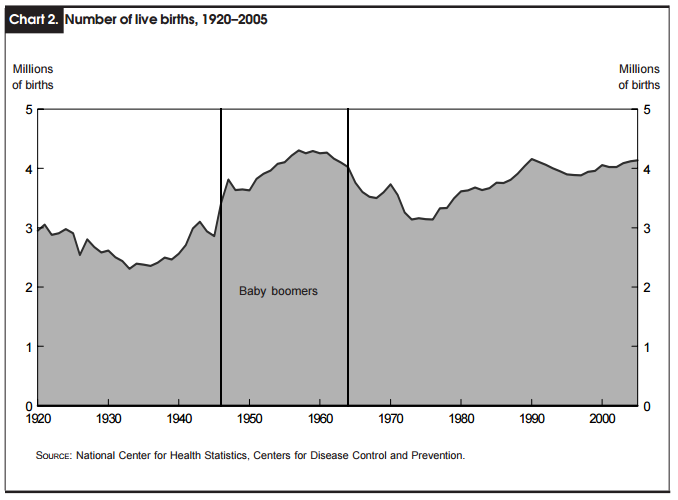

The aging of the Baby Boomers is not something that caught economists completely by surprise. That generation has been the subject of (academic) study going back to the surge in birth rates right after World War II. In economic terms, the challenges presented by the prospective retirement years for this cohort has been anticipated to some degree all along, particularly as the 20th century from which the demographics were born ended.

In November 2006, the Bureau of Labor Statistics in its Monthly Review magazine published a lengthy study that sought to quantify these aspects. Of specific interest was, since this was a BLS publication, any possible effects on the labor market. The labor force had expanded rapidly in the 1970’s due to both the Baby Boomers coming of working age as well as the rising participation of women. Thirty years later, conditions were projected to be much different:

With an annual growth rate of 0.6 percent over the 2005–50 period, the labor force is projected to reach 194.8 million in 2050. Peaking at 2.6 percent during the 1970s, the growth rate of the labor force has been decreasing with the passage of each decade and is expected to continue to do so in the future.

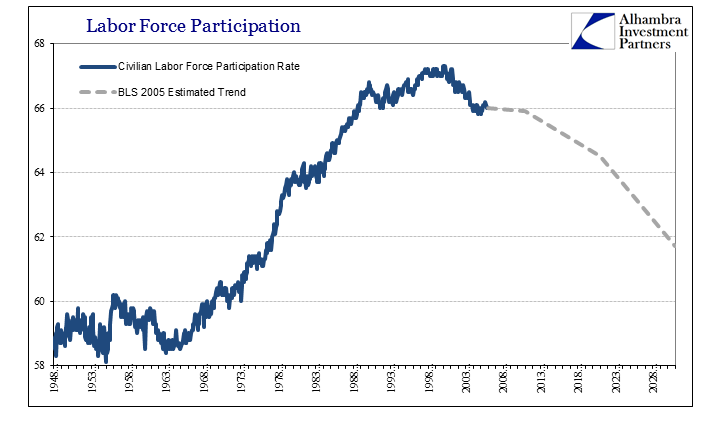

Using various statistical and regression-based models, the BLS figured that the Civilian Labor Force Participation rate would decline to 65.9% by 2010 from 66.0% at that time in 2005. By 2020, the participation rate would be 64.5% and ten years later just 61.7% as the bulk of the demographic retirement would have by then transpired.

There were considerable uncertainties and qualifications to these predictions, of course, as there always are trying to predict so far into the future (and using extrapolations of the past as the primary guide). Among them, the BLS listed immigration, further gains in the participation rate of women, or the young (it was the housing boom, after all, and construction work was plentiful at the time), but also the prospect of seniors themselves working longer. What wasn’t included as a possible trend-changer was a massive economic collapse caused by systemic monetary rejection that contrary to the very nature of recession meant a permanent alteration in the global economic system.

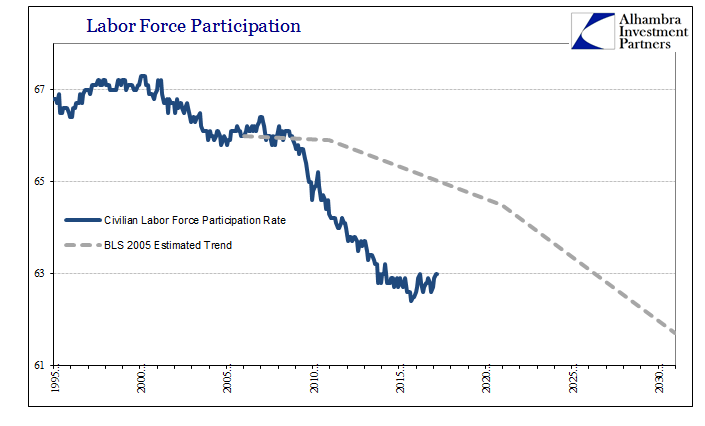

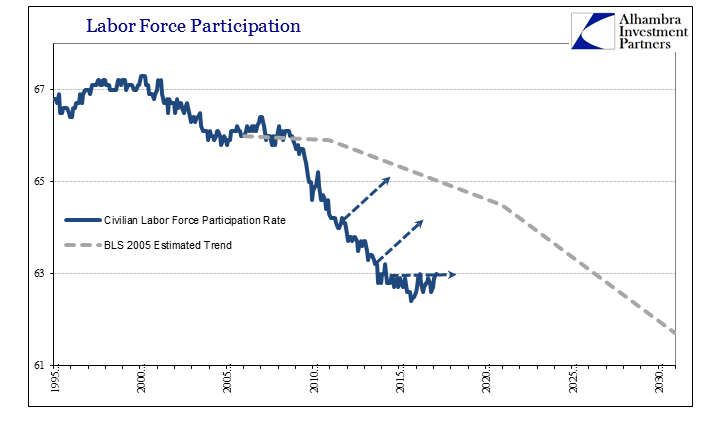

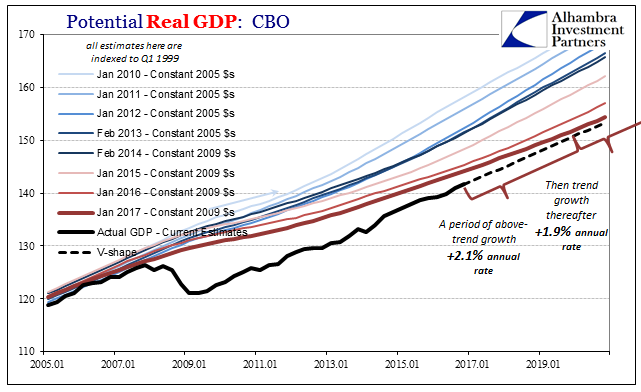

In the years since the Great “Recession”, economists and policymakers have feverishly tried to reconcile this difference. This is not to say that the BLS’ 2005 projections are the correct starting point for estimation, but they were much closer to consensus pre-crisis, an estimation that lasted several years into the “recovery.” It is the lack of it in the labor force that has gained so much notice and led to an enormous divergence about what it could possibly mean. If the gray dotted line above should have been closer to the actual track of the participation rate to more accurately reflect demographic changes, then there would have been no use at all for any but the first and maybe second QE (according to orthodox understanding; in reality, there was never much use for QE in any context).

Policymakers themselves remained far more sympathetic to the 2005 trajectory, and that is why they tried four QE’s in total lasting all the way to the end of 2014. A large gap between that prediction and reality meant cyclicality, a shortfall in “aggregate demand” (large output gap) which “stimulus” would alleviate given enough time. As Janet Yellen said in February 2013 just as QE4 (UST purchases) was really just getting started:

For the Federal Reserve, the answer to this question has important implications for monetary policy. If the current, elevated rate of unemployment is largely cyclical, then the straightforward solution is to take action to raise aggregate demand. If unemployment is instead substantially structural, some worry that attempts to raise aggregate demand will have little effect on unemployment and serve only to stoke inflation.

This question is frequently discussed by the FOMC. I cannot speak for the Committee or my colleagues, some of whom have publicly related their own conclusions on this topic. However, I see the evidence as consistent with the view that the increase in unemployment since the onset of the Great Recession has been largely cyclical and not structural.

Indeed, even with a speech to the Jackson Hole audience more than two years later in August 2014, Yellen attempted to argue that some of the assumed structural factors were themselves in part arising due to the remaining cyclical shortfall.

What is more difficult to determine is whether some portion of the increase in disability rates, retirements, and school enrollments since the Great Recession reflects cyclical forces. While structural factors have clearly and importantly affected each of these three trends, some portion of the decline in labor force participation resulting from these trends could be related to the recession and slow recovery and therefore might reverse in a stronger labor market.

As she said, the number of Americans taking disability (as well as college enrollment) in the past correlated with recessions, and the unusually large rise in those doing the same after 2008 in just plain common sense terms would be consistent with the unusually large contraction of the Great “Recession” and particularly the negative effect on the labor force. In fact, one implied goal of this particular speech was to claim a need for such nuance in assessing the labor market, justifying continued monetary “accommodation.”

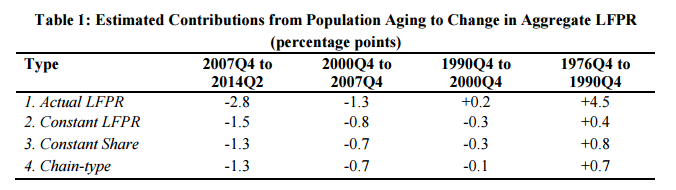

On the other side were other studies that more aggressively asserted the structural argument. One such extensive work was published by the Federal Reserve Bank of Cleveland in September 2014. It determined that half of the decline in the participation rate was Baby Boomer retirement:

As it happens, however, the three calculations in table 1 do not differ greatly when it comes to the post-2007 period: all indicate that the changing age distribution of the population has been a substantial component of the decline in aggregate labor force participation over this period, with our preferred calculation attributing nearly half of the observed decline to this source. [emphasis added]

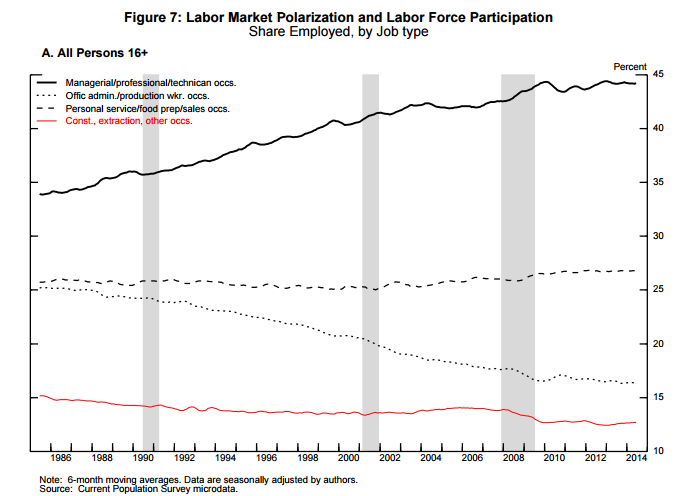

A significant portion of the rest of the participation gap was, in their math, due to the rising “polarization” of the labor market, a trend that had been in evidence for several decades before the events of 2008.

Returning to the top panel of figure 4, prime age males without a college degree have experienced a long secular decline in their participation rates, joined by prime age women without a college degree beginning in the early 2000s. These declines have been the subject of a considerable literature reaching back to the 1980s. The early literature, which focused on prime age men, identified declining labor market opportunities for low-skilled workers, manifested in stagnant real wage growth, as the likely explanation (e.g. Juhn, 1992). However, since the 1990s, changes in labor demand have not been characterized by a monotonic increase in the demand for skilled workers, but rather by a decline in labor demand for occupations that have tended to be “middle-paying” or middle-skill jobs, and a concurrent increase in the both the share employed in higher-paying jobs (for better educated persons) and the share employed in lower paying jobs (for less educated persons), e.g. Autor 2010. Can this polarization explain the decline in labor force participation among these workers over the past decade or two?

This is the genesis for the “skills mismatch”, which has further attained drug addicts and lazy locals to its assumed nature. Monetary policy nor indeed any “stimulus” would be powerless to affect changes in such an environment where such polarization might be prevalent. The only answer to that challenge would be education of some kind, largely university related but not exclusively so. It is a matter not for any central bank to do more than catalog and study.

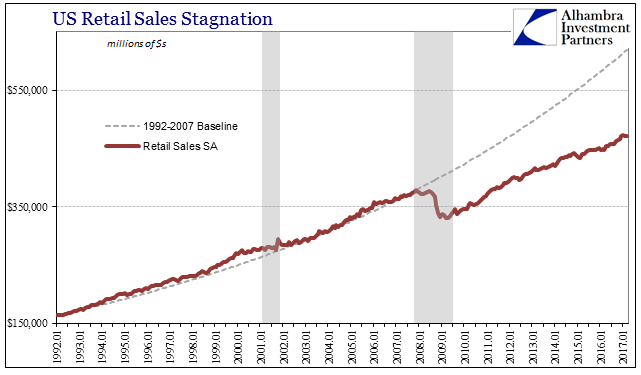

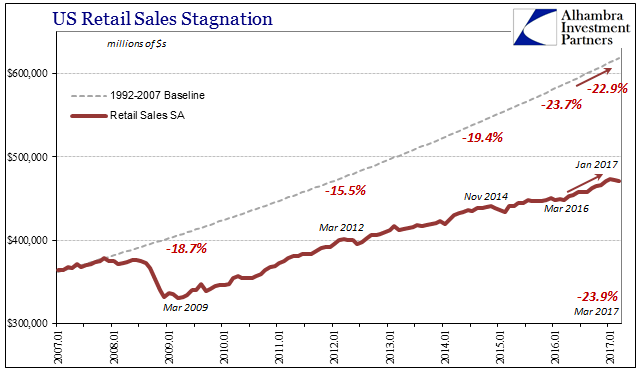

What none of these studies or speeches ever address, however, they don’t even bring it up, is why it all just happened in 2008. Their focus is always the lingering problems with recovery, such that it was, and therefore are limited to labor statistics like participation rates. But if half of the decline or even more might be due to retirement, then why hasn’t spending recovered even slightly? A Baby Boomer who is working one day and retired the next doesn’t stop shopping when they are handed their symbolic gold watch. They may become more frugal in what they buy and when, but that is a smaller adjustment rather than the permanent aggregate shift we all recognize in various ways.

The track of retail sales shows what none of these economists and policymakers are talking about. The huge hole was created in late 2008 and early 2009, coincident not coincidentally to the first global financial panic since the 1930’s, which was then made permanent into a lack of economic recovery. Workers who built homes pre-crisis and then claimed disability post-crisis would like retirees still be spending if also at a lower rate; college age graduates who would likely have joined the workforce after graduation who now instead stay enrolled that much longer in graduate or post-graduate programs are still eating (out) and buying clothes.

What is missing is opportunity, pure and simple. That would mean Yellen’s instincts were right all along, what failed her was (largely Bernanke’s) execution. There is actually a third option never considered, and given the politics of Economics won’t ever be. If the first was normal cycle, the one chosen to be fixed by QE’s and ZIRP, and the second labor structure, one with no hope of solution on its own, the third is even more obvious and far less convoluted:

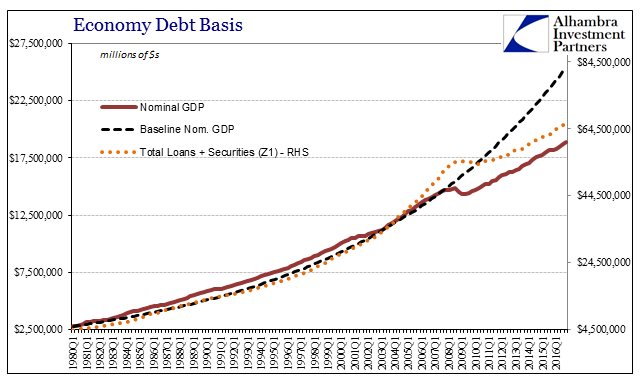

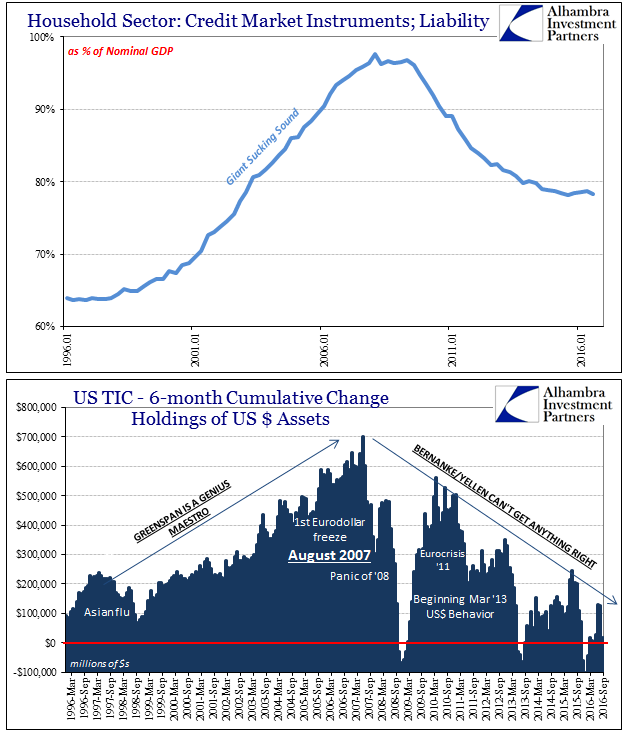

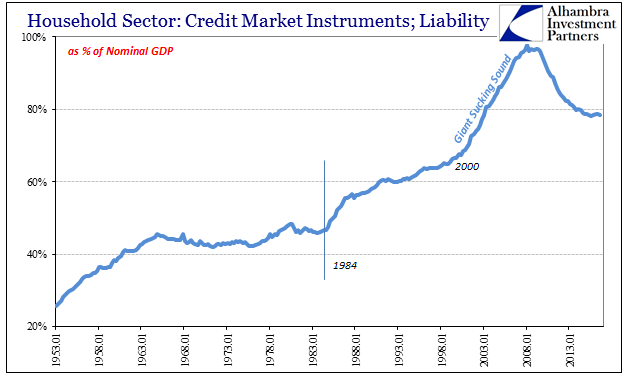

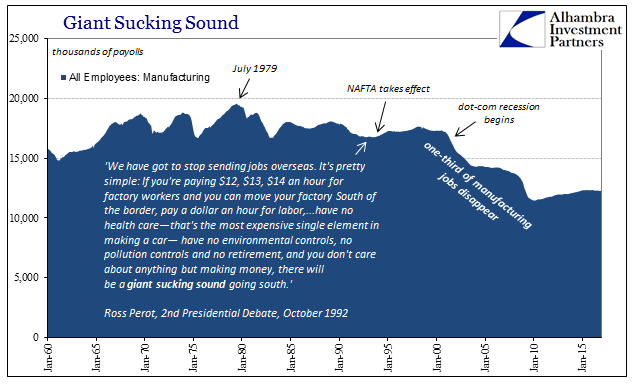

It is the combination of one aspect of “polarization”, the offshoring of those very middle-area production jobs, with the monetary and credit overdrive of the late eurodollar system. In 2008, the eurodollar’s self-rejection of the assumptions supporting its meteoric rise (only high returns for little or no presumed risk) meant the credit supplement for Americans was all at once turned off – and never really turned back on. That had the effect of exposing the loss of earned income under polarization, leading to spending exhibiting a clear dislocation right at the moment that marginal credit was terminated. If national income supporting national spending was 80% earned and 20% credit, then spending without credit would suddenly drop to 80% and stay there.

This is not a pathology that Economics will ever take, however, due to assumptions first about monetary neutrality and then rational expectations and efficient markets. In the condensed world of conventional central banks, they all did their “stimulus” often massive and supposedly powerful and achieved very little by them. Thus, the answer to the economic “conundrum” must be elsewhere, even in the labor market itself. But to believe that we are forced to also believing that older workers all at once decided that the failure of Lehman was their signal to retire and then stop buying things altogether (only some hyperbole). It flies in the face of common sense, and it was even a qualification that the 2006 BLS study contemplated in reverse:

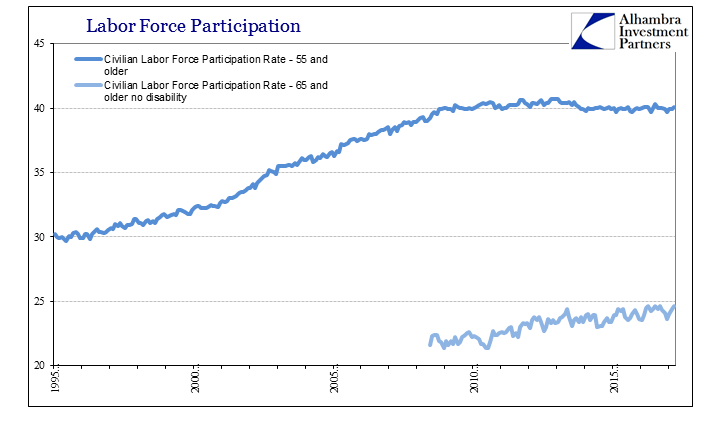

The labor force participation rate of older workers has been increasing since the end of the 1980s. The decision to continue work into the later years of life has been the result of several intertwined factors, such as the continually increasing life expectancy of the population, wherein a growing number of people are healthier for a longer portion of their life span. Because the average number of years spent in retirement has been rising steadily over the past several decades, and even before that, since the 1980s older workers have increasingly chosen to remain in the labor force in pursuit of additional earnings. In addition, the elimination of mandatory retirement and the enactment of age discrimination laws have contributed to the increase in participation rates of older persons.

Economists attributing this lengthy economic depression to Baby Boomers do so on an assumption that the rate of retirement is constant with age. It may not be; BLS estimates suggest that it is not.

The structural issues raised by economists are very real problems and they do require every careful consideration. But they are certainly not the problem, a combination so deleterious they rendered the Fed’s $4.5 trillion balance sheet completely irrelevant. The labor market questions are being elevated by that irrelevancy alone chiefly because economists have left themselves no other suspects. QE’s were balance sheet expansion and nothing more, leaving the global system to survive monetarily without any aid whatsoever (apart from psychology). It reacted accordingly (risk vs. reward) leaving the economy further exposed to its permanent withdrawal.

For Janet Yellen, it is impossible for her in 2017 to admit all those bank reserves they created were useless and inert rather than dollars. It is much easier to claim necessary nuance about considerable labor market uncertainties where no satisfying answer may ever be found. Into that fog of mystery the Fed can exit.

Stay In Touch