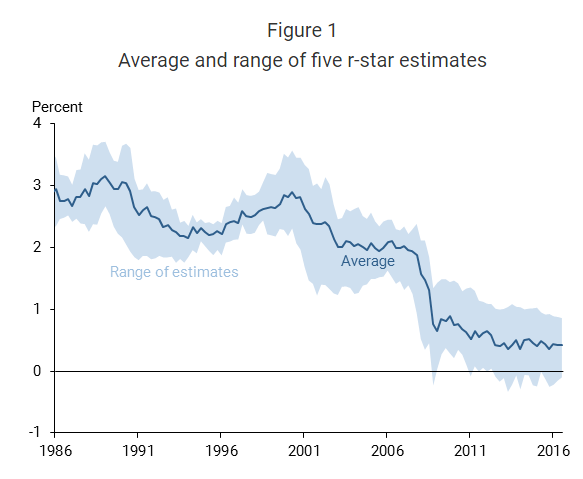

It’s such an obvious thing, so maybe that is why no one mentions it. I doubt that is the reason, however, because doing so isn’t a mystery so much as narrowing down suspects. That is why when talking about the so-called natural rate of interest, or R* (r-star), the issue is (intentionally) cloaked in the language of the very long run. Pay no attention to that big decline and the timing of it; instead worry only about economic trends that predate the internet.

San Francisco Fed President (and CEO) John Williams has been carrying the torch of R* ever since it was updated to econometrics at the dawn of the 21st century. The idea was a 19th century one, where Swedish economist Knut Wicksell theorized an equilibrium interest balancing with commodity prices. At this harmonizing point, the economy might grow without sparking inflation, which for a central bank would be pure magic – if it could ever be found, further assuming such a thing would ever exist.

That is the primary problem with R*, as why would any complex economy feature just one equilibrium rate of interest; and even if there was one, why would it be stable for more than just a few minutes, let alone months or years? Economists like Williams recognize that even in their quest for it, R* must in the long run move around. In trying to reverse engineer the thing, for it isn’t something that can be observed, the literature especially out of San Francisco has found global coherence with it.

In other words, not only has R* fallen in the US, it has done so everywhere else these economists have studied. Such synchronization should raise alarms, but does not. Instead, there is rarely much mention of how that could realistically occur as well as trying best to, as stated above, ignore the blaringly obvious timing.

The 21st century has been an exclusively downward journey for it, but most completely and so far permanently after that big drop in, surprise, 2008. Yet, for all the clear certainty of that contravention, the literature is surprisingly (or not) devoid of all mentions about the Great “Recession.” In the publication the chart above was taken from, FRBSF’s February 2017 newsletter, in an article authored by John Williams, the Great “Recession” was not mentioned even once; the word “recession” itself was on one occasion and in the context of near nonsense:

For example, the U.S. economy has fully recovered from the recession following the financial crisis, and the most recent estimates of r-star there have shown no signs of rebounding.

If you are slightly confused by what appears to be a contradiction, that is because Williams’ statement requires translation. I provide as much for my column tomorrow:

The most obvious inference from that statement is that he is using the word “recovery” in a way that is very different from what it actually means. Recovery, as in the business cycle segment, means just that – complete healing from the trauma of recession. What Williams wrote instead was that the economy has fully recovered even though there is no sign of it having healed even slightly. He has detached monetary policy from reality because he thinks he can.

It is Alan Greenspan’s conundrum turned upside down by the events of 2008, but as if the events of 2008 created no lasting effect. Economists have always held a tenuous grasp of the bond market, but this is taken to new levels of wonder. The “logic” of a low R* is simply the fact that interest rates are low and show no sign of being anything else, and the economy remains so bad despite it. Thus, people like John Williams take the view of low (and often negative) interest rates being “stimulus” and therefore the lack of effect must be due to a broken economy, reflected in perhaps even a negative R*. For them, it can never be that low rates are something else altogether.

From there, monetary policy is blameless because the economy fully recovered; from broken to still broken. They have no answers for how it was broken except as to speculate about longer run trends so long as they don’t touch on 2008.

What is really going on is that this is the only way economists think they can plausibly admit this economic depression while subtracting themselves from it. They will never, ever call it that, instead they will and have, as noted above, say it was nothing less than full recovery. The end result remains the same, however, for the growth trajectory of the global economy will be nothing like what it was ten years ago. That’s a huge problem, and the big problem of R* is that economists are declaring there is nothing that can be done about it (plus it would be so much more convincing had they predicted this result, worrying about the natural in permanent subduction in 2007 or even 2014 rather than 2016 and 2017 after the recovery had thoroughly been disproved).

Ten years after all this started, it is those events that remain relevant. And it is those very things that these “experts” want nothing to do with. Just as the history of the QE’s has been quietly purged from polite contemporary discussions, so too will the massive, generational monetary failure that we aren’t supposed to think played any role in how we got here – even though it is the central axis on everything.

There is one thing that can and should be done; that is to remove economists from the equation just as they try to remove 2008 from all considerations. There is and has been no money in monetary policy, but the more we go without anything resembling real growth there won’t even be policy in monetary policy. Subtracting both money and policy from monetary policy, though, wouldn’t really be much of a change. That is what actually matters, and though economists like John Williams won’t be able to see, that is what R* in a more realistic conjunction with interest rates as they are actually tells us.

Stay In Touch