In a stroke of immensely fortuitous timing, India’s largest automaker Tata Motors was able to raise funds by selling bonds on offshore markets. Faced with an increasing cash crunch and unable to finance working capital needs via strictly Indian banks, the company turned to Singapore. On May 10, 2013, Tata raised S$ 350 million (Singapore dollars) Regulation S bonds paying a 4.25% coupon. It had previously floated S$ 500 million in January that year, but in the name instead of its cash cow Jaguar Land Rover subsidiary.

In the immediate post-crisis era especially, Singapore had become the world’s risk capital, where corporate junk might be underwritten for firms lacking the size to be noticed and realistic in the high yield developed market junk space, or where home countries refused junk debt altogether. It was the global bond market’s version of the offshore pink sheets.

For companies like Tata, it was a godsend, a deep (enough) pool to raise funds without being strangled by Indian monetary mechanics (“dollar” in 2013) or left to pay inordinately high rates in the mainstream offshore exchanges. Not only did Tata Motors go to Singapore for working capital, Tata Communications floated S$ 250 million in January 2013 while Tata Steel raised S$ 300 million that April.

The big Indian conglomerate, however, was more the exception than the rule of late. The global junk corporate market has soured, and the apex of Singapore more so in doubt – for both offshore issuers as well as domestic city companies. The year 2012, as it has turned out, was the high water mark. Total bond market gross was S$ 31.5 billion that tumultuous year, including about S$ 7 billion in corporate junk, but had fallen to S$ 19.9 billion the next one during the year of the “taper tantrum.” Last year, 2016, gross new volume was also less than $20 billion, down 15% from 2015.

The reason for Singapore’s weak bonds last year was, as usual, laid at the doorstep of the Federal Reserve. With rate hikes ongoing, so it is believed, more attractive yields (with less risk) can be obtained in the more mature markets with less risk. Of course, this belief is pervasive even though it is never backed up by actual trading; interest rates in the US and Europe are, in general terms, appreciably lower in 2017 than in 2013 despite now three “rate hikes.”

Rather than take the simple tradeoff as the mainstream would have it, investors in Singapore unlike those in many other jurisdictions have been made appreciate risk the past few years and not strictly of the interest rate variety. Like the Chinese corporate market a few years back, the Singapore corporate market has had to face up to the prospects of default. Oil services firm Swiber, a local company, was forced into judicial management (bankruptcy) last October after missing debt payments last July.

“We had not seen Singapore dollar corporate defaults since 2009, but suddenly we see a pick-up in defaults in 2015-2016. This is a warning sign about a refinancing confidence crisis across many sectors, not just commodity-related ones,” said Raymond Chia, Head of Credit Research for Asia ex-Japan at Schroders Investment Management.

The latest is Ezra, another oil firm that today filed Chapter 11 in protection under United States law and jurisdiction. The problem for Ezra seems to be more than just the stubbornly low price of global oil, where a 80-100% rebound isn’t nearly so impressive after considering its prior 80% collapse. The company’s biggest problem is its debt – it is, or was, leveraged in excess.

This will not be the last default in Singapore’s corporate sector, nor will the defaults be strictly oil and gas related. There is a wave of refinancing about to come due, particularly those both local and foreign taking advantage of what was once an open financing door prior to 2013 (and the inception of what would become the “rising dollar”). For once, the issue isn’t primarily a liquidity story with regard to Singapore, “dollars”, or Singapore dollars. It is, in fact, an economic one and that is the true danger around the world. As Bloomberg reports today:

For some of Singapore’s small debt-laden firms, a rebound in manufacturing and exports hasn’t been enough to bolster bottom lines sufficiently. In the latest sign of strains, Ezra Holdings Ltd., which provides engineering services to the offshore oil and gas sector, filed for Chapter 11 protection March 18 in the U.S. [emphasis added]

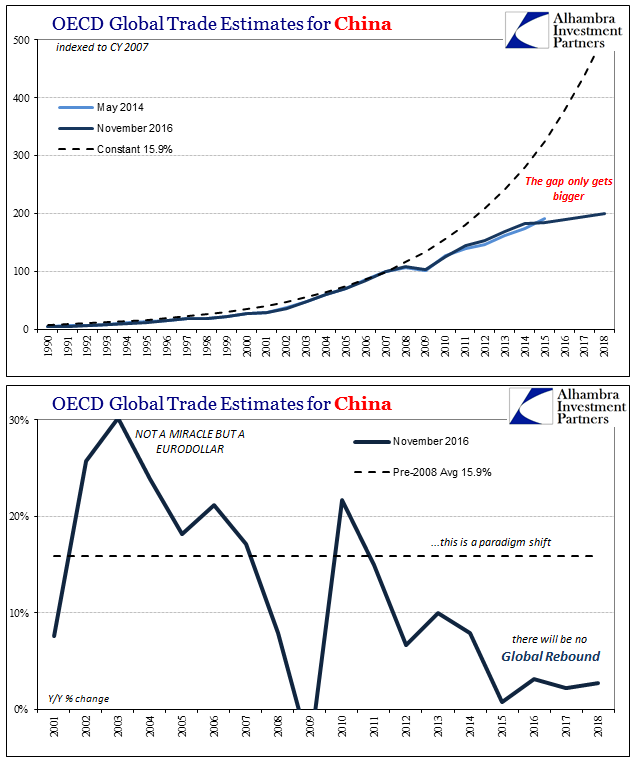

Though the economy especially in Asia is relatively better this year than last year, in the end that comparison just doesn’t mean all that much. This is something I have been writing about for years, the big problem with how the 2012 slowdown wasn’t a cyclical or temporary global downturn but rather the second leg (2009 being the first) lower for the economic baseline (or potential). The entire financing regimes that arose in the initial “recovery” period especially those offshore focused on EM’s or Asia were so based on the idea that the world was going to fully recover at some point. I wrote about a year ago with regard to the Chinese version of this recalibration:

That is why we saw so much “capital outflow” last year as it wasn’t that but rather “dollar” funding being destroyed. Banks may be stupid but they aren’t stupid; they put commitments (funded by “dollars” directly or indirectly as in the forex basis of the PBOC’s balance sheet) into China on the premise of 2011 or 2007 growth being the standard. These 2015/16 growth rates only further confirm that will never happen, so it is a race to not be the Greater Fool at this point.

So much debt had been created out there in the world up until the “rising dollar” as if going back to the EM “miracles” of the mid-2000’s was at least possible. Even if the developed world might labor under some unexplained “new normal”, surely the EM world would continue on with high growth and “rebalancing” predicated on the assumed wealth attained during those pre-crisis years. At the time it was categorized as “reach for yield”, but that doesn’t begin to describe the imbalance of financial factors. So much of the world’s credit remains tied to an economic paradigm that no longer exists, and for which only in the past few years have “investors” begun to catch on.

In early January 2016, as the “dollar” began for a second time to roil global markets and so strain its economy, Tata Motors bought back two years early 91.07% of its 4.25% Singapore bonds.

Stay In Touch