From the outside, it appears as if Wall Street operates like a bureaucracy. There is an enormous amount of paperwork, endless committees who conduct endless meetings, and layers of management supposedly managing the movement of that paperwork as well as the meetings of those committees. The idea is simple enough, to make it appear as if there is tremendous weight to the process especially when considering big things. That is what banking is, after all, an image.

This is not to say that the whole works is strictly for show, to fool the rubes into complacency while the Cowboy mentality actually prevails behind the veil. Overall, there is simply a balance that is struck because the process is imperfect, and cannot be anything other than that. If the Cowboys (or BSD’s, of Salomon fame) can make a ton of money for the bank, then all the rest is mere formality; if they can’t, then formerly rising stars have a lot of people to answer to. Bankers are human and operate as human beings with biases and perceptions.

That was one of the great ironies about LTCM. It introduced math in a way that actually preyed upon biases. The allure of math is its scientific senses, the way in which it is pitched under objectivity, as if great formulas and complex equations can see the future because there they have no emotion or individuality. In truth, this financial math is sleight of hand, a magic trick performed by the best of illusionists. In the middle 1990’s, that was Robert Merton and Myron Scholes.

With those two names attached, who was going to argue against LTCM? As I wrote about two years ago in June 2015 just before “global turmoil”, the lessons never stay learned:

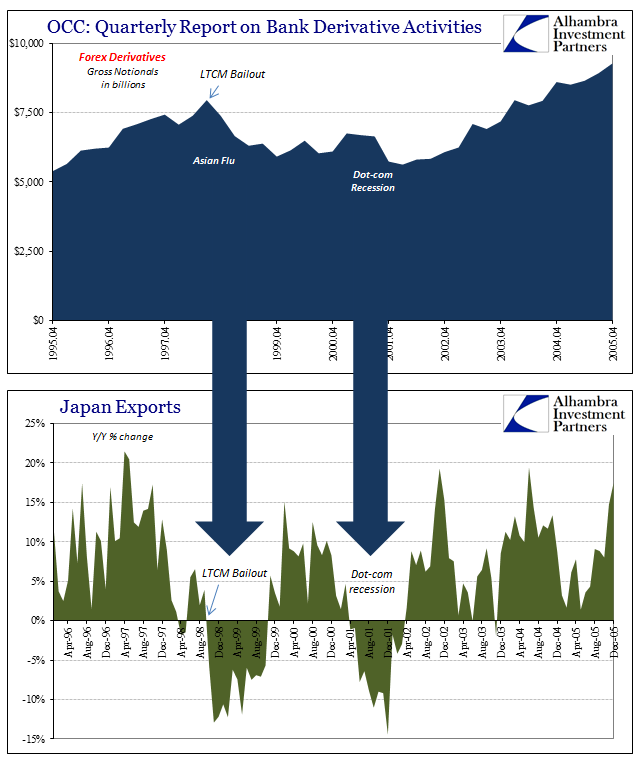

If Robert Merton and Myron Scholes tell you that they have discovered a way to book huge returns with little risk, there isn’t so much pushback without fear of being embarrassed at doing so. That seems to have been the case all over Wall Street, as LTCM amassed huge leverage from just about every foreign and domestic “dollar” bank as existed. The firm started out with $1 billion in equity financing in March 1994, and by the end of 1997 that had grown to about $4 billion. That was the slim foundation for a total portfolio of more than $120 billion! By way of comparison, JP Morgan Chase’s total assets listed in its March 1998 10-K were $365 billion. Off balance sheet, notional derivative exposure was thought to be about $1.45 trillion.

LTCM was given trades all over NYC often repo and often at zero initial margin, so good was their illusion. The FOMC meetings that considered the bailout of LTCM were often marked by comments expressing disbelief as to how a firm nobody (in official circles) had heard of one day was a threat to the global financial system the next. As Alan Greenspan asked of the Fed staff making a presentation on the matter, “Is it just that the lenders were dazzled by the people at LTCM and did not take a close look?”

The real problem of the LTCM affair wasn’t just that Wall Street didn’t understand them, or that regulators didn’t understand them, or that monetary policymakers didn’t understand them, it was that despite nobody being able to understand much of anything it still became the dominant business model for the entire industry anyway. Rather than learn and appreciate the dangers of operating on loose margins and complex strategies solely dependent upon elegant math still tethered to human assumptions and frailties, firms all over the world set out instead to find a way to be a better LTCM without ever asking if it was even possible. As I wrote then, the Asian flu was simply a rehearsal for 2008 and more importantly its aftermath.

Policymakers, in particular, remained confused and never truly figured out what had happened, but because of the dot-com bubble positively affecting much of the developed world, the whole Asian flu seemed like a foreign affair just as it was officially treated. Greenspan was given a pass largely because economists pointed fingers at Thailand and Indonesia for not having already joined the groupthink about “floating currencies” and huge stockpiles of “reserves.” Though the US economy did experience a near-recession in 1998, the only part of the so-called West fully embroiled in it all was Japan.

It is in these specific episodes where we can calibrate our interpretations for the behavior of complex monetary components like FX derivatives, especially necessary given that numbers like gross notionals are only rough proxies that at best can provide small insight into bank balance sheet intentions. The bailout of LTCM did not cause the Asian flu, but it made it what was already a big problem that much worse. And of course, LTCM’s final demise was but the last step in its global disruption, as it had already spread a great deal of the initial financial problems worldwide. That is what is truly missing in official policy positions, how these forms of eurodollar contacts are often if not always the very agent of contagion that escapes orthodox “understanding.”

For much of Asia, the first half of 1999 was incredibly difficult. And in what was a preview of what has become commonplace, the Bank of Japan in February 1999 introduced the world to ZIRP in an effort to “stimulate” their way out of a negative condition far beyond its ability to do so. Central banks do not sit upon the monetary apex.

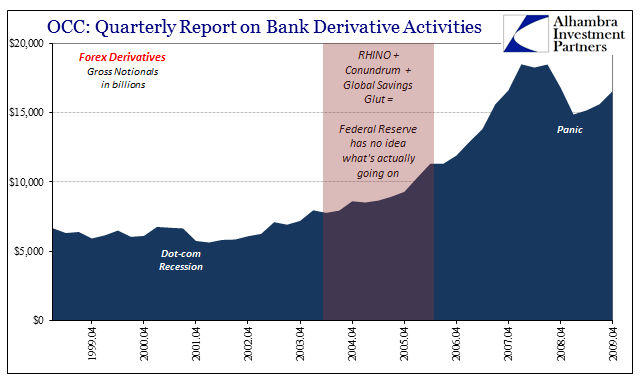

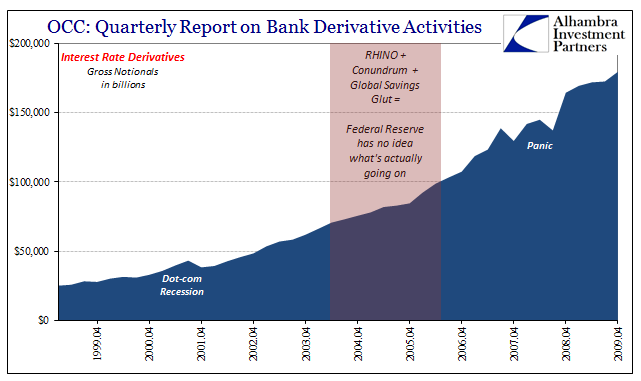

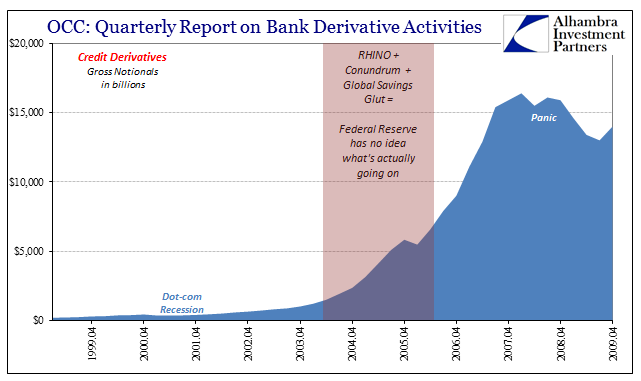

Because monetary policy doesn’t consider any of these eurodollar aspects to be anything other than complex investments, not only did they miss the Asian flu but they mishandled the dot-coms and then were completely lost in the middle 2000’s. Alan Greenspan “raised rates” starting in June 2004 and yet practically nothing of monetary importance actually seemed to notice (which is why I call it RHINO, Rate Hike In Name Only). In what was an especially embarrassing final act, the former “maestro” was forced to elicit absurdities to try to explain these massive monetary disparities (“global savings glut”, interest rate “conundrum”). In reality, the more complex parts of the global money system were operating just as LTCM had totally outside official purview without much input at all from the Federal Reserve.

That was perhaps most evident and most dangerous in the form of credit default swaps, the most potent and refined of the math-as-money formats particularly when used in “regulatory relief” as actual and functional balance sheet leverage.

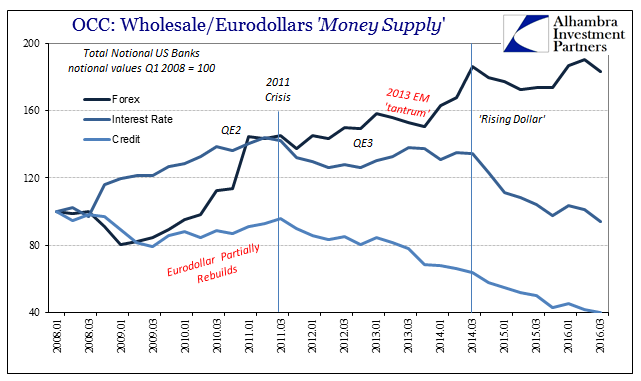

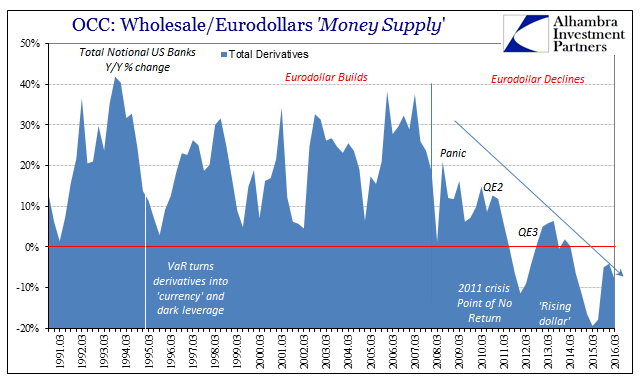

The behavior of derivatives and eurodollar bank books is instructive in more ways than just revealing the naked ignorance of economists and official “experts.” It demonstrates another way in which we can calibrate our interpretations – evolution. The derivative system of the middle 2000’s was clearly different than it had been in the 1990’s, largely driven up to LTCM by forex contracts and trading. Interest rate derivatives increased in notional size as well as relative importance because the eurodollar-driven bubbles were by then more credit (and mortgage) related. You could even make a case, as I might, that the Asian flu and the subsequent retreat in FX was instrumental in the ultimate shape of the housing bubble (without FX and purely trade financing, eurodollar vastness had to turn inward to mortgages and non-trade finance).

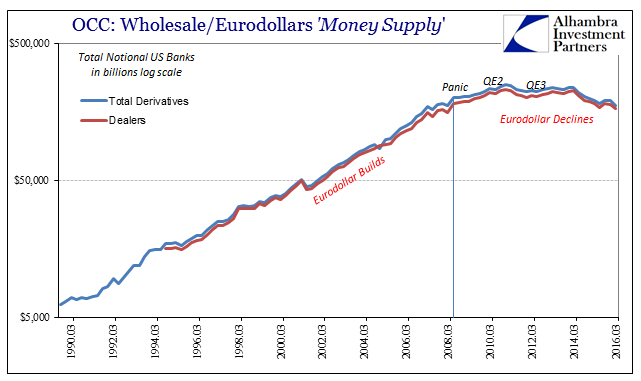

The eurodollar in the aftermath of the 2008 panic has likewise evolved again, several times. In the immediate period right after the worst of it, interest rate swap trading rose sharply first. Forex derivatives made a comeback around QE2, while even credit derivatives staged a mild comeback up to the middle of 2011. It was during this period where the recovery appeared its most realistic (though still “off”).

The 2011 crisis, as we see everywhere around the world, changed everything again. In derivative terms, credit default swap books were simply run off and are still so; interest rate swaps peaked and began a gentle decline; but forex derivatives emerged as the marginal source of limited capacity once more, and thus likely accounting for the increasing currency-driven nature of what has followed.

Like the 2011 crisis, however, the “rising dollar” that emerged in the middle of 2014 changed everything all over again. Banks began to retreat from their interest rate books with greater emphasis, while forex capacity completely stalled, leaving the global system without any additional capacity in any of the major forms of it. The global economic and financial conditions of the past few years reflect that interpretation very well, particularly in currency terms.

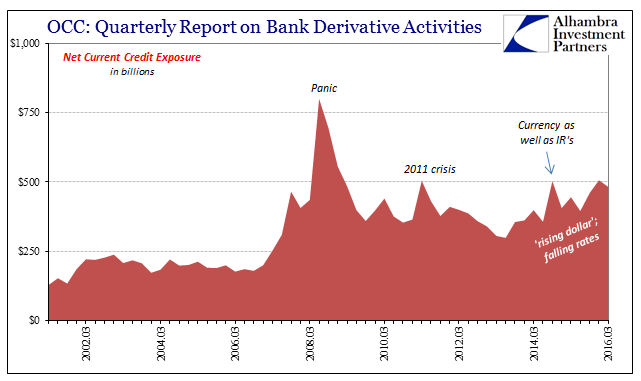

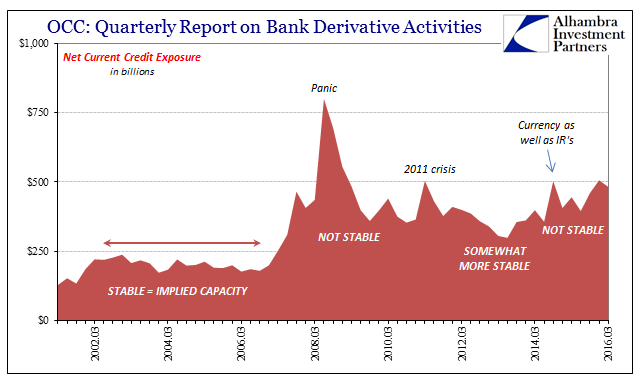

Last month in anticipation of the OCC’s Q3 2016 update, I examined some of the possible reasons why forex derivatives would behave in this manner. Primary among them was inferred volatility in the currency space (especially Q1 2015 when CNY, RUB, and CHF were all suffering dramatic and erratic movements). One of the metrics the OCC provides to try to distill dealer risk is through something called Net Current Credit Exposure (you can review here what I wrote then for a primer on this figure and what it means).

NCCE is typically driven by interest rates, and largely because interest rate swaps form the largest portion of derivative books. Lower interest rates increase NCCE, but in Q1 2015 that wasn’t the only cause as currency volatility was also a prime factor.

Because of the way NCCE is calculated, the remainder after gross positive fair values are netted by either collateral or offsetting positions, a rise in NCCE for whatever reason is a rough proxy for dealers being able or unable to lay off risk (and thus of systemic capacity).

With interest rates rising in Q3, I had expected that NCCE would have declined significantly as the “reflation” trade began to take hold in bond markets. The updated estimates for Q3, however, show very little change in overall NCCE for the quarter. From $502 billion in Q2, NCCE retreated only to $482 billion. Given the behavior of interest rates, from that small change we can infer a great deal of currency volatility, thus risk, thus dealer reluctance (because they could not find a reasonable way to offset those risks).

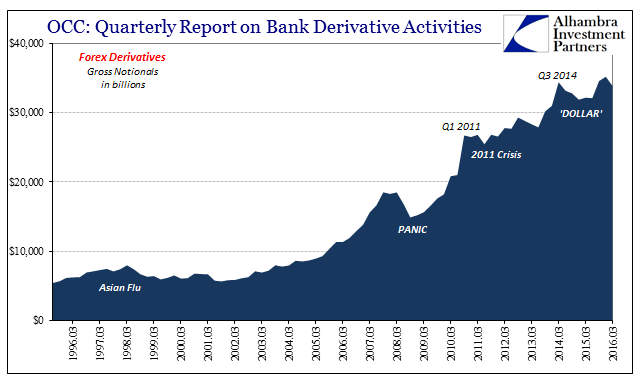

That seemed to have been the case, as total forex gross notionals declined again in Q3, to $33.9 trillion from $35.2 trillion. It does appear consistent with the eurodollar conditions we observed in Q3, which for many regions of it were a total and complete mess.

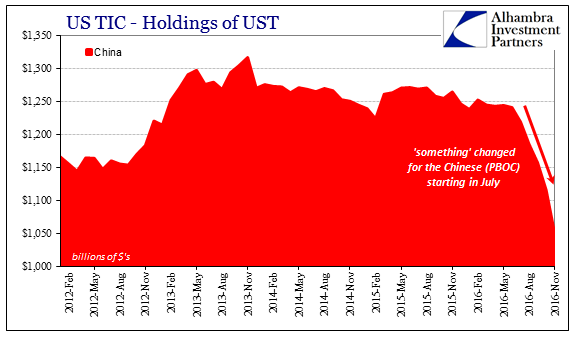

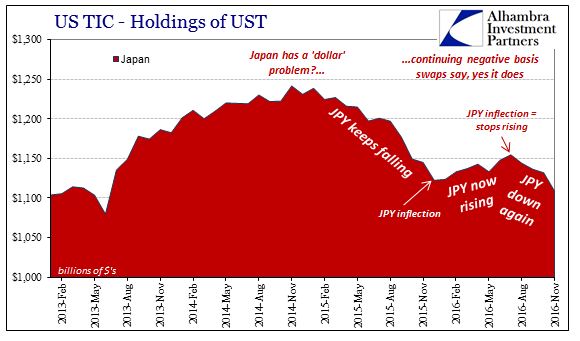

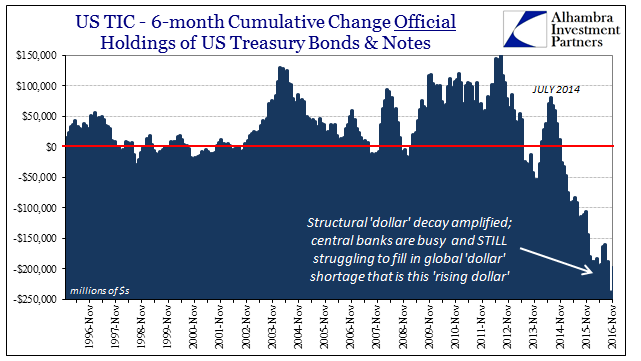

Over the past few years of “global turmoil” attached to this “rising dollar” it has often appeared to have taken on a more foreign (Chinese) flavor. Like Japan in the late 1990’s, foreign central banks especially in 2016 were found to be very busy attempting to offset “capital flows” that by these calibrated derivative statistics we see yet again were neither “capital” nor “flows.” They were, as always, “dollar” destruction in the form of retreating balance sheet capacity (which can often mean simply the lack of growth rather than outright and severe contraction).

Overall gross notionals of US banks, including all types of derivatives beyond forex contracts, fell to $177 trillion in Q3. That was the lowest amount since Q3 2008. Therefore, by these derivative statistics we can account for, roughly, the context as well as the form of global monetary behavior. And from that, economic behavior and conditions. In many ways, the lack of global recovery after the Great “Recession” is the folly of LTCM extrapolated to its perhaps inevitable ends.

Stay In Touch