We have to start with the understanding that Alvin Hansen was completely wrong. Hansen was the American economist who in the late 1930’s worried that the Great Depression was not just a severe, catastrophic event but a permanent alteration in the economic landscape. For those who took him seriously, it was a perpetual midnight setting against robust growth that had been the baseline for the globe since practically the Renaissance and the institution of the lessons of the Age of Enlightenment. This was “secular stagnation”, whereby without population growth, innovation, or territorial expansion there was, in Hansen’s view, nothing to drive economic fortunes, and thus create the reference line trend of rising living standards.

All of those factors are difficult if not impossible to foresee or measure. Hansen could not have known about the Baby Boom that was less than a decade into the future, nor the revolutionary aspects of the transitor which had been patented in one form in 1926 but in its 1947 arrangement would lead to eventually to the computer and internet revolution. That is the point; what drives economic growth are not those things that Hansen described but something even more basic that becomes in parts those aspects – the human desire for “more.”

Secular stagnation disappeared for decades because it was a loss of faith in humanity soon disproved by the strong urge for progress often despite ourselves (or “our” policies). It is by no means a straight line, however, and in those peaks and valleys “we” can be fooled into thinking either the peaks or, as now, the valleys are permanent introductions upon the landscape of global potential. To believe in secular stagnation is, in essence, to lose faith in humanity, an oftentimes easy thing to do but no less ridiculous on its face (just as “permanent plateau of prosperity” is to assign far too much faith).

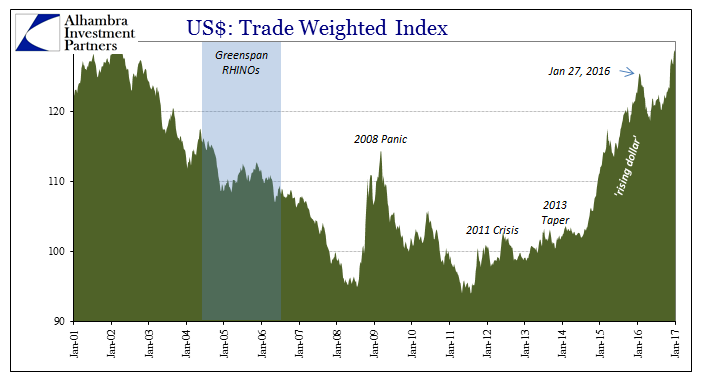

In one of the more quiet aspects of Economics’ (capital “E”) reconciliation with the global effects of the “rising dollar” is an embrace of the possibility for secular stagnation. And why not? If you are a central banker it is almost like a “get of jail free card”, a way of saying that monetary policy didn’t fail even though it obviously didn’t succeed.

The Banque du France held a small conference on the topic yesterday titled Secular Stagnation and Growth Measurement. ECB board member Peter Praet participated in a panel discussion about “How to deal with potential secular stagnation”, but no remarks were prepared nor discussion recorded. Overall, there was very little notice at all, and even less publicity.

Nonetheless, Francois Villeroy de Galhau’s speech has been made available, a review of the situation from the perspective of the central banker.

Nevertheless, this risk, popularized again recently by Larry Summers, is a matter of concern for central bankers. Why? Because a persistent slowdown in trend output growth could make the economy more vulnerable to shocks that push the natural interest rate below the effective lower bound. Whether secular or lasting for many years, very slow growth and inflation also challenge the efficacy of conventional monetary policy tools.

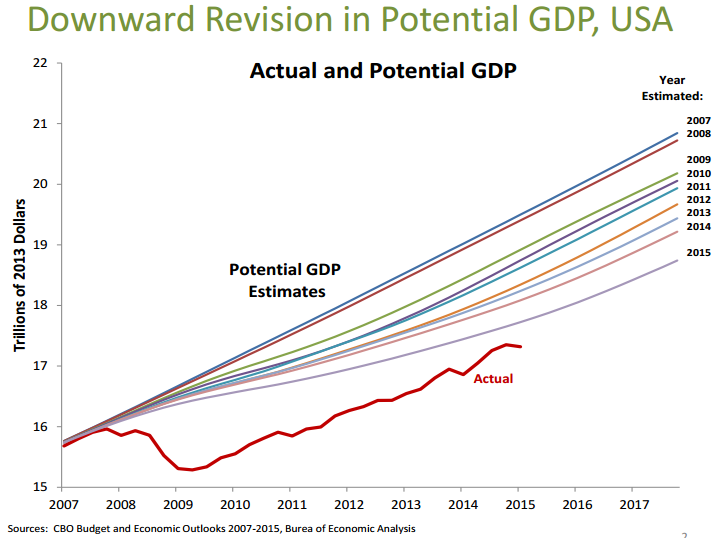

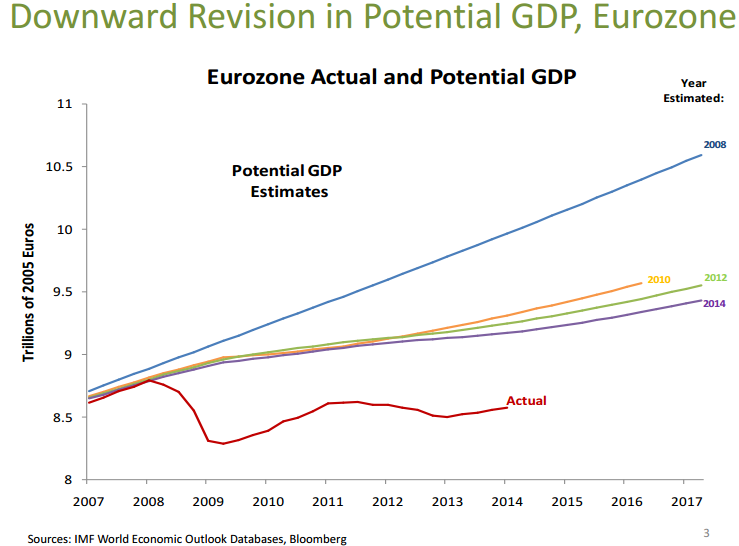

On the first part, there is no doubt, a fact that global QE’s in abundance could not change. The presentation materials accompanying the speech include what is truly a damning indictment, but one that seems unable to be appreciated by central bankers given their obvious blindspot.

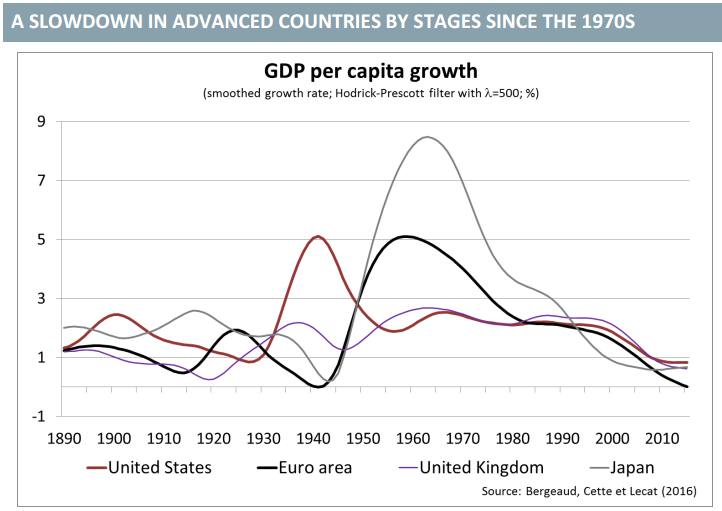

For the first time in modern world history, GDP per capita growth has become synchronized in the worst possible way. There have been economic problems before, but never before so sharp and uniform. Economists and policymakers have no answers for this, which isn’t surprising since it already by its existence questions the competence of these economists and policymakers.

We know without reservation that these “experts” had no idea what they were doing because they kept doing things over and over that would never have worked under these conditions. Thus, the relevant question to ask first is not how did this happen, but rather why are we letting people who didn’t see this coming try to figure out why they didn’t see this coming? It’s not as if there weren’t warnings, and I don’t mean outright global panic in 2008.

The latter part of the 1990’s was a period of constant monetary imbalance and allusion to “something” within the sphere of central bank dominion. Alan Greenspan before the fame of his briefcase was often unusually concerned about all this. Even after the dot-com bust, the inability of central banks to operate within their mandates was a bright flashing warning (Greenspan’s 17 rate hikes that appeared unable to disturb in the slightest inflation or monetary conditions where rate hikes were thought to be powerful if not the only instruments of influence). And yet, nothing; no scurrying concern, no triggered response of intellectual mediation let alone mechanical inferences. Even after the great crash, central bankers proceeded as if the Great “Recession” were one, big, severe recession.

All of the relevant data and estimations show that it wasn’t, and do so conclusively. That is why this explanation is being explored more seriously. The IMF held a similarly quiet conference on “secular stagnation” all the way back in June 2015. The keynote speaker was none other than Larry Summers, who has more than anyone else revived Hansen’s blackened view of the modern human condition (and the capitalist engine that made it possible). His presentation was still dispositive that “something” is very wrong, but despite its cross-border infection is not given a suitable reasoning.

How could economists, really Economists, have not the slightest inkling as to what was coming? Unfortunately, that question can be applied to more than just the aftermath of the Great “Recession”, as it relates to that dislocation itself. And that means we are back within the realm of the monetary, the one aspect of all this that policymakers especially refuse to consider. It is almost a tautology of circular reasoning that prevents it: central bankers assume and consider money only in the closed system form, therefore a globally unified problem can only be considered outside of money.

And yet, that is the one place where all this should begin. After all, prior to 2008 it was claimed by every central banker that “deflation”, depression, and even panic were practically impossible in the modern sense. Ben Bernanke told Milton Friedman on his 90th birthday that the Fed was responsible for the Great Crash 1929-33 and that the Fed would never do it again; but here we are, with policymakers all over the world very discreetly discussing how it could be that it did happen all over again. The reason they have dug up poor old Alvin Hansen once more is that the global economy has fallen into the same condition as the 1930’s – and have no interest in being blamed for it.

If central bankers were wrong about money going all the way back to at least the 1990’s (and really a great deal further back) it stands to reason they could be wrong about it as the possible trigger for secular stagnation, depression, or whatever term one might deploy in accurate description. The stakes are enormous, as de Galhau said yesterday, “And beyond central banking concerns, they [very slow growth and inflation] can also alter the functioning of our social models.” Thus, it is incredible that these same people who presided over its “unexpected” arrival will now be allowed to describe that arrival and therefore tell us they have “scientifically” determined that it is enduring, maybe even perpetual, damning the fate of the world to the far greater possibility of all the same worst case scenarios.

Alvin Hansen was wrong because what ailed the world, indeed what unified the world in global depression, was not lack of population, innovation, or territory but rather more simple than all that. The Great Depression, the preceding decades, as well as its aftermath were all characterized first and foremost by monetary instability. Bretton Woods wasn’t even a good solution, let alone a sustainable one (it functionally ended after only 16 years), but it was enough to allow global growth to return all over again. No less than John Maynard Keynes, one of the fathers of Bretton Woods, and no great fan of hard currency, knew the problem wasn’t secular stagnation but monetary policies that made no sense for anyone anywhere.

The problem in the 21st century is that money itself no longer even makes sense. It has taken officials almost ten years to come to terms with the consequences, but even now they will still doom us to Hansen’s dark vision if they are allowed to define humanity down to such an inappropriate nub. In other words, they see the great problem as us; from the modern, wholesale money view, we see very clearly it is instead them. And we didn’t need a decade of depression just to consider the possibility.

Stay In Touch