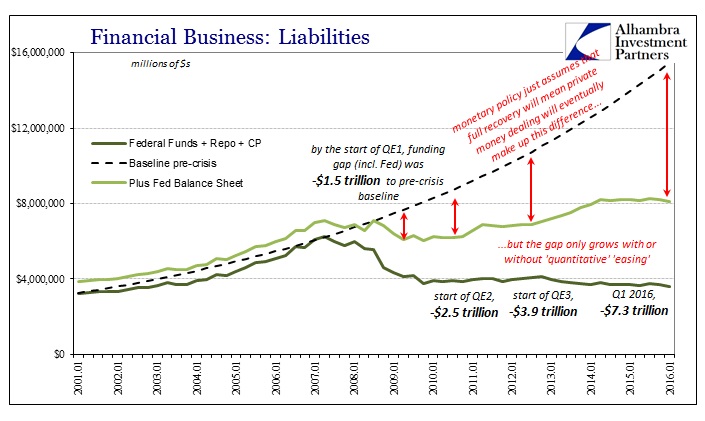

There are usually ceteris paribus assumptions lurking behind every mistaken impression in economics, including monetary economics. If Central Bank X does Y, where Y is a plus sign it is believed to be “accommodation” or “loosening.” Rarely if ever is there an account of money outside of this condition, except in only the most extreme of circumstances. In the past, that would have been any activity no matter how small at the Federal Reserve’s Discount Window (before it was changed), or the belated and stunted dollar swap lines with foreign central banks.

Quantitative easing was just such a mistake, where policymakers and economists (redundant) wrongfully asserted it was a positive monetary contribution – four times. Removing ceteris paribus from that assumption has the effect of rendering QE as at the very least quantitatively insufficient in total across all four applications, while more important being only one narrow form of wholesale money into which the entire global market was/is starved of all forms.

There has been a similar proposition embedded within commentary related to Chinese monetary conditions. If, for example, the PBOC reduces the rate of required reserves (RRR) for Chinese banks it is by and large assumed to be a further “accommodation.” That is true only in the ceteris paribus sense. As discussed last week, since 2011 that just hasn’t been the case. A reduction in the RRR is, as QE actually was, an ex post facto reaction to private monetary events. The Chinese starting in February 2015 reduced the RRR as the “dollar” shortage directly impacted China’s money supply. It was intended to be a neutral policy action, at best.

That has been the direct claim of the Chinese central bank throughout, and for once we can take them at their word. Monetary policy in China has been since 2011 about one task only – to fill any created funding gaps created by what are called “capital outflows” in the mainstream but are really this unrelenting and variable “dollar shortage.” If the RRR is reduced, it is because the PBOC has judged “dollar” problems sufficiently disruptive so as to merit an increasing RMB policy response in order to maintain that neutral position.

The format of the PBOC replies has not been limited to RRR cuts, nor even rate cuts to its main policy levers. Starting in 2013, the central bank has been adding, and using, several additional tools in order to more precisely manage whatever intended policy stance; neutral or otherwise. The Standing Lending Facility (SLF) was inaugurated in early 2013 and used pretty extensively almost straight away – 2013 was, if you recall, not the best year for Chinese monetary conditions. The SLF is akin to the Fed’s Discount Window.

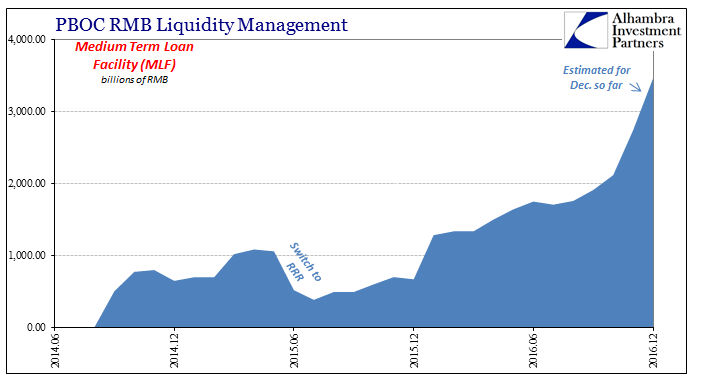

The Medium Term Loan (or Lending) Facility (MLF) was implemented in September 2014 as a method for “targeting” institutions directly involved in lending capacities, offering three-month tenders of RMB to commercial banks. Like the SLF, it was used almost immediately from its inception in the later months of 2014 as the “rising dollar” amplified the “dollar” problem that had been escalating in pieces ever since 2011. A big piece of “dollar” decay came in early 2014 when suddenly the CNY exchange rate lurched downward against “all” expectations.

At the time, the mainstream was hugely confused, especially in March 2014 when the PBOC unexpectedly widened the daily currency trading band. Conventional “wisdom” eventually settled on speculators (it’s always speculators, rather “speculators”), where China’s central bank surely must’ve been addressing those trying to make a profit from CNY appreciating too quickly. The more obvious answer was impossible in this convention because QE, ceteris paribus, meant a dollar shortage (let alone a “dollar” shortage) was impossible.

I wrote instead in March 2014:

What all this data shows, as opposed to conjecture about the supernatural powers of central banks, is that yuan’s devaluation may be directly tied to dollar shortages. In fact, as I argue here, it is far more plausible that a dollar shortage (showing up as a rising dollar, or depreciating yuan) is forcing the PBOC to allow a wider band in order that Chinese banks can more “aggressively” obtain dollars they desperately need. Worse than that, the PBOC itself cannot meet that need with its own “reserve” actions without further upsetting the entire fragile system.

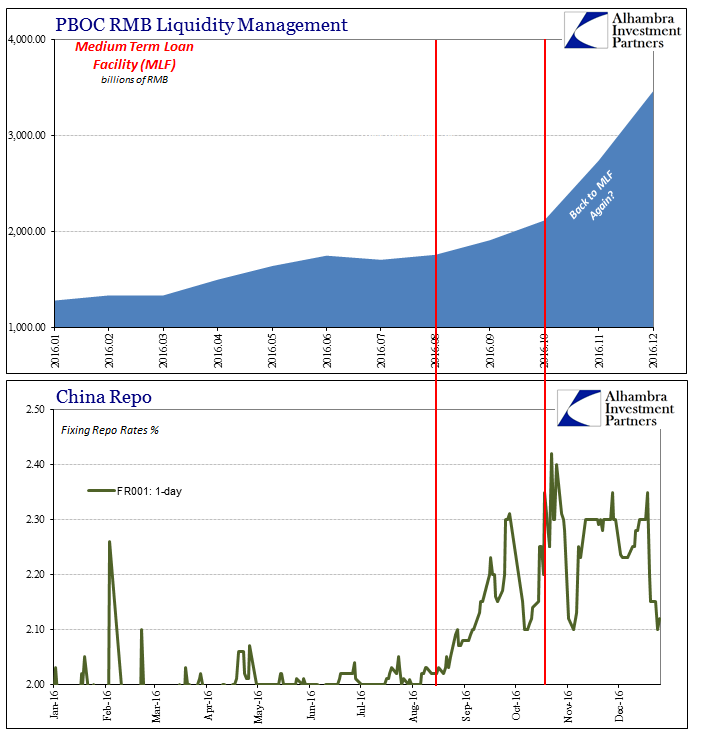

As the “dollar” vise tightened, the PBOC began to more heavily use its new tools, especially the Pledged Supplementary Lending (PSL) Facility and the MLF. By the end of 2014, the MLF had an outstanding balance of almost RMB 700 billion (with another RMB 1 trillion committed via the PSL to China Development Bank).

For reasons yet to be stated, the PBOC abruptly changed in February 2015. On February 4, 2015, Chinese officials announced the central bank would, in fact, be cutting the RRR effective the next day (no waiting period). It was the first RRR change since 2012. There was a parallel large increase in MLF outstanding into March, but after three months (the typical MLF term) these balances were drawn down by more than half. The PBOC had for a second time cut the RRR in April 2015, clearly shifting its overall neutral stance to its more customary tool.

This was not completely unexpected, as the new liquidity management methods were meant for liquidity management rather than long-term use, as any central bank would have it. Standard practice called for standard policies to take up the effort given enough time; the hard part is always trying to figure what is “enough time.” This common perception was voiced from the very start of the experiments, as this quote from November 2014 illustrates.

“It shows the central bank is very reluctant to loosen monetary policy, but it has to reduce financing costs for end borrowers,” said Guan Qingyou, chief macro-economic researcher with Minsheng Securities Co. in Beijing. “It doesn’t mean the new tools can replace traditional tools forever.”

The PBOC would stick with the RRR (as well as traditional rate cuts) all through the worst of it into February 2016. The last reduction in required reserves was effective March 1 of this year. This traditional approach was augmented by additional MLF funding made available in January during the absolute worst, as Chinese money markets (especially offshore) were quite unsettled.

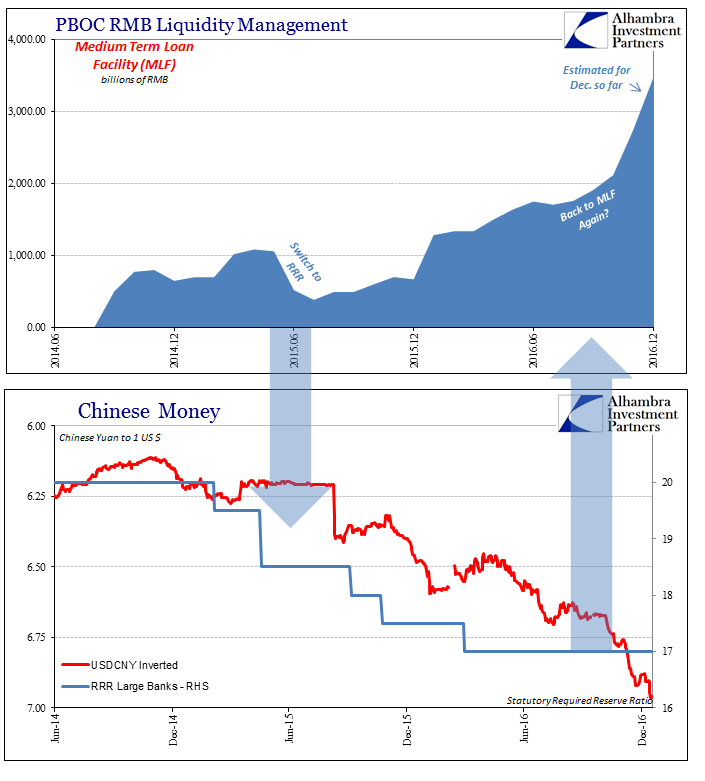

Rather than being drawn back down again three months after January, however, MLF usage has only increased though the RRR rate remains still fixed at the March 1 mandate. At RMB 1.3 trillion at the end of March 2016, three months forward the total balance was RMB 1.7 trillion (during that time CNY was falling again). Where in August total MLF borrowings were RMB 1.75 trillion, the total at the end of November was an astonishing RMB 2.73 trillion; and it is currently estimated (AIP calculations from incomplete PBOC figures) to be RMB 3.46 trillion, or nearly double August. That’s an enormous amount of RMB in a short amount of time just to keep a neutral monetary stance.

The fact that MLF borrowings have skyrocketed since August should be already familiar to anyone paying the slightest attention to Chinese money markets. The chain of causation is thus established, especially from a neutral position. The MLF, like the RRR and other traditional tools, is and has been reactive to external monetary circumstances, not proactive “loosening” or “stimulus.” The more the PBOC does through any of these channels, the more we can reasonably assume they feel they have to do to keep up with the variability in the “dollar” gap or shortage.

The fact that the central bank has also leaned almost exclusively on the MLF in later 2016 rather than the RRR is likewise significant. There are tradeoffs to any purpose or method, and we have to assume that the PBOC has judged the MLF (as well as the SLF) the most effective (or least harmful) means of tackling the escalating funding problem.

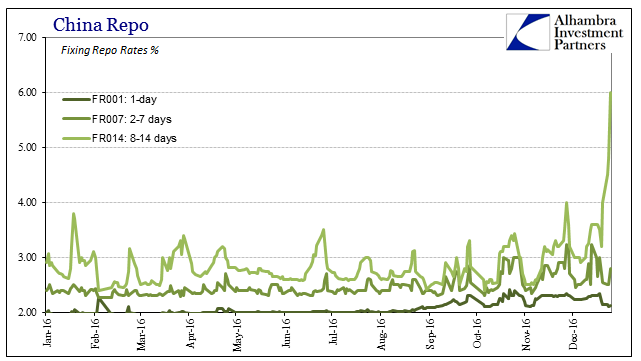

Just today the repo rate (14-day) fixed at 6%. The PBOC is stuffing trillions in RMB through the MLF just to keep repo (and other money market) rates from getting further out of hand. It is clearly being overwhelmed by “something” far outside the academic, media drawn lines of ceteris paribus.

Such drastic changes and blown expectations immediately call our attention to the “dollar.” Why has the PBOC sacrificed its post-August 2015 liquidity regime to stick CNY at around 6.68 to 6.685 – not even 6.70 anymore? The fact that Chinese money markets are now such a huge and obvious mess can only mean that whatever it is about the “dollar” that caused this shift has been judged as the greater of these two “evils.”

No matter which way you reduce these factors, they always come back to the same thing. The mainstream is filled with stories of stoic Chinese central bankers calmly disassociating speculators from the global recovery. The truth is far more sinister and troubling, that of a central bank increasingly unable to manage even a neutral stance despite trillions in assumed liquidity additions. That description applies universally and globally, of course, across the whole of this downward side of the eurodollar dating back now almost a decade. The Chinese are no exception, only the latest to be fully engulfed.

If it hasn’t already, global dreams of reflation will eventually have to reckon with these forces, just as past episodes did.

Stay In Touch