abated, overall money rates in Hong Kong (including, importantly, for Hong Kong dollars) kept rising overall even as CNY dropped precipitously. It could be said that Chinese authorities were using HIBOR on an upward trajectory to make sure that CNY didn’t fall farther than it “should” have, but such an argument would amount to yet another “jobs saved” fallacy. What I see clearly on the chart above is not attempted control, but instead growing systemic illiquidity forcing a greater loss of it.

“Something” changed over the summer, where prior during the spring though CNY fell right on schedule in May and June, money rates in China were very stable – even HIBOR. It was during this iteration of the “ticking clock” that suddenly saw the proliferation of “CNY doesn’t matter” articles and proclamations. So much for those.

Even if we were to stipulate that the HIBOR rates are a reflection of intentional Chinese monetary policy against “speculators”, at over 8% for the 3-month rate we would still have to conclude that it was at the very least an increasingly desperate as well as unsuccessful one. That isn’t what happened, of course, instead the media and the mainstream are attempting to make sense of what we see here by reverse engineering to how it could possibly be nothing of concern (like 2a7, which was always ex hoc ergo propter hoc fallacy). They see falling currency and rising money rates and conclude it must be central bank policy to keep the currency from falling even farther, and for bubbles to be less bubbly.

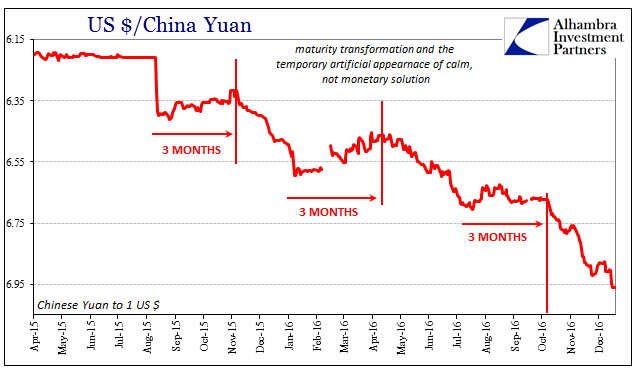

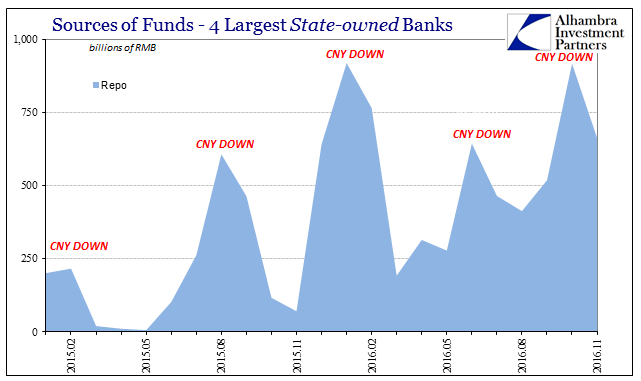

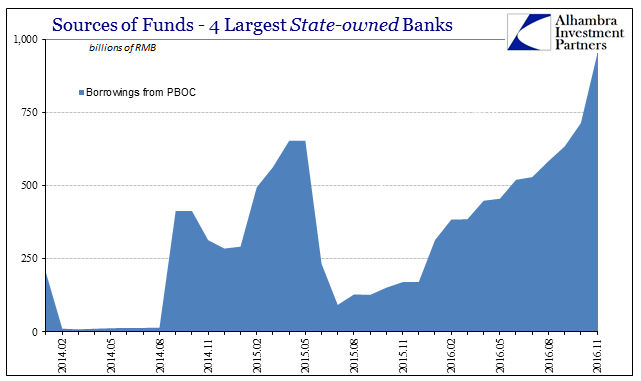

The Chinese have never given up their bubble risks, including this year where economic risks returned to the forefront. Even monetary “stimulus” has been different than before on just that account, channeled increasingly in “targeted” ways through the largest banks. If there is a “war on speculators” in China, it is through the PSL, MLF, and SLF conduits where the PBOC routs RMB funding through the big banks almost exclusively.

And what we find in November is those Big 4 state-owned banks dropping out of the repo market as repo rates jumped (on broad illiquidity). They replaced that funding with direct borrowings from the PBOC, but it wasn’t sufficient to maintain the prior month’s balances when the PBOC was clearly more active. And if it was insufficient overall for the Big 4, what might have been left for the rest of the RMB market? We don’t have to guess; we can see it in the SHIBOR and HIBOR rates.

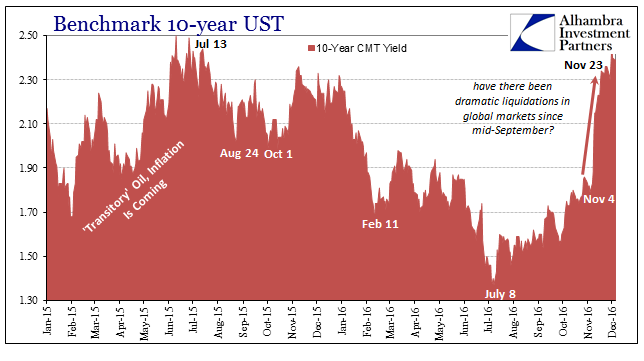

It was the middle of November, of course, where the global bond liquidation hit, also where CNY fell farthest and fastest.

Again, in October the PBOC had made sure the Big 4 were plenty stocked with “spare” RMB – and thus able to transfer additional liquidity in (it is assumed) more responsible fashion than the prior regime of adding RMB directly to money markets. To believe that it was offshore speculators therefore at the center of a global bond market rout makes no sense. The PBOC didn’t change their liquidity tendencies drastically from October to November because of Hong Kong CNH shorts, thus triggering a worldwide liquidity problem to which bonds reacted most violently, as there is only one “currency” that could have possibly accomplished such a feat and account for the whole thing.

That has been the one constant throughout the past few years of CNY Down = Bad, where when CNY is falling fastest and most out of control it is doing so because the PBOC is itself restrained (“ticking clock”) from providing “dollars” (“selling UST’s”) and therefore not providing RMB. This reciprocation internal from external is actually a requirement of the PBOC’s balance sheet where every intervention comes with tradeoffs and costs. The “dollar” was especially harsh in November, not just for global bonds but also the Chinese central bank.

Though it increasingly appears as if the media is trying its best to describe all this like it was 2013, I am not convinced the Chinese are in agreement with that view. Economic risks are greater now than they were then, even if we accept the idea that the global economy has stabilized because it would be doing so at an even lower state. Obviously, financial risks are as much a concern, including bubbles. In other words, both China and Economists missed the “dollar” in their 2013 rush to declare global recovery. Three years later, I would argue that it is only Economists making the same mistake, with the media trying very hard to make it seem as if the PBOC hasn’t learned, either.

Stay In Touch